We’re just two weeks out from the Federal Reserve’s next policy meeting on December 9 and 10. And everyone’s debating what America’s central bank will do.

Will rates fall again, or won’t they? That is the question.

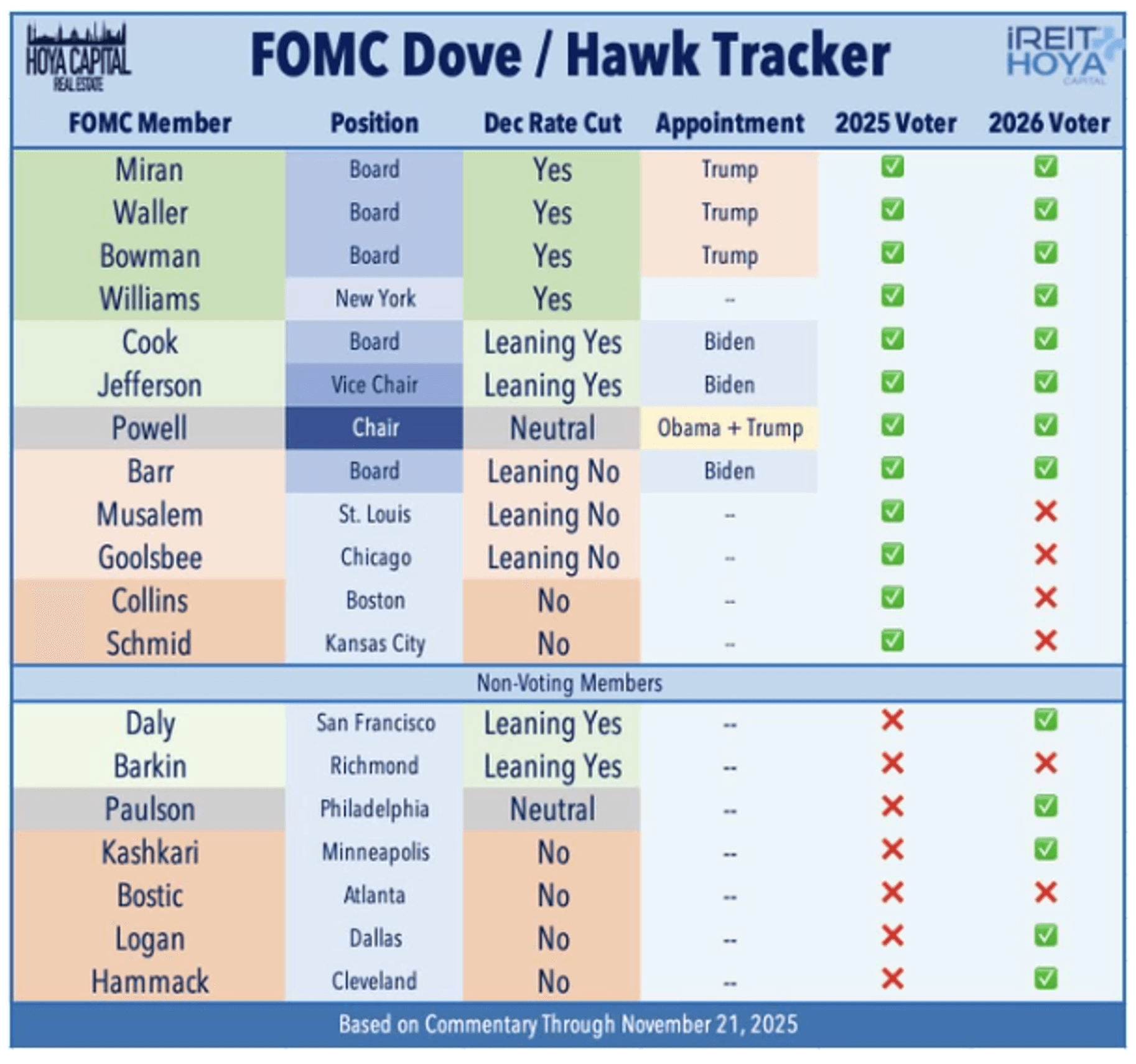

Chairman Jerome Powell recently said it was “far from” a foregone conclusion that we’ll see a third cut this year. It turns out that Fed voting members are exceptionally and abnormally divided on the issue.

