In December, I wrote:

I’ve witnessed over three decades of economic cycles now – and I’ve never seen a time when [real estate investment trust (“REIT”)] valuations were so attractive. They’re boasting strong fundamentals, favorable supply trends, and capital markets that are wide open.

I went on to show how real estate tends to outperform following years where it had underperformed. The “spring back” rallies of 2010 and 2021 are the best examples. It stood to reason that, after an underwhelming 2025, real estate might get up and go as we entered 2026.

So far, so good…

The S&P 500 Real Estate Index added 2.9% in January. That’s not bad considering how geopolitical developments in Venezuela and Greenland sent everyone into several tizzies. Then tech sold off, taking up even more oxygen.

As a result, the S&P 500 has gained just 1.29% year to date, less than half of the return printed by real estate.

Of course, one month a year does not make a trend. Anything can happen from here. I’ll be paying special attention to Trump’s nominee for Federal Reserve chair, Kevin Warsh. A former Fed governor, Warsh was in at the Fed during the bailout years of 2008/2009. But he has also been a Fed critic in recent years. What the Warsh era (assuming he’s confirmed) will look like is anybody’s guess. I’ll share some more thoughts on Warsh later this week.

But for the time being, it appears REITs are having a moment. And if this does turn out to be the year of the “REIT Renaissance,” it’s worth having a look at who the likely leaders will be.

One that I have high hopes for is industrial king Prologis (PLD). Let’s see what we can expect from it for the balance of 2026.

