I’m down here in sunny, opportunity-laden Florida this week for a whole host of reasons – including meeting with two real estate-specific billionaires.

I’m excited about speaking with both men and seeing where their insights and connections can lead. And while I love my home state of South Carolina, it’s great to get out and visit cities like Miami, Delray Beach, and West Palm Beach.

Even if it’s just for business, the sights are impressive to see.

I will admit, however, that my meetings are making me a little nostalgic. Because there’s one man that I won’t have the chance to meet again – Sam Zell.

Source: Brad Thomas

Zell was someone I always looked up to. Hardly your typical billionaire, he was the son of immigrants who put himself through college at the University of Michigan, managing a 15-unit student apartment in exchange for a free room.

This guy really was about as self-made as you can get. That’s probably why he was so… unique… once he graduated and started making a name for himself.

Zell didn’t play by anyone else’s tune.

Over the decades, he purchased properties that nobody else would touch from owners who were desperate to sell. That meant he got them at very, very low prices, then used his expertise and notable willpower to bring them back from the brink of death, often pocketing millions in the process.

That’s how Zell got the nickname the “Grave Dancer.” Designated lost causes simply didn’t scare him. He’d crunch the numbers, assess his resources, and make his move where no one else dared to step.

He passed away in 2023. But the man was a legend with a legacy that’s still well worth studying today.

Architect of the Modern REIT Era

I met Sam Zell in 2021, right after I published my book, The Intelligent REIT Investor Guide – my ticket to sit down with him in person. You see, he had endorsed it, writing:

The simple genius of public [real estate investment trusts, or REITs] is that they turn bricks and mortar into transparent and predictable liquid assets. Since they tend to pay high dividends, REITs can serve as a terrific addition to an investment portfolio. Thomas’ book helps break down this asset class for the average person, making REITs more understandable and therefore more accessible to everyone.

Zell was an absolute expert on them, having even founded two himself, Equity Residential (EQR) and Equity LifeStyle Properties (ELS). He was still chairing both, as well as a third REIT – Equity Commonwealth – when he passed away in May 2023 at age 81.

REIT champion and global education initiative Nareit wrote how:

Zell was also Nareit’s chair in 1999 and 2000, and was a past recipient of Nareit’s Industry Leadership Award. He was a highly vocal and active champion of the listed REIT approach to real estate investment, and the transparency, predictability, and accountability that REITs bring to the industry.

Nareit President [and] CEO Steve Wechsler described Zell as the principal “architect and progenitor of the modern REIT era, with a vision that few had and one that has truly come to fruition.”

Now, none of that chutzpah, dedication, and experience has saved his REITs from suffering the same fate as the rest of the sector. All three saw their shares fall and fall hard during the 2020 shutdowns. All three bounced back in 2021. And all three went right back to being unloved as interest rates moved higher from there.

Equity Commonwealth went on to liquidate its assets earlier this year as part of a planned sale and dissolution approved by shareholders in November 2024. But Equity Residential and Equity LifeStyle Properties are still on the market… and trading at prices I think Zell himself would approve of if he were in our shoes.

As I shared yesterday, I believe we’re in a historic buying opportunity for REITs. And so, I thought we’d look at Zell’s REITs today… and see if it’s time to start dancing.

A Closer Look at Equity Lifestyle

Equity Lifestyle owns and operates North America’s highest-quality portfolio of manufactured home (mobile home) communities, recreational vehicle resorts, campgrounds, and marinas. Altogether, it holds over 173,000 homesites across 35 U.S. states and Canada, with an enterprise value of around $19.7 billion.

One of Equity Lifestyle’s primary “moat” advantages is the underlying demand for real estate – temporary or otherwise – by customers who are vacationing or in retirement. Over 110 of its properties are located on lakes, rivers, or the ocean. And over 70% of its manufactured housing properties are either age-qualified or have a resident 55 or over base.

That makes ELS a beneficiary of the “Silver Tsunami” thesis. That would be the observation that America’s millions of Baby Boomers are aging into their golden years. That means millions of new potential customers for Equity Lifestyle in the years ahead.

Then there’s Equity Lifestyle’s value proposition, which is associated with buying and renting manufactured housing versus traditional housing. The cost to purchase a manufactured home is significantly less than a single-family home… by as much as 75%! And ELS renters pay approximately 20% to 25% less per square foot than the average two-bedroom rental in related submarkets.

Wide Moat Research also likes ELS’ balance sheet. It offers some of the most attractive debt metrics in the REIT sector, with a debt-to-enterprise value of 20.9% and total debt/adjusted earnings before interest, taxes, depreciation, and amortization for real estate of 4.5 times.

In the third quarter, the REIT maintained its full-year 2025 normalized funds from operations ("FFO") guidance of $3.01 to $3.11 per share, with $3.06 at the midpoint. This would represent an estimated 4.9% growth rate over 2024.

As shown below, ELS has maintained very consistent earnings growth of 8% compound annual growth rate (“CAGR”) since 2006. And its dividend growth of 20% CAGR is even more impressive.

Source: FAST Graphs

Based on consensus per-share adjusted FFO (“AFFO”) growth of 5% in both 2026 and 2027… it appears likely that ELS will continue generating steady dividend growth.

In short – as any grave dancer would recognize – ELS is cheap, trading at 24 times, below its normal price-to-AFFO (p/AFFO) multiple of 25.7 times. Its dividend yield is 3.3%, and I suspect shares could return as much as 25% over the next 12 months.