Four seem inclined to take rates down a final time this year. Another two appear to be leaning toward a cut, while five others want to hold rates steady.

Source: iREIT® + HOYA

HOYA Capital Real Estate’s Alex Pettee points out how “the likely swing votes on the committee appear to be Lisa Cook and Jay Powell – the very officials the president has called on to resign.”

But even setting aside that complication, most Fed officials do seem to be anxious about inflation. While Consumer Price Index (“CPI”) readings are down from the near double-digit growth we saw in 2022, inflation is still on the warmer side with a topline figure of 3% according to the latest data. That’s still well above the Fed’s stated target of 2% annual inflation. As a reminder, the Fed would typically combat inflation by keeping its rate on the higher side.

At the same time, the Fed is acutely aware of the cooling labor market, which Jerome Powell described as “less dynamic and somewhat softer” in a speech last month. That’s central banker speak for “not great.” And the usual remedy for that malady is lower rates.

In essence, the Fed is between a rock and a hard place.

And on top of all that, the situation is complicated by last month’s government shutdown that led to delayed economic data reports. The employment statistics for October and November, for instance, will be rolled into one report and won’t come out until December 16. And the November consumer price data is due two days later.

This leaves the Fed to make an interest-rate decision at its December meeting with less information than usual. All of which makes it trickier to discern what will happen to real estate investment trusts (“REITs”) from here.

Trickier, but not impossible. Thankfully, there are still plenty of clues we can factor in.

Evaluating the Fed-REIT Relationship in Depth

Let’s begin with the disappointing reality that rates have already been cut twice in the past few months… yet REITs have hardly budged.

Their shares are traditionally handicapped in high-interest-rate environments because of the misconception that they automatically suffer under those conditions. Against this backdrop, and in the wake of the recent quarter-point cut, Cohen & Steers decided to take a closer look at several notable data points.

