Compounding.

It has been called “the eighth wonder of the world,” supposedly by Albert Einstein (although that attribution has always been dubious).

But Warren Buffett has definitely encouraged investors to embrace this same concept for long-term investment success.

His late partner, Charlie Munger, echoed the sentiment more than once, warning investors to “never interrupt it unnecessarily.” And Seth Klarman, CEO of hedge fund Baupost Group, described “even moderate [compounded] returns over many years” as being “compelling, if not downright mind boggling.”

The principle of compounding is essentially the intelligent investor’s way of earning returns on both their original investment and the returns from their original investment. When done right, it can add up, helping you to build significant wealth.

There is a catch, though, and that’s how it takes time. A lot of it. This means that compounding as a wealth-building formula is simple, but it isn’t always easy.

There’s always the temptation of getting impatient and opting out of reinvesting to chase the latest investment fad. Or indulging in luxuries instead of reinvesting.

And it can feel overwhelming trying to keep up with inflationary costs while also building up your 401(k), contributing to your kids’ college funds, and/or dealing with unexpected expenses.

Unfortunately, though, even just a temporary pause puts a dent in the compounding process, resulting in less wealth accumulation over time.

You Have to Stick to It

The only way to make the most out of this strategy is to:

-

Invest in a safe, stable, dividend-yielding stock

-

Receive that dividend income

-

Put your dividend income back into the stock

-

Collect even more dividends

-

Reinvest again to get more shares

-

Rinse and repeat

It’s a continuous cycle – one that could make you tens of thousands of dollars… or more.

Now, you can use any steady-as-she-goes dividend-paying stock to cultivate compounding. But naturally, the more often you put money into it, the more often it has a chance to grow – and at a faster rate. That’s why I like monthly dividend-paying assets that continue to intelligently and sustainably raise their dividend payouts.

Consider a hypothetical example: A $10,000 investment yielding 5% will turn into $70,399 after 40 years when compounded annually. But that same investment compounded monthly will become $73,584 over the same period. That’s a non-insignificant difference. Which is why, if you’re going to compound, you might as well do it monthly.

Like the two down below..

Monthly Dividend-Paying REIT No. 1

Agree Realty (ADC) is a net-lease real estate investment trust (“REIT”) that owns over 2,500 properties. Sixty-eight percent of its contracts are with investment-grade companies such as Walmart (WMT), Dollar General (DG), Kroger (KR), and Lowe’s (LOW).

It also owns 232 ground-leased properties, 88% of which are operated by investment-grade-rated customers.

I’ve been covering Agree Realty for over 15 years now. During this time, I’ve watched it transform from a mediocre REIT into a “wide moat” monthly dividend payer with one of the safest dividends around.

One of Agree’s primary competitive advantages is its strong balance sheet. It has a total debt-to-enterprise value of just 28% and a fixed-charge ratio of a very healthy 4.2 times.