Welcome to Equity Residential

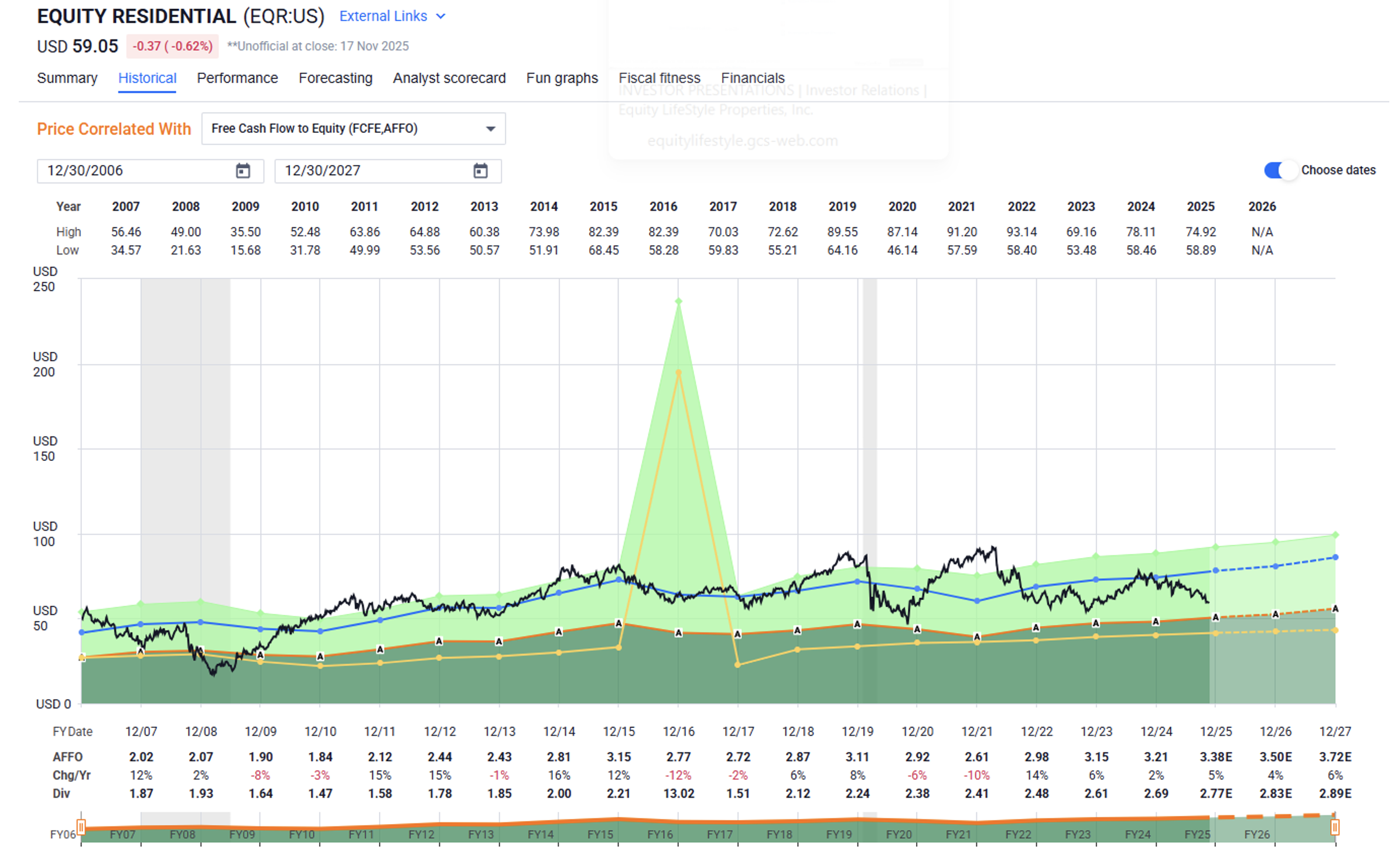

Equity Residential is an apartment REIT that owns 84,648 units in 312 communities in 12 states. With an enterprise value of $36 billion, it splits its investments between lifestyle (52%) and suburban (48%) communities.

EQR has industry-leading credit ratings of A- from S&P and A3 from Moody’s. And its debt metrics reflect its balance sheet strength, with net debt-to-EBITDA of 4.41 times and a 6 times fixed-charge coverage.

This means one of its “moats” is that it boasts the lowest cost of debt capital in the entire REIT space.

EQR recently maintained its fiscal year 2025 FFO per-share guidance at a midpoint of $4.00. It did, however, cut its same-store revenue expectations by 15 basis points (“bps”) to 2.75%. And while it left expenses alone at 3.75%, same-store net operating income is now projected at 15 bps lower to 2.35%.

Even so, EQR has delivered strong and consistent dividend growth of 5.8% CAGR since 2011 – while maintaining a manageable AFFO-per-share payout ratio of 79%. So the fact that shares are in “grave dancer” range, trading at 17.7 times p/AFFO compared with their normal 23.1 times multiple?

Well, they look like a bargain to me.

EQR’s dividend yield is 4.7%, which is a nice consideration in and of itself. Better yet, as new supply pressures ease in 2026, I expect to see it generate returns of 20% or more on an annualized basis.

Source: FAST Graphs

If those two Sam Zell-specific grave-dancing examples intrigue you, don’t forget to watch The Wide Moat Show on YouTube this Thursday. My fellow host and analyst Nick Ward will be helping me disclose a larger list of stocks that have solid fundamentals but bargain-level share prices.

So, here’s to Sam Zell. He built two great REITs in Equity Lifestyle and Equity Residential. I expect great things from them going forward.

Regards,

Brad Thomas

Editor, Wide Moat Daily

|