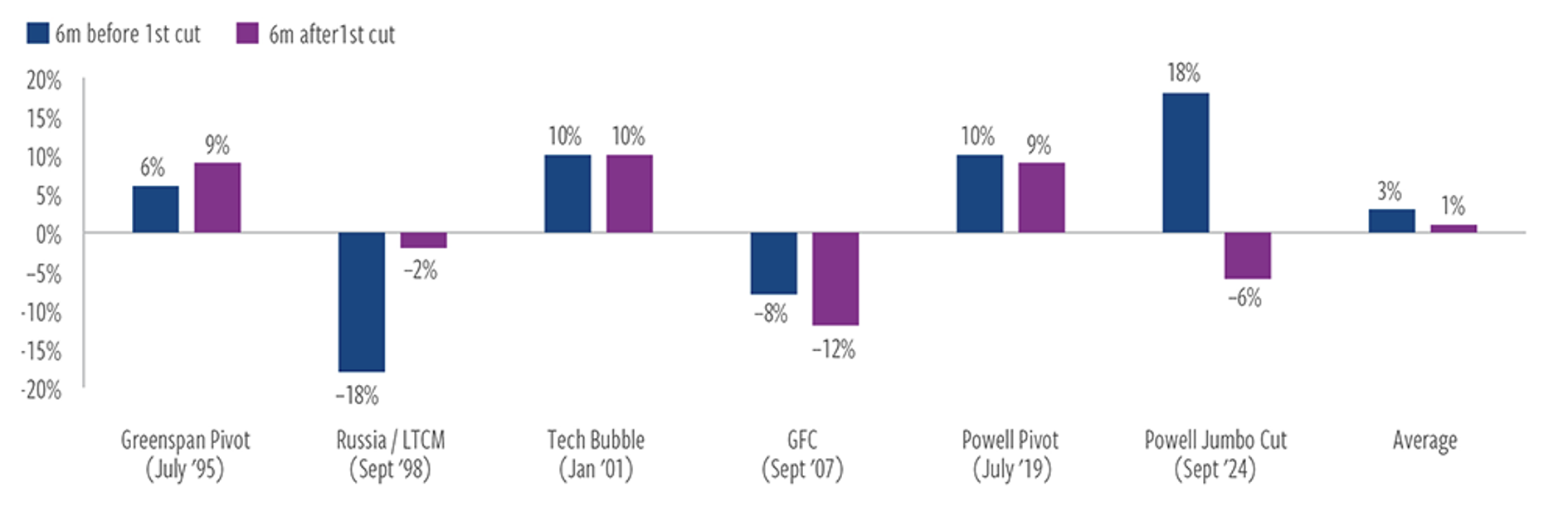

“While every cycle brings with it idiosyncrasies,” it notes, “an examination of past Fed rate-cutting periods indicates REITs have performed well when the Fed starts easing. And given the Fed’s efforts to telegraph policy changes, it is not surprising to see REIT performance in the six months prior respond positively in most instances.”

Take last year, where REITs gained 18% in the six months before the Fed cut interest rates that September. However, Cohen & Steers goes on to say, “While the change in interest rates is important, arguably more significant is the change in real rates – i.e., rates adjusted for inflation.”