Prologis Just Doesn’t Stop Succeeding

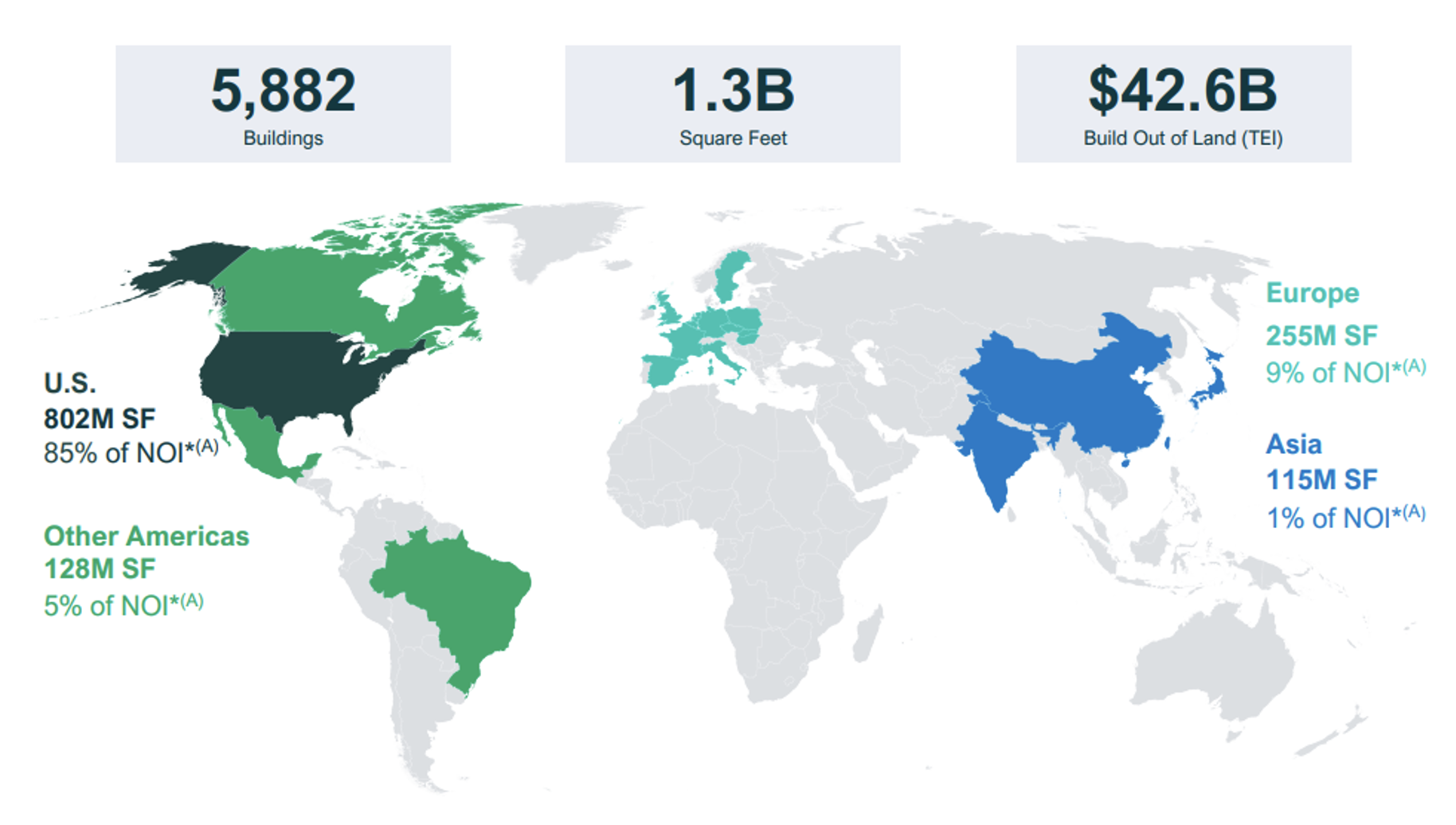

Prologis is a global leader in logistics real estate with a focus on high-barrier, high-growth markets. As of the fourth quarter of 2025, it had around 5,882 buildings comprising 1.3 billion square feet spread across:

-

The U.S. (85% of net operating income, or NOI)

-

Other Americas (5%)

-

Europe (9%)

-

Asia (1%)

Prologis also has a buildable land portfolio that could support new build-to-suit (“BTS”) projects worth around $42 billion in total expected investment (“TEI”). That includes another $1.1 billion in new buildings, with 48% BTS in the fourth quarter.

The warehouse REIT started this year with $3.1 billion in BTS projects. This allows it to generate attractive returns since these assets are much less risky than speculative construction.

