The “Silver Tsunami” is well underway…

The term was first coined in the early 2000s as the Baby Boomer population – those born between 1946 and 1964 – drew closer to their 60s. Since there were a whopping 79.6 million such individuals living in the U.S. at the time, the idea was we would see an increased need for medical care as they entered their “silver” years.

And boy, was that idea correct.

As of 2022, adults aged 65 or older made up 17.3% of the U.S. population. In another 15 years, that figure is expected to hit 22%… which amounts to more than 80 million people.

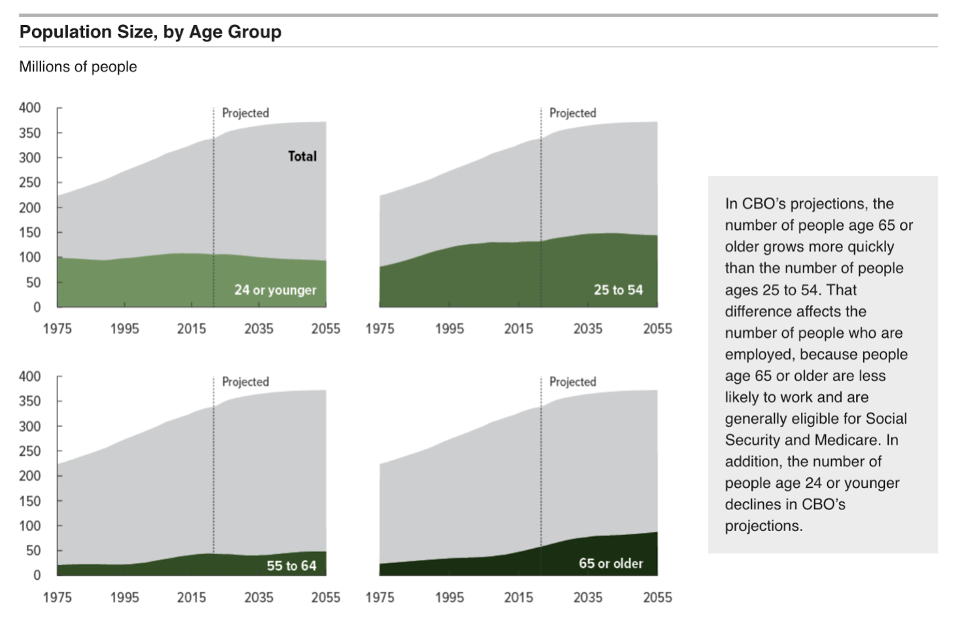

The Congressional Budget Office (“CBO”) comes to similar conclusions. As you can see in the next chart, the population size for most age cohorts is expected to plateau through 2055. The number of young people is actually expected to fall. But the 65-plus group is going in only one direction – up.

Source: CBO

According to AARP, nearly 10,000 Baby Boomers cross the 65-year-old threshold every single day. And the economic implications of this shift are obvious.

Older adults already account for more than half of global health care spending. The older we get, the more our bodies break down. The more our bodies break down, the more we need treatments to keep us going.

Expensive treatments.

In short, America’s Baby Boomers are either in or entering the most medically expensive years of their lives. That should signal a boon for one corner of the real estate market.

In fact, we’re already seeing it…

Health Care REITs Are Right There for the Taking

There’s are certain commercial real estate (“CRE”) companies that know precisely how the Silver Tsunami can generate significant shareholder value. And many of them are conservatively managed, sustainably growing, dividend-paying real estate investment trusts, or REITs.

In 2025, REITs as a whole had an underwhelming year. But health care was the exception. Health care REITs returned an average 24% over the past 12 months.

And those holding senior housing specifically? They returned over 44%.

One name I remain impressed with is Welltower (WELL). As a leading health care REIT, it holds over 2,000 senior and wellness housing communities throughout the U.S., U.K., and Canada.

The company returned more than 50% last year due to robust adjusted funds from operations (“AFFO”) growth of 20% in 2024 and 23% in 2025.

I’ve noted repeatedly how many REITs handled themselves so well despite the elevated rate environment they had to operate in. But Welltower still stands out with its disciplined approach to capital allocation, maintaining its A- rating from S&P and A3 from Moody’s.

Welltower also stands out for its technological advancements, where its software has helped it become an employer, partner, and investor of choice.