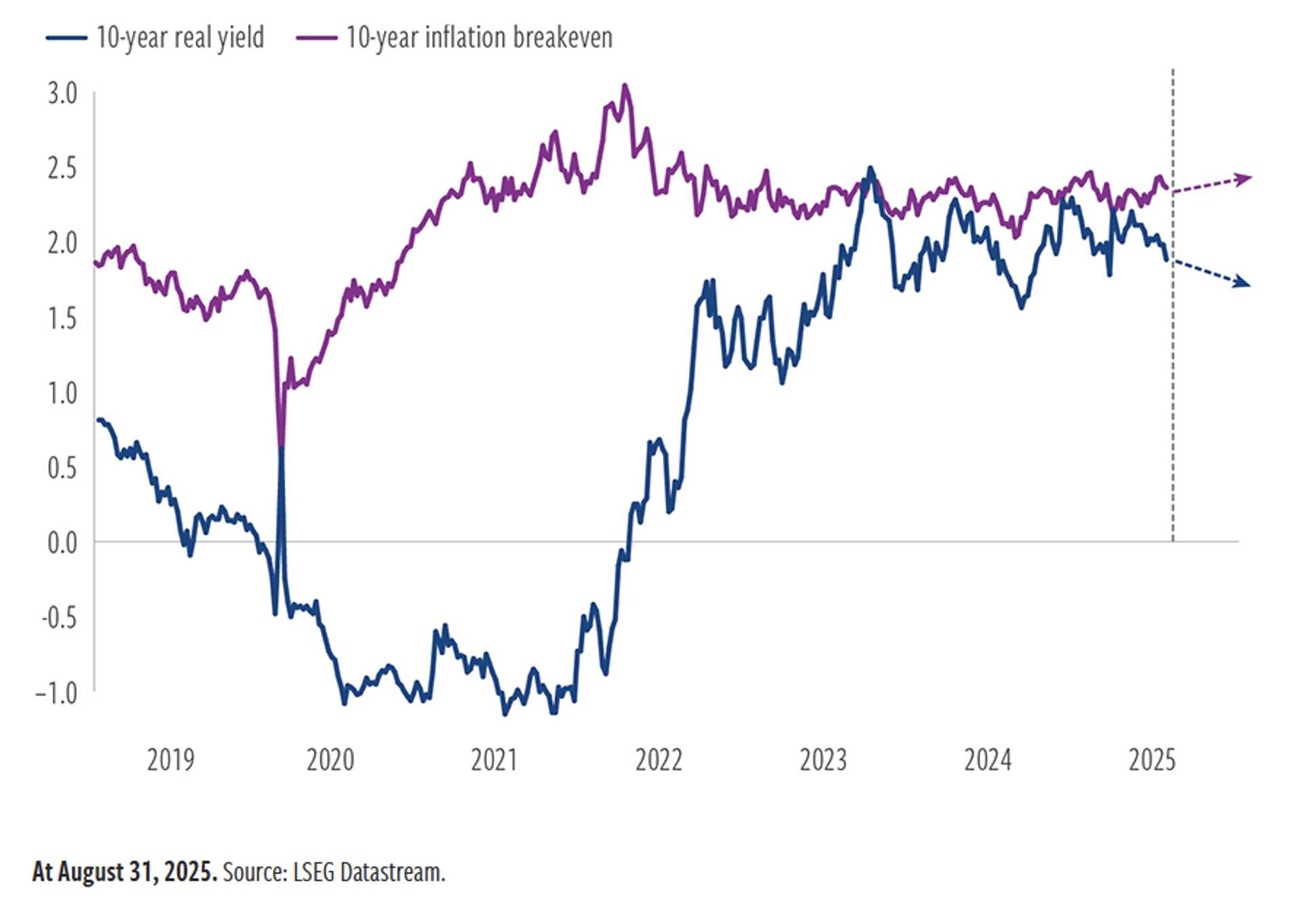

Keep in mind that we saw a total of 10 rate hikes in 2022, which resulted in a much higher cost of capital. And that:

This drove a sharp repricing in commercial real estate (CRE) values, first in the listed markets and then in the private markets (33% and nearly 20% declines, respectively, peak to trough).

The bulk of the change in rates occurred in real rates, which rose from -1.0% to 2.5%, while inflation expectations (expressed by 10-year inflation breakevens) remained muted.

Breakeven inflation rates, as explained by the U.S. Treasury, “are future inflation rates embedded in the Treasury securities market.” They “pertain to inflation of the (not seasonally adjusted) Consumer Price Index for All Urban Consumers (CPI-U).”

In the past, it was the combination of rising real rates and flat or falling inflation that has really presented a problem for commercial real estate values. Therefore, Cohen & Steers continues:

It was that dynamic that drove repricing in both listed and private real estate. Cap rates increased without the offsetting rent growth projections that typically accompany higher inflation expectations.

We’re now seeing a reversal of those trends, however. Real yields have fallen to 1.7%, which is 70 basis points (bps) below their 2023 peak, while inflation breakevens are trending higher.

Cohen & Steers “believes real yields will continue to decline, while fiscal and monetary policy – and rising price pressures – will drive inflation expectations higher.”