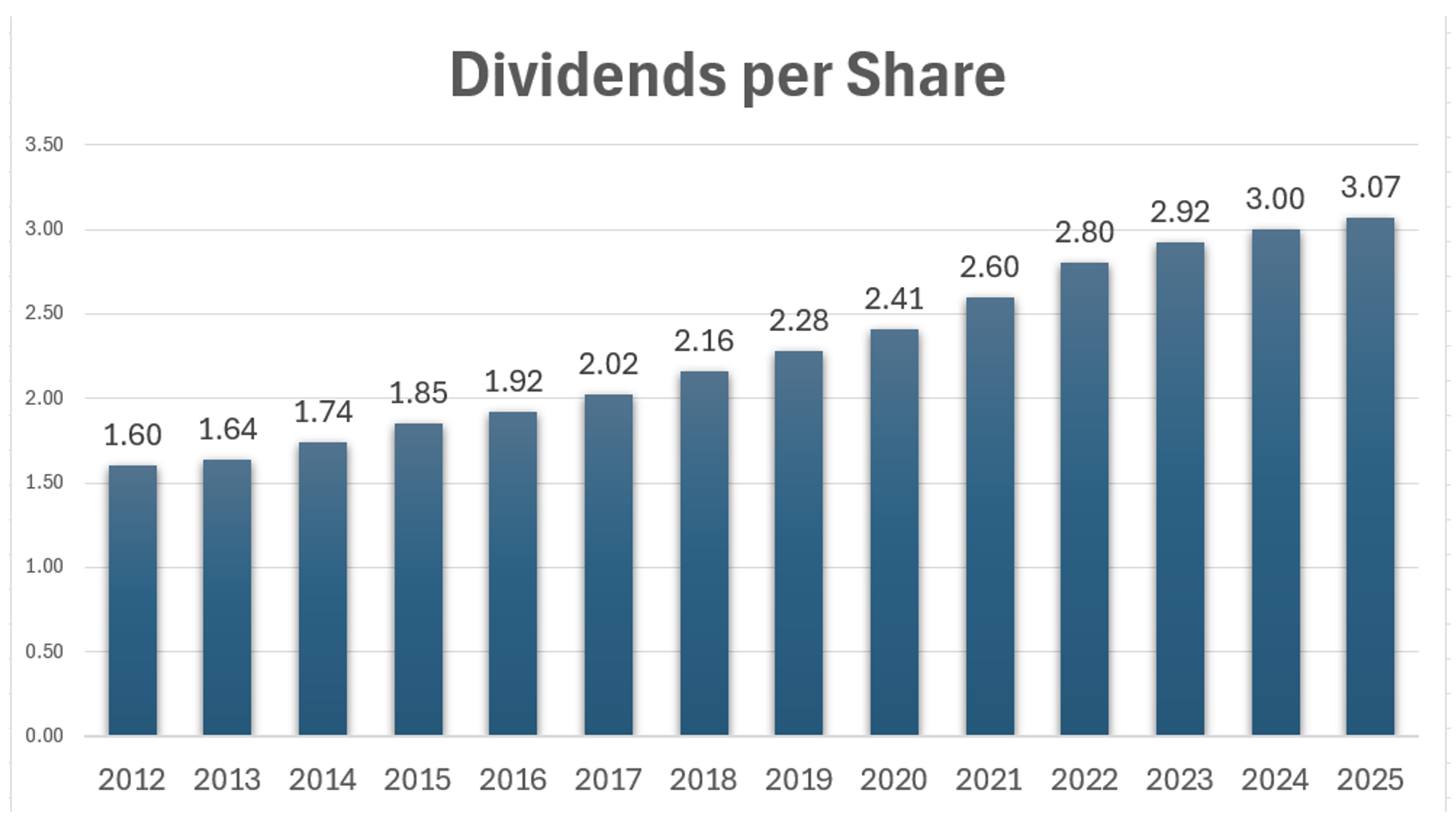

As for its payout ratio, that has been solid, currently sitting at 71% based on adjusted funds from operations (“AFFO”) per share. And its dividend growth has been reliable, averaging a 5% compound annual growth rate since 2012.

Source: Wide Moat Research

Agree’s current dividend yield is 4.3%, and its price-to-AFFO (p/AFFO) multiple is 16.9 times compared with its normal 18 times. Analysts are forecasting 5% growth in 2026 and 2027.

Based on the sum of these parts, I’m forecasting this monthly paying REIT to return around 15% over the next 12 months.

Monthly Dividend-Paying REIT No. 2

Healthpeak Properties (DOC) is health care REIT that owns 703 properties across the U.S. This number comes courtesy of its recent merger with Physician Realty in March, which created a more diverse business model and safer dividend.

Its tenant list consists of medical office buildings, life-science properties, and senior housing. The REIT has over two decades of building relationships with leading health systems and biopharma tenants – like HCA Healthcare (HCA), and big pharmaceutical companies like Novo Nordisk (NVO), Bristol-Myers Squibb (BMY), and Johnson & Johnson (JNJ) – to generate leasing and investment opportunities not available to the broader market.

In short, its lessees fuel innovation in patient care and research by accelerating scientific discovery, enhancing health care delivery, and fostering healthier populations. And that, in turn, drives corporate profits and shareholder value.

The company also has a strong balance sheet rated Baa1/BBB+ with nearly $2.3 billion of liquidity. At the end of the second quarter of 2025, it had net debt to adjusted earnings before interest, taxes, depreciation, and amortization of 5.2 times.

As shown below, Healthpeak has grown AFFO per share by around 5%. And its related payout ratio is 72%.

Source: Wide Moat Research

Analysts are forecasting Healthpeak to grow earnings by around 6% in 2025. But I have to say… I believe the Federal Reserve’s quarter-point rate cut yesterday will spark a return to venture capital funding in the life science sector.

And that could fuel Healthpeak’s growth even further.

Its dividend yield is 6.7%, and shares are trading at 11 times p/AFFO versus its normal 16 times. All things considered, I’m forecasting shares will return 20% or more over the next 12 months.

The Compounding Story Continues

Incidentally, I recently interviewed Healthpeak’s CEO for Wide Moat members, and I remain impressed by its potential. I plan on interviewing Agree’s CEO soon, and I expect my current conclusion will stand there as well.

These REITs are solid considerations for a compounding-focused portfolio.

The act of compounding itself might be about as “boring” a way to get rich as possible. There’s nothing flashy about it whatsoever.

It’s the slow-and-steady tortoise way to run the investment race. So I can’t say you’re going to get much bragging rights at the water cooler for owning monthly paying companies like Agree and Healthpeak.

Then again, we all know that the tortoise wins in the end…

Regards,

Brad Thomas

Editor, Wide Moat Daily