That’s a topic that I hope to cover soon. There are certain REITs that stand out for their AI-enriched platforms. And while Welltower certainly makes the cut there, it’s hardly alone.

Silver Tsunami Pick No. 1: Healthpeak Properties

All the same, I wouldn’t rate Welltower as the best Silver Tsunami-specific REIT out there right now. Its shares have, after all, already gained a lot, which means its investors have already achieved a good chunk of its near-term potential.

Healthpeak Properties (DOC), however, still has plenty of room to run. Another health care REIT, it owns a portfolio of 673 properties that include:

-

524 outpatient medical office buildings (“MOBs”)

-

115 life-science properties

-

15 continuing care retirement communities

-

19 senior housing joint ventures

It needs to be noted that health care delivery continues to transition to outpatient care. This is less expensive for payers, more convenient for consumers, and more profitable for providers. So Healthpeak’s impressive MOB portfolio has served it well.

Those 524 properties keep generating robust leasing volumes, releasing spreads, and tenant retention – all of which drives equally notable earnings growth. Healthpeak’s year-to-date leasing volumes totaled 3.2 million square feet with total occupancy that rose 10 basis points (“bps”) to 91%.

The life-science sector is, admittedly, dealing with oversupply issues, as I noted last month while addressing Alexandria Real Estate’s (ARE) dividend cut. So Healthpeak’s share price may very well have grown less than it could have because of that segment of its portfolio.

Fortunately, Healthpeak didn’t participate in that overbuilding. It’s actually maintained solid life-science releasing spreads and tenant retention, with year-to-date leasing volumes totaling 1.1 million square feet and total occupancy of 81% as of the third quarter of 2025.

Healthpeak also maintains a strong capital structure. Its net debt to earnings before interest, taxes, depreciation, and amortization (“EBITDA”) was 5.3 times at last report. And it had $2.7 billion of liquidity.

The company also maintains a conservative payout ratio of 72%, which suggests it’s likely to increase its dividend from here.

Shares are now trading at 9.7 times, well below their normal price-to-AFFO (P/AFFO) multiple of 16 times. Although not an apples-to-apples comparison, Welltower trades at over 44 times.

Healthpeak’s dividend yield is a juicy 7.4%, and we believe shares could fetch $21 by the end of this year. If so, that would mean a 30% total return.

Silver Tsunami Pick No. 2: Equity Lifestyle Properties

My second pick isn’t in the health care sector at all, admittedly. Yet Equity Lifestyle Properties (ELS) still has all the Silver Tsunami drivers powering it to make it very attractive.

Its portfolio consists of 455 properties comprised of manufactured home (“MH”) communities, recreational vehicle (“RV”) resorts, campgrounds, and marinas across North America. Equity especially focuses on coastal and Sun Belt retirement destinations…

The very places where Baby Boomers tend to make up large swaths of the market.

Over 70% of its MH properties are age-qualified or otherwise have average resident bases over 55. In fact, nearly 50% of its overall MH residents are aged 70 or older.

That’s because the manufactured home business model runs on affordability. Whether buying or renting, these properties provide greater value than traditional options.

Equity Lifestyle’s renters pay about 20% to 25% less per square foot than the average two-bedroom rentals around them. So, again, it’s ideal for senior citizens living on fixed incomes.

Pair that Silver Tsunami appeal with limited manufactured housing development over the past 20 years. Big landlords and the politicians they fund tend to be against building new MH communities, which keeps the supply low.

That’s an obvious strategic advantage for Equity Lifestyle.

In terms of its balance sheet, the REIT is in great shape. It has no secured debt maturing before 2028, and its weighted average maturity for all debt is almost eight years.

Meanwhile, its debt-to-EBITDAre (EBITDA for real estate) is 4.5 times – with over $1 billion of capital from its combined line of credit and ATM programs.

Shares are attractive to buy today, with a P/AFFO multiple of 23.1 times compared with its normal 27.4 times. Equity’s dividend yield is 3.5%. Plus, it has an impressive history of growing that dividend by around 11.4% per year over the past decade.

I could see shares hitting $71 by year end, which would result in 25% annualized returns.

The Silver Tsunami promises to be a decades-long trend. For an investors looking to gain exposure, these are a solid few options to begin your research.

Regards,

Brad Thomas

Editor, Wide Moat Daily

|