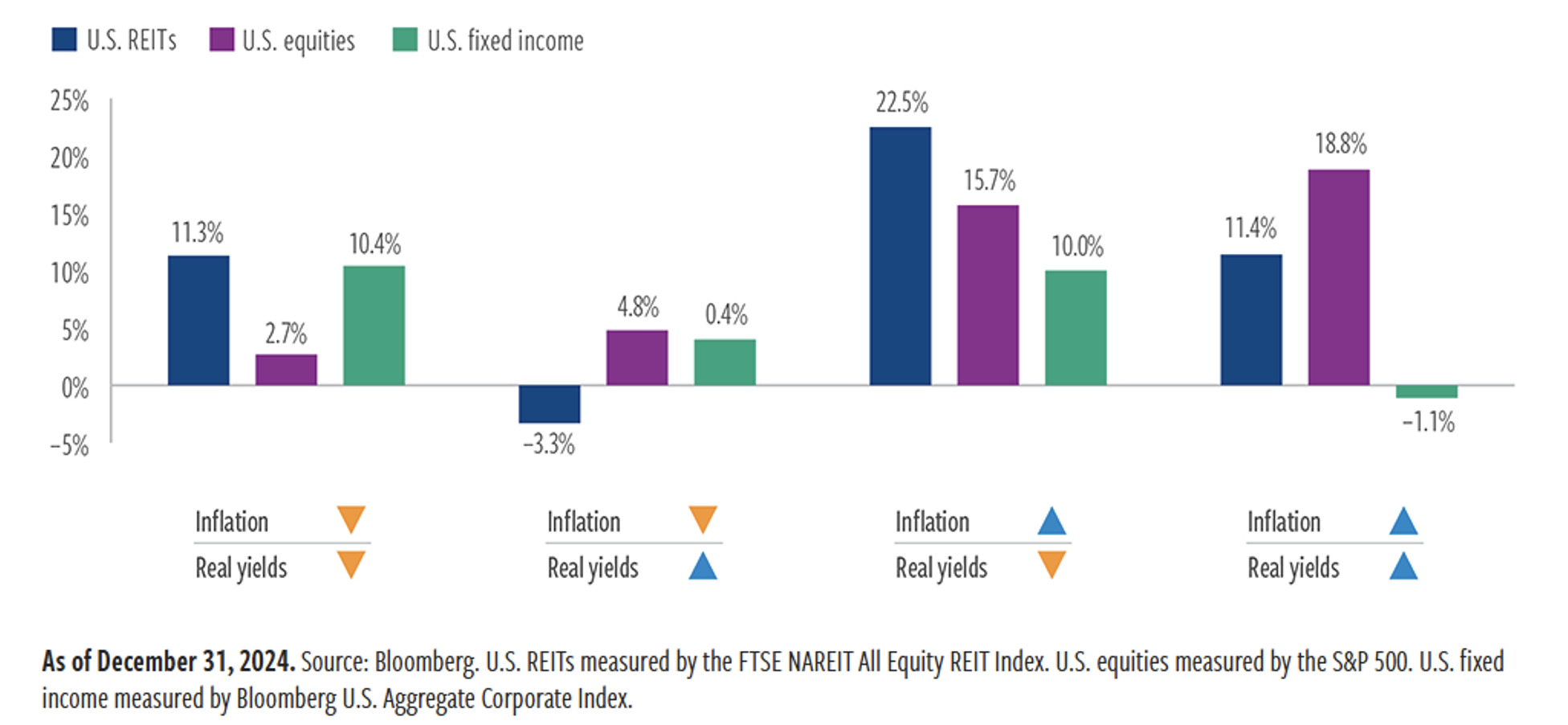

Again, this is usually exactly what we want to see for REITs. Since 1997, listed real estate has outperformed U.S. equities in such environments 22.5% to 15.7%. Whereas the past three years’ worth of rising real yields and falling inflation breakevens tend to be pretty painful.

