Happy Saint Patrick’s Day to one and all!

You may very well be wearing green for the occasion. Perhaps you’ve toasted good fortune to friends or family. Maybe you’ve even bought a lottery ticket or two? (The ones with the leprechauns printed on them, of course.)

It’s all good fun… or at least it should be. It becomes something very different if we’re actually staking our future happiness on mere luck, which is about as fickle as it can be.

We’d all love to find a pot of gold at the end of the rainbow. But great results rarely come from chance. Instead, they come from a continuous commitment to research and discipline.

This is true with relationships. It’s true of careers. It’s true of hobbies. And it’s true in the markets as well.

It might look like stock prices move less on logic and more on practically unpredictable emotion. But that’s if you’re watching it with a short-term mindset.

So-called day-trading rarely works out. And when it does, it’s a high-stress life that might not be worth it anyway.

What’s much, much more consistently worthwhile is investing in wide-moat companies: businesses that can protect their profits and reputations year in and year out regardless of what “luck” does or does not come their way.

These companies don’t wait for rainbows to appear; they amass their own pots of gold, all while constructing solid safety nets around them. Their moats can consist of anything from timeless brands to cost advantages or proprietary technologies.

Essentially, these companies are castles built on bedrock rather than sand. Which is why they tend to reward investors over the long term instead of just one chancy day of the year.

The Real Saint Patrick’s Day Approach

Co-authors Chris Zoona and James Allen write in their book, Repeatability: Build Enduring Businesses for a World of Constant Change, that:

Successful companies endure by maintaining simplicity at their core. They don’t stray from or regularly discard their business model in pursuit of radical renovation. Instead, they build a repeatable business model that produces continuous improvement and allows them to adapt without succumbing to complexity.

This isn’t to say that luck never factors into a quarterly result here or there – whether the good kind or the bad. Only that wide-moat companies stay standing years and even decades later regardless of chance.

Take Coca-Cola (KO). It doesn’t sell so many beverages because it’s lucky; it succeeds because its brand and global scale form layers of defense that are almost impossible to breach.

Or there’s Visa (V). It isn’t the largest payment network because mere fortune smiled on it. Visa worked hard to establish its enormous infrastructure and gain equally impressive consumer trust.

And it jealously guards those moats today.

It’s that mentality – and effort – that Wide Moat seeks to invest in. The result is that we benefit from enterprises with disciplined management that produce durable demand, growing cash flow, and strong returns on capital.

Moody’s: A Wide Moat ‘Lucky’ Charm

One wide-moat company I’m monitoring today is Moody’s (MCO).

Together with S&P Global (SPGI), Moody’s forms a global credit ratings duopoly that is hard to beat. While the company itself could theoretically ruin its reputation internally, it has an often captive client base that’s almost guaranteed since bond issuers are often outright required to obtain ratings from these two.

And these ratings are not free. In fact, they’re how Moody’s and its main competitors make most of their substantial revenue.

Another “moat” advantage is Moody’s strong, asset-light balance sheet. This reflects its status as a high‑margin, data- and intellectual‑property‑driven business.

Better yet, Moody’s has modest leverage of 2 times earnings before interest, taxes, depreciation, and amortization (“EBITDA”)… and investment-grade credit ratings of its own with an A- from S&P and A3 from Fitch.

Its operating cash flow consistently exceeds $2 billion annually, which easily covers dividends and debt service. Moody’s has actually maintained a payout ratio of around 30%. And it grows that dividend by an average rate of 10% annually.

Importantly, Moody’s has increased that dividend for 17 consecutive years. That’s still eight years short of being a Dividend Aristocrat, but it’s still nothing to sneeze at.

