In December 2019, I published an article for Forbes – “It’s A Sad Day For My Hometown Mall.”

In it, I explained the up-and-down history of Westgate Mall, a retail gem up in my neck of the woods:

CBL & Associates (CBL), based in Chattanooga, Tennessee, purchased the mall. Moreover, it proceeded to do significant work on it, expanding the building and adding in two new anchors: Dillard’s and J.B. White.

The refurbished property was then touted long and loud as “the first Carolina mall with six anchors.”

[…]

Over the next several years, both the Blackstock Center and Westgate Mall flourished. A new Wal-Mart anchored center was built nearby, and an Olive Garden opened as well.

For a while, things were good.

But that was a very long time ago.

From the article:

CBL still owns [the mall], but it’s in bad shape.

For one thing, Sears has shuttered. For another, the building’s interior looks like a flea market.

As traffic fades, so has occupancy, which is only to be expected. It’s down to 82% based on recent filings. Meanwhile, the Toys “R” Us property across the street continues to still sit there. Vacant.

Making matters worse, the $34 million loan on the mall, which is securitized through UBS-Barclays Commercial Mortgage Trust, could default.

As it stands now, [JCPenney] is still holding on. But it appears its days there are numbered. And Dick’s Sporting Goods, another anchor, is likely closing soon.

I was (unfortunately) correct.

Dick’s Sporting Goods closed in 2021. Bed Bath and Beyond, another anchor, closed in 2023. CBL filed Chapter 11 that same year. I actually tried to buy the mall when that happened. It was a very complicated deal, and it didn’t work out, but that’s a story for another day.

The JCPenney is still hanging in there. But recent reviews from shoppers are less than inspiring. Here’s an unfortunate one from TripAdvisor:

This bankrupt mall is essentially dead. Dillard’s and Belk’s are good stores and [JCPenney] is fine. The mall itself is extremely poorly managed. Recently they have told hundreds of shoppers that if they shop in the mall and have not purchased anything they have to LEAVE.

It would seem to have been a sad few years for my local mall…

From Apocalypse to Apathy

I know shopping malls might seem an odd topic to write about.

After all, we live in a world of artificial intelligence… tariffs… Jamie Dimon’s latest comments… and did I mention artificial intelligence?

But just hear me out. You might be surprised by what you learn.

Investors paid some attention to shopping malls in 2020 and 2021… but not for good reasons. Those were the days of the “mall apocalypse,” when the prevailing wisdom was that lockdowns and e-commerce would finally put traditional malls in the dirt.

That sentiment has been largely replaced by apathy. Investors just don’t spend much time – if any at all – thinking about malls.

But the truth is that these buildings are becoming more relevant in many ways, not less.

And while mall real estate investment trusts (“REITs”) might not seem “exciting,” there could be some interesting investment opportunities for those who bother to look.

The Death of Malls Has Been (Slightly) Exaggerated

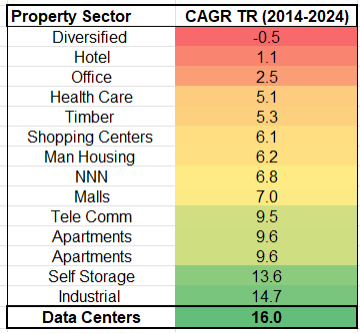

I’ll be the first to admit that malls haven’t been thriving, as my own story above demonstrates. But at the same time, this property sector hasn’t been performing that poorly, as the chart below will show.

Source: Wide Moat Research

On a total return basis, malls haven’t been barnburners the way data centers have been. At an approximate 7% compound annual growth rate (“CAGR”) between 2014 and 2024, they’re almost smack-dab in the middle. Not great, but also not as bad as most expect.

And to understand why this is, you really have to understand the true problems malls had in the first place… and what it means for those still standing.

Only the Strong Survived

Shopping malls’ biggest problem wasn’t really ever e-commerce, believe it or not. It was overbuilding. I actually mentioned this in my 2019 Forbes article:

I was a developer for over 20 years, building shopping centers especially. That was back in the midst of a retail expansion like we’d never seen before and may never see again.