Today’s Bottom REIT Line

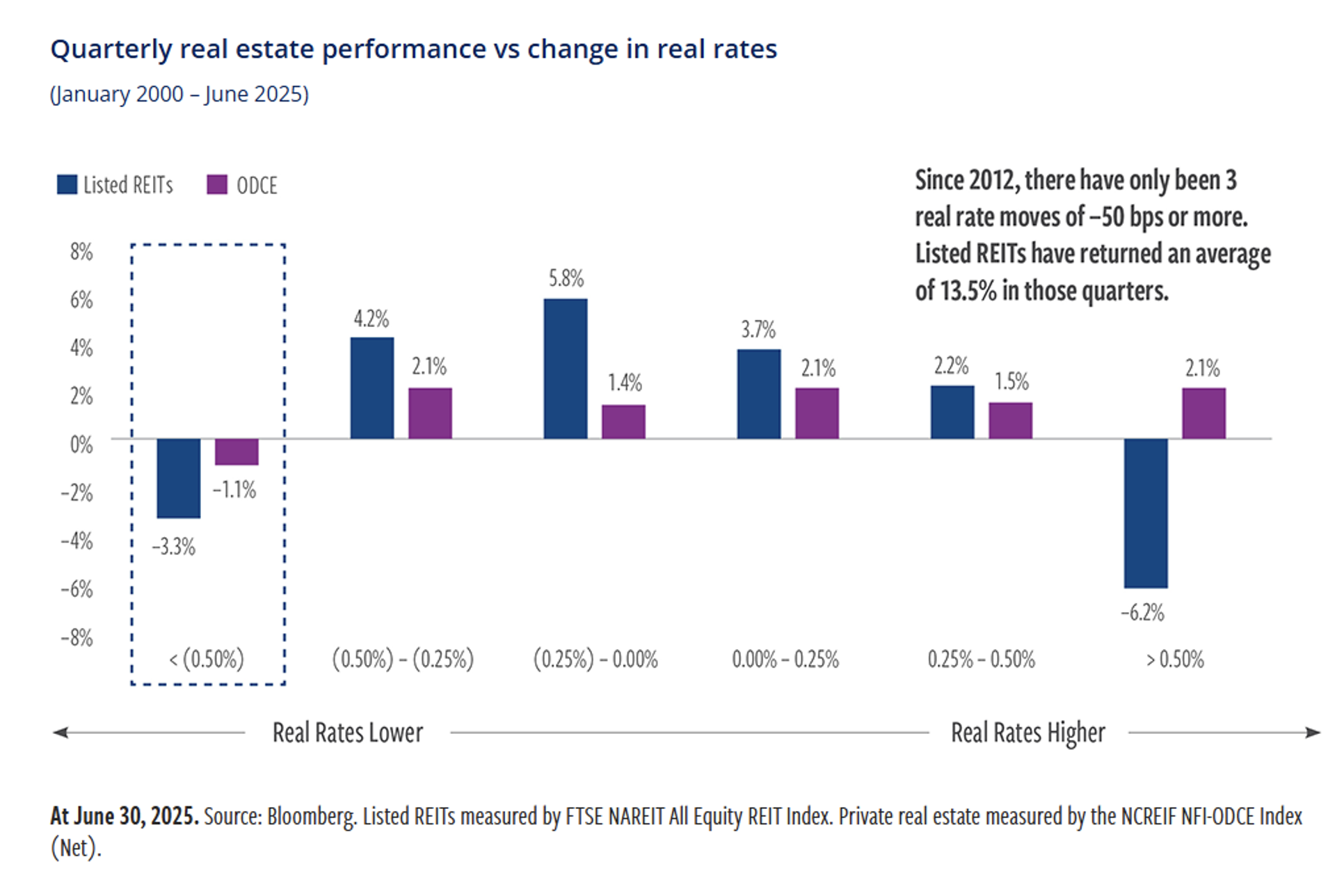

We also need to recognize that REIT share prices really haven’t yet benefited from the drop in real rates.

They normally perform well when real rates fall between 0 and 50 bps, it turns out. (Anything above that tends to indicate real economic issues that are much harder to work with.) However, that just hasn’t been the case recently, as you can see below:

Perhaps that’s because the economy is still working out all those pandemic-era effects, including changes to e-commerce and remote work. While we’re returning to a balance nowadays, we’re still not where we once were.

Will we ever be? Maybe not totally. But as investors begin to focus on 2026 and 2027, I agree with Cohen & Steers that:

