In August, I showed that Warren Buffett was buying into American homebuilders. And I told you why I was not.

From that Wide Moat Daily:

Between high list prices, high mortgage prices… and how debt-ridden consumers are… there’s not much incentive for people to buy a home these days. Which means there’s not much room for homebuilders to profit.

But Buffett is a stock-picking legend for a reason. The two homebuilders he picked up for the Berkshire portfolio – Lennar (LEN) and D.R. Horton (DHI) – have done quite well since August. They’re up about 13% and 10.3%, respectively, in just two months.

Perhaps Buffett saw something I didn’t see.

And it would appear the White House is throwing its full support behind homebuilders. Here’s the president in a Truth Social post on Sunday:

Before I became President, “OPEC” kept Oil prices high. It wasn’t right for them to do that but, in a different form, [it’s] being done again – This time by the Big Homebuilders of our Nation. They’re my friends, and they’re very important to the SUCCESS of our Country, but now, they can get Financing, and they have to start building Homes. They’re sitting on 2 Million empty lots, A RECORD. I’m asking Fannie Mae and Freddie Mac to get Big Homebuilders going and, by so doing, help restore the American Dream!

There’s a lot to unpack there. And most news outlets are doing exactly that, mostly in critical ways.

Even the conservative-leaning Newsmax immediately questioned whether homebuilders “would actually be interested” if Trump got Fannie Mae and Freddie Mac to speed up loan processing on housing construction.

The press has every right to wonder. It’s just that none of the news stories I saw on the subject mentioned the Buffett factor.

I have no idea whether the “Oracle of Omaha” only bought homebuilders because mortgage rates were supposed to fall… or if he somehow knew that Trump was about to get involved. But I’m more than willing to revisit the homebuilder situation today.

And even though I’ve been skeptical of the homebuilders in general, there is one name that I like and have even recommended.

It’s a Mighty (Green) Brick House

In December 2024, I launched a service called Wide Moat Confidential. It specifically focuses on smaller-cap stocks that are targeted to grow by 40% annually at a minimum.

So far this year, I’m proud to say that we’ve generated solid results across various sectors. That includes auto-parts chains, restaurants, commercial real estate (“CRE”), grocery stores… and homebuilders.

I usually don’t reveal those stock recommendations here on Wide Moat Daily. But emerging details about “the American Dream” have me looking even harder at my February pick, Green Brick Partners (GRBK). Paid-up subscribers can read that issue here.

This homebuilder got its name from co-founders David Einhorn – who runs the renowned firm Greenlight Capital – and Jim Brickman, who has more than four decades worth of experience in real estate investing.

Again, Green Brick is a smaller-cap company, with a market cap that’s just over 3 billion. That’s nothing compared with the national homebuilders Trump was talking about, like PulteGroup (PHM) with its $25.57 billion or D.R. Horton (DHI) with $48.05 billion.

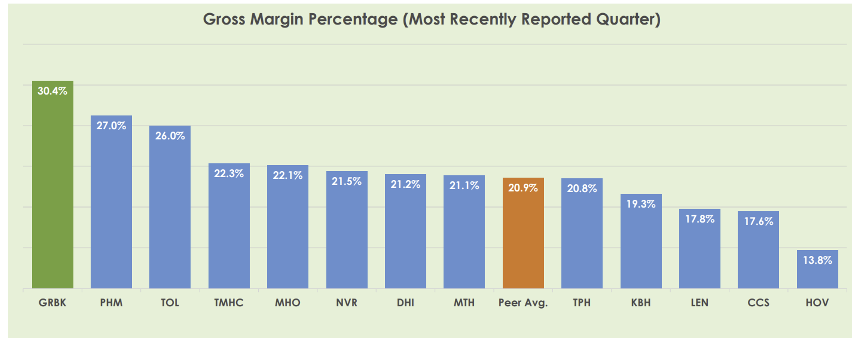

Even so, Green Brick has carved out some unique competitive advantages that have enabled it to generate industry-leading profit margins of over 30%. That bests even Toll Brothers (TOL), which is widely considered to be the “gold standard” homebuilder performer.

Source: Green Brick Partners

One factor that helps Green Brick achieve those results is that it operates in some of the hottest housing markets… from Austin, Houston, and the Dallas-Fort Worth area of Texas, to Atlanta, Georgia, and Florida’s Treasure Coast.

It’s considered a “sharpshooter” in these markets since it builds primarily in “infill” (undeveloped land in urban settings) and infill-adjacent locations, where supply is more constrained.

In other words, the company doesn’t generally take on one or two massive, hundred-acre projects. They take on several very targeted projects.

This requires extensive local knowledge to address more complicated entitlement, regulatory, and development processes – all of which Green Brick consistently displays.

The homebuilder has its own “land bank” database of lots, which allows it to purchase them more cheaply as they become available. As I explained in Wide Moat Confidential, “This provides Green Brick with a lower cost of capital advantage” since outside land bankers would “charge builders equity-return interest rates and substantial earnest money deposits” for their help.

More Things to Like About Green Brick

As a real estate developer myself back before I became a Wall Street writer – though on the CRE side – I can easily recognize Green Brick’s strengths. I like how it’s mitigating its land exposure risk through disciplined management of entitlements, the use of land and lot options, and other flexible land-acquisition arrangements.

Essentially, this homebuilder is actively involved in every step of the land entitlement, home design, and construction processes. And that commitment shows throughout its business.

At the end of the second quarter of 2025, Green Brick grew its total lots owned and controlled by 21% year over year to 40,200. It owned over 35,000 of those on its balance sheet, with approximately 5,000 controlled.

Source: Green Brick Partners

I’ll also point to Green Brick’s low leverage. At the end of the second quarter of 2025, its net-debt-to-total-capital ratio was just 9.4%. And its debt-to-total-capital ratio was 14.4% – the lowest level since 2015 and among the best of its small- and mid-cap public homebuilding peers.

As I explained in Wide Moat Confidential:

The co-owners of Green Brick recognize that excessive leverage is the reason for the trouble during the Great Financial Crisis. And as a result, they understand that Green Brick’s financial strength gives it ample flexibility regardless of the housing cycle.

When I initiated research on Green Brick early this year, shares were trading at 7.4 times earnings, which was below the sector average of 8.3 times. Today, they’re at 10.7 times and have outperformed all their homebuilder peers year to date, up 24% (or 36% annualized).

(Note: In the chart below, “YTD” stands for “year to date.”)

Source: Wide Moat Research

I’m still a very big fan of Green Brick, especially now that both Buffett and Trump have shown such interest in homebuilders as a whole. However, given that pricing level – and the pricing level of the sector in general – I would wait for a pullback before jumping in.

While you do, there is another angle to approach the return of the American Dream. Make sure to read tomorrow’s Wide Moat Daily to get the details.

Happy SWAN (sleep well at night) investing!

Regards,

Brad Thomas

Editor, Wide Moat Daily

|