Bankers were loaning money as fast as it was printed, and retailers were expanding in record numbers. Even in my hometown of Spartanburg, South Carolina, my business partner and I built more than 20 projects in the course of 10 years.

It’s simple economics: When too many sellers offer the same products in close proximity to each other, they’re going to eat into each other’s profits. And while those margins might work during ideal conditions, the second hardships arise, losers emerge quickly.

Then again, so do winners.

It stands to reason that mall landlords who have survived this whittling process… and the rise of e-commerce… and the shutdowns… might be capable of surviving still. And that really is what we’re seeing.

An interesting example might be Simon Property Group (SPG). The largest mall owner in the U.S. took on a surprising initiative – convincing young people to come back to the mall.

SPG launched a campaign last year called "Meet Me @themall." It’s centered around “talking about how it’s fun to go to the mall and hang out just like in the ’80s and ’90s,” Chairman, CEO, and President David Simon explained in February.

That might seem unusual. The terminally-online younger generations are often considered one of the main culprits for struggling malls. But that’s not actually the case.

A 2024 survey by mall industry group ICSC, did show that Gen Z shops in stores more than both millennials and Gen X – much more akin to Baby Boomer habits, in fact…

The results for SPG: Occupancy rose from 95.8% at the end of 2023 to 96.5% at the end of 2024. That might not sound like much. But take it from somebody who has done this kind of work. Those little changes can make all the difference, especially at scale.

There are other reasons to be optimistic.

ICSC found in its annual survey last year that:

Physical stores continue to play a major role in holiday shopping. Ninety-two percent of shoppers will spend in a physical store. Brick-and-mortar remains a valuable driver of omnichannel shopping, as nearly all in-store shoppers also plan to buy online from the same retailer’s website, with almost half saying that browsing in stores will influence their purchases.

Consumers still recognize the value of in-person shopping, including at malls. Retailers themselves recognize it, too, with even online-only businesses as big as Amazon (AMZN) moving to open physical locations.

Malls might have faltered over the years. But they’re far from “dead.” And that presents an interesting opportunity for investors.

Simon: A Mall REIT Extraordinaire

Looking at the mall REIT sector specifically, it looks expensive at first glance. But keep in mind they were trading with extremely cheap valuations during COVID and the retail “Armageddon.” Those events skewed their normal numbers quite a bit.

Even now, malls trade at 14 times forward AFFO (adjusted funds from operations). REITs overall are around 19 times.

I’ll admit I’ve been cautious in this area for years, watching and waiting while the consolidation process plays out. And considering the drama and outright bankruptcies we saw both before and after COVID…

It seems safe to say that restraint paid off.

Now might be a good time to look at the aforementioned Simon Property Group. It’s the largest mall REIT with 194 properties in the U.S. alone, comprised of:

-

92 malls

-

70 premium outlets

-

14 mills

-

6 lifestyle centers

-

12 other retail properties

SPG also owns an 88% non-controlling interest in Taubman Realty Group, which itself holds interest in 22 malls and outlets across the U.S. and Asia. And Simon has additional stakes in 35 premium outlets and designer outlet properties mainly located across Asia, Europe, and Canada.

There’s also SPG’s 22.4% equity stake in Klépierre SA, or Klépierre – a publicly traded, Paris-based real estate company that owns or holds interest in shopping centers across 14 European countries.

Naturally, this all gives it scale advantage, which is used to build an A rated balance sheet with a positive S&P outlook.

Better yet, Simon is somehow trading at a modest discount of 14.4 times versus its “normal” 15.5 times. Plus, its dividend yield is 5.2% and well covered.

Source: FAST Graphs

There are other mall REITs out there to consider, it’s true. But Simon is my first suggestion for those looking to dip their toes into the sector.

Perhaps it has been a sad few years for my local mall. But, for mall investors, there’s plenty of reason to expect the next few years could be happier ones.

Regards,

Brad Thomas

Editor, Wide Moat Daily

P.S. Next week, I’ll provide readers with an overview of another REIT retail sector: shopping centers. There are several attractive value propositions there that are well worth knowing about.

|