Source: PLD Investor Deck

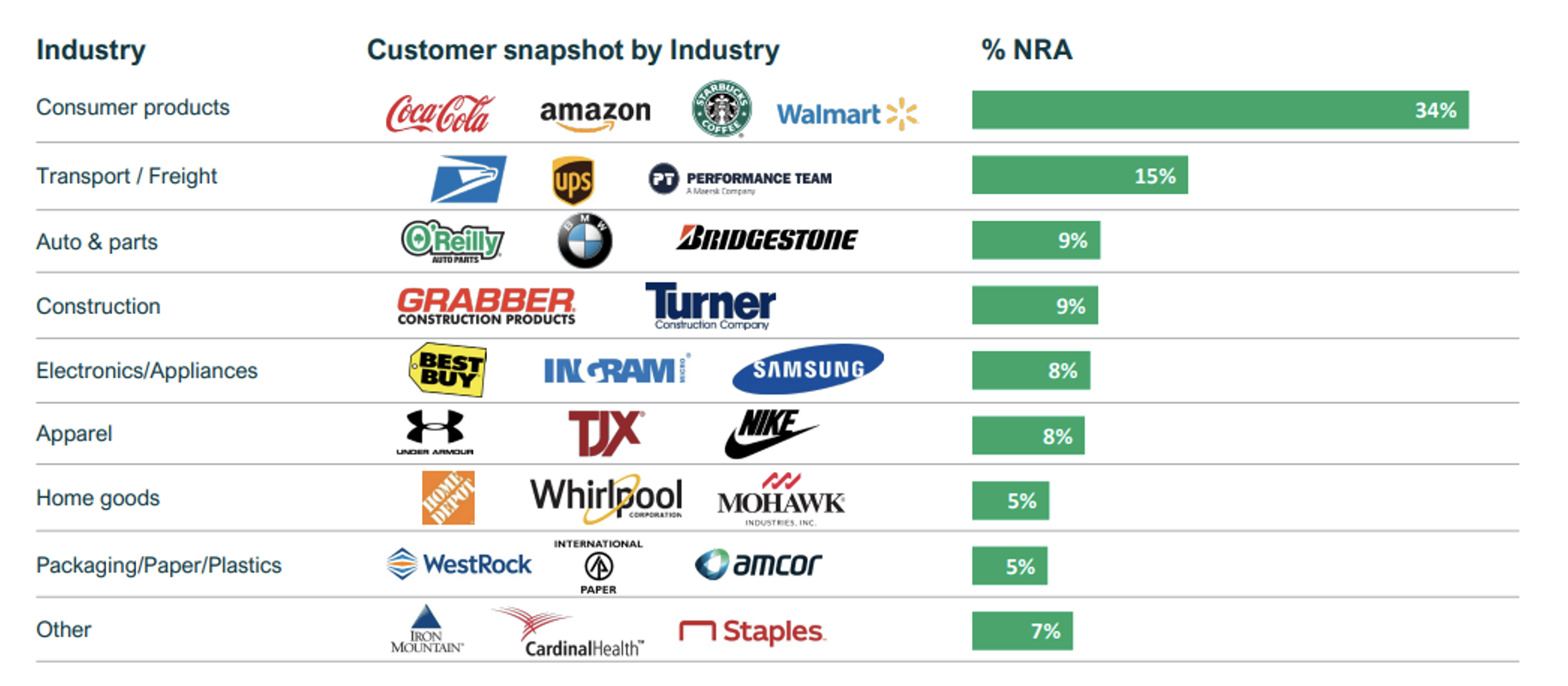

Prologis’ broad diversification – including 6,500 customers – is one part of its business model moat, giving it a best-in-class scale advantage. In fact, it’s the largest industrial REIT in the world, with 556 assets in Southern California alone. To say nothing of its properties across Northern California, New York, New Jersey, Chicago, the Dallas-Fort Worth area, South Florida, Atlanta, Houston Seattle, and Baltimore.

Vacancies among this widespread array of assets remain low at around 7.4%. And Prologis expects that number to tighten further to around 7.2% by the end of 2026.

In the fourth quarter of 2025, the company signed 57 million square feet of leases, driving occupancy to around 96%. Its 78% lease renewal rate reinforces that Prologis makes it fairly easy for tenants to rationalize their footprints.