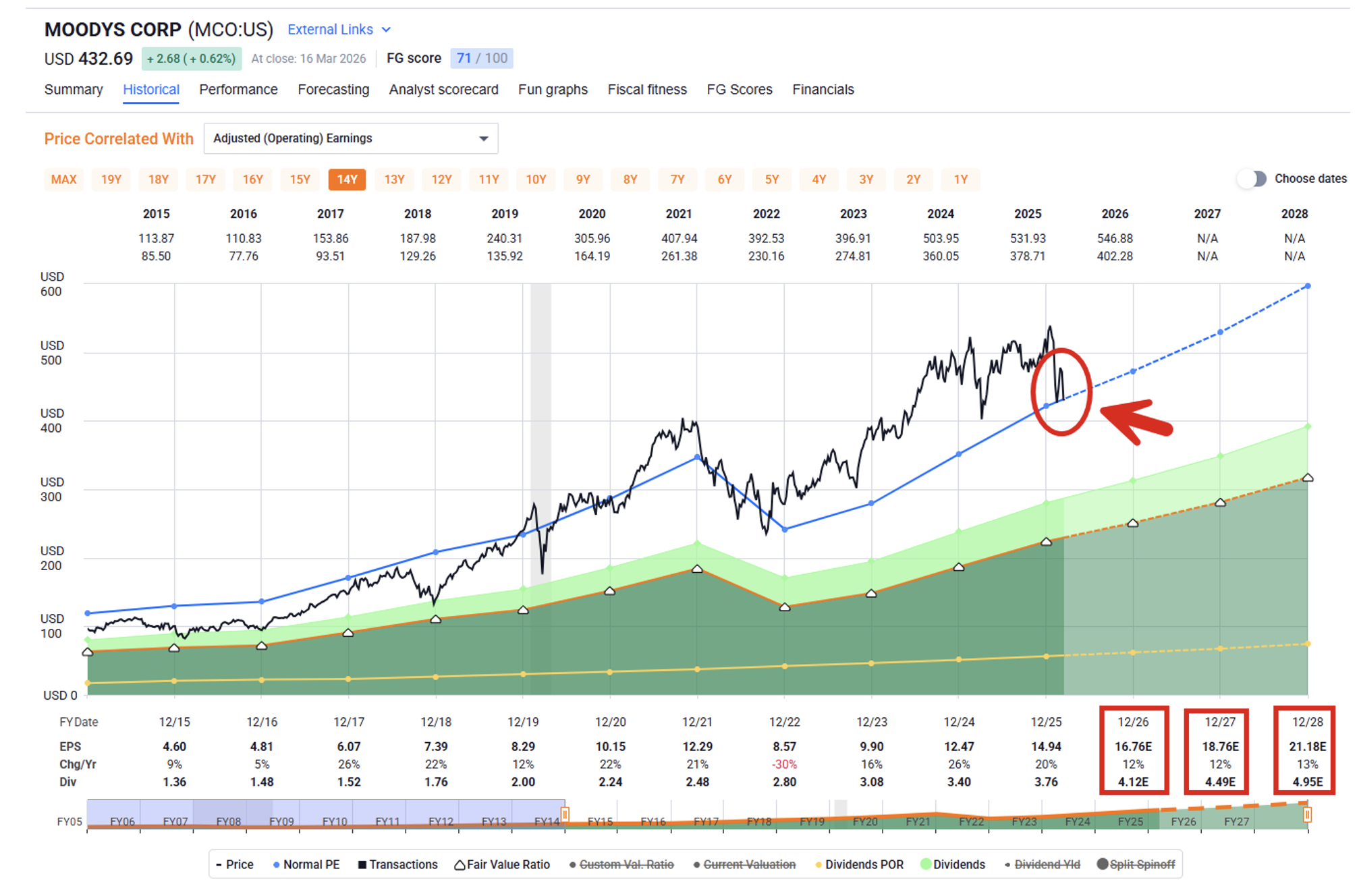

Source: FAST Graphs

As you can see, Moody’s is now trading at fair value with a price of $432.69 and a price-to-earnings (P/E) multiple of 28.3 times. Its dividend yield is just around 1%, so hardly the most impressive percentage ever. However, analysts expect growth of 12% in 2026, 2027, and 2028.

Altogether, Moody’s stands out as a rare combination of stability, scalability, and trust. Its credit‑ratings duopoly, expanding analytics platform, and data‑driven business model have built a moat that’s deep and durable, generating cash flow that grows through nearly every cycle.

Long‑term-minded investors don’t have to worry about luck here. Investing in Moody’s is taking a stake in the infrastructure of modern capital markets.

So, this Saint Patrick’s Day, raise a glass to luck should you so choose. But when it comes to investing, you’re much better off if you act like it doesn’t exist at all.

Regards,

Brad Thomas

Editor, Wide Moat Daily

|