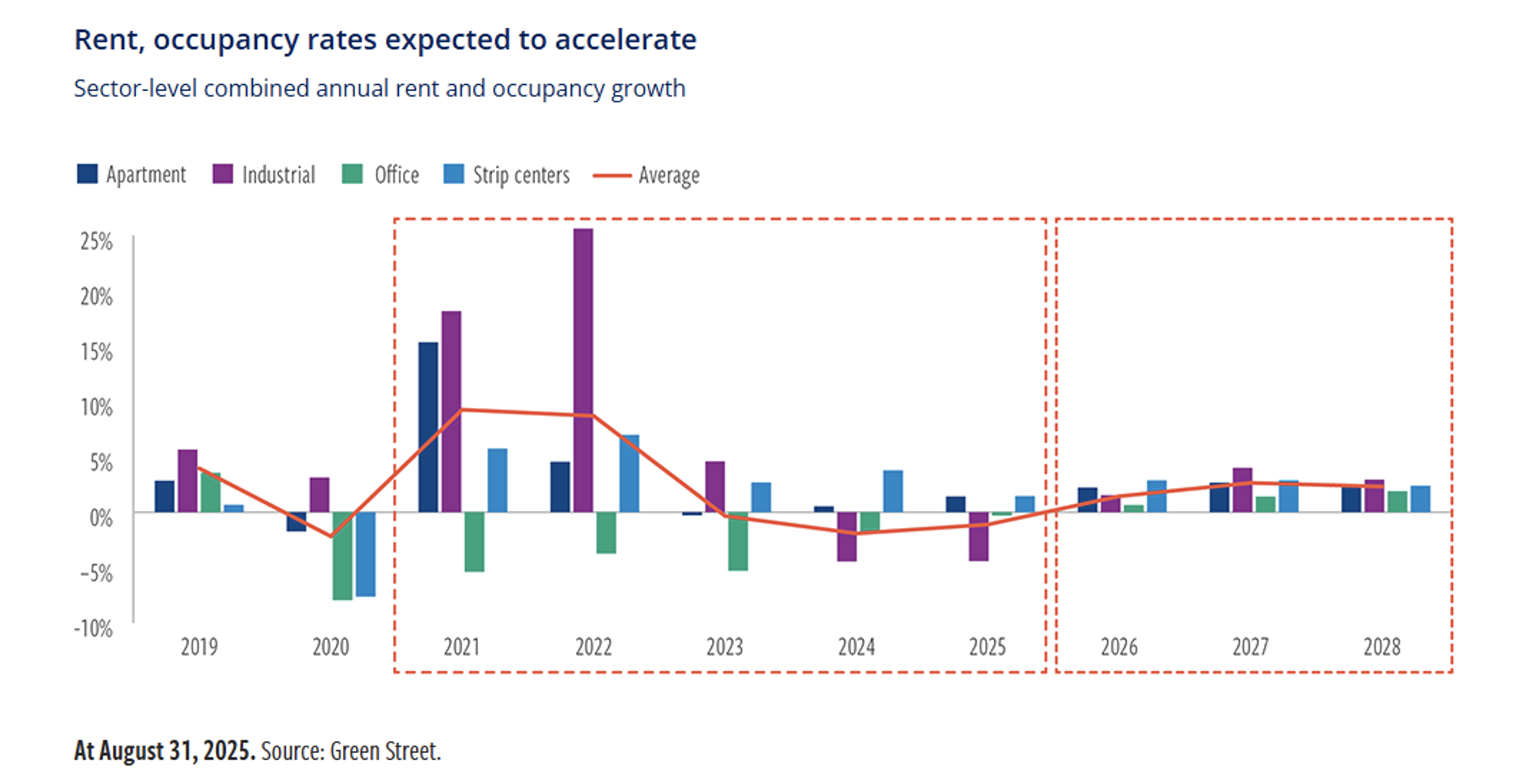

… operating fundamentals will reaccelerate and provide greater supply/demand balance, with an acceleration in rent and occupancy growth.

We expect listed REIT earnings growth to see a similar acceleration, from 3.3% this year to 7.6% next year and 7.5% in ’26 and ’27, respectively. That clarity should serve as a near-term catalyst for performance in the listed market.

My regular readers know I hold many REITs in high regard one way or the other. They’ve been navigating these tough times beautifully, maintaining healthy balance sheets and even raising their dividends along the way.

So, I’m happy holding them regardless. However, if we can get some share price appreciation sometime soon on top of those dividends…

Then that’s definitely something to look forward to as we close out the year.

Regards,

Brad Thomas

Editor, Wide Moat Daily

P.S. Stay tuned for a special announcement I’ll be making on December 5 – just days before the Fed announcement. This could be one of the most important news events I’ve spoken on in my 30-plus year career as a real estate investor and Wall Street writer.

|