Source: PLD Investor Presentation

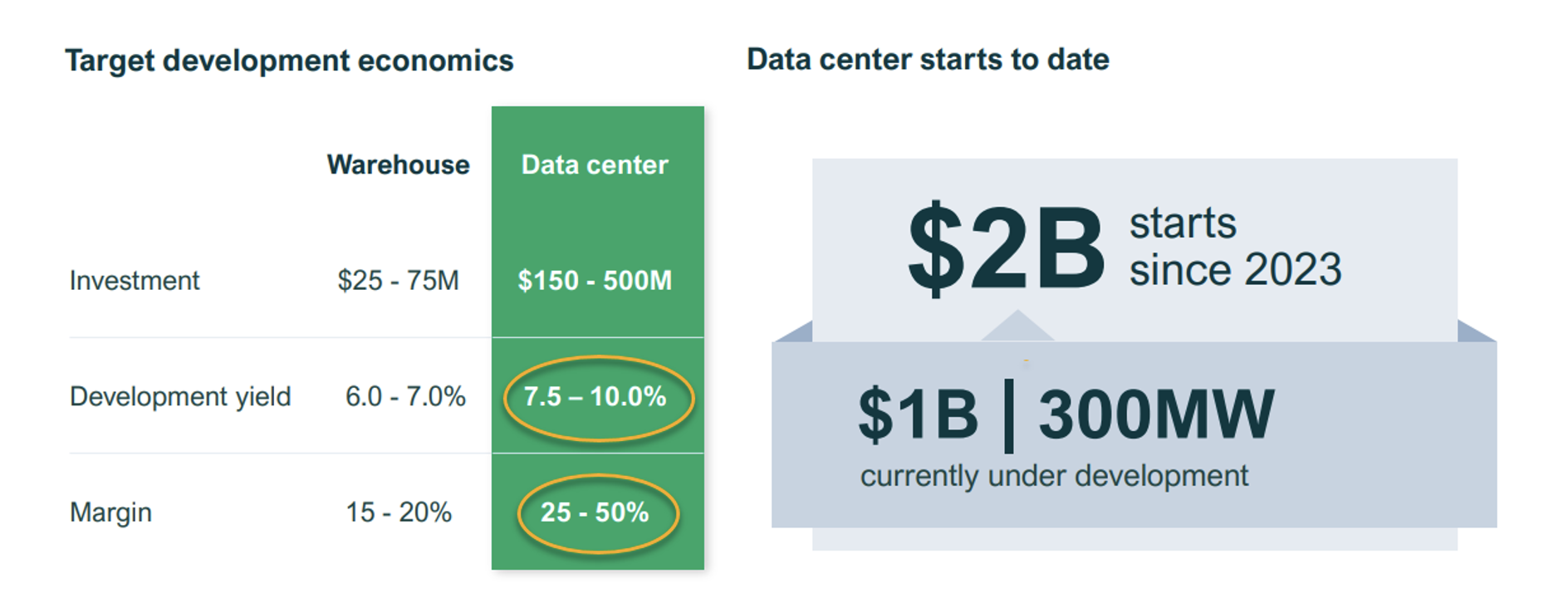

Another wide-moat advantage for Prologis is its increased engagement with the data-center business. Despite being known for its warehouses – and with good reason – approximately 40% of its 2026 global development starts are targeted toward data centers.

With a 5.7-gigawatt (“GW”) power pipeline, Prologis is participating in the trend of land with access to power becoming increasingly valuable. Yet it’s being strategic in its selection process. Logistics remain the foundation of its inroads here, as land and capital are increasingly being allocated to digital infrastructure.

Source: Prologis Investor Deck

Analysts project the U.S. needs $7 trillion worth of data-center investments by 2030 to keep pace with computing power. And Prologis has a unique advantage to harness these developments to generate outsized returns…

Prologis: Making More Great Moves

During the fourth quarter of 2025, Prologis:

-

Expanded its power access to 5.7 gigawatts

-

Stabilized 72 megawatts of projects

-

Sold a state-of-the-art turnkey facility

Its leasing demand is exceptional, and every megawatt in the company’s pipeline is in some stage of discussion. That includes 1.2 gigawatts currently in letter of intent (“LOI”) or pending lease execution.

Then there’s Prologis’ fortress balance sheet. The company maintains an A2 rating with Moody’s and an A with S&P, plus a 3.2% weighted average interest rate. It also has well-staggered debt maturities with a long weighted average term remaining of 8.3 years.

In the fourth quarter of 2025, funds from operations (“FFO”) were $1.44 per share, including net promote expenses; and $1.46 per share, excluding net promote expenses. That meant it finished the year at the top end of both guidance ranges.

Same-store NOI growth, meanwhile, was 4.7% on a net effective basis and 5.7% on a cash basis. Each was, once again, ahead of midpoint guidance.

In terms of valuation, Prologis is trading at $130.56, with a price to adjusted FFO (“AFFO”) multiple of 28.6 times and a 3.1% dividend yield. Keep in mind it’s maintained solid fundamentals over the past 15 years, with steady dividend growth over the past 10.

Source: FAST Graphs

Considering its successes last year and its continued inroads into data centers now… I believe Prologis should easily be able to continue along its path of high double-digit growth. Analysts forecast 8% in 2026 and 9% in 2027.

My only concern is that while shares are fairly valued, they’re not a bargain. So I do recommend waiting on a pullback closer to the $120 mark. Though, admittedly, that train may have already left the station, as demand is moving in the right direction.

Fortunately, as I said earlier, there are plenty of other places to look for well-priced REITs. Ones that could return quite 20% or more in 2026.

Stay tuned in the weeks to come as my team and I continue to look for the widest moats with the most attractive bargains.

Regards,

Brad Thomas

Editor, Wide Moat Daily

|