Brad’s Note: Earlier this week, I mentioned I had an announcement scheduled for today. Well, the day is here, and my new presentation is now live. It has to do with a new executive order out of the White House. You see, the Trump administration has thrown its weight behind the build-out of AI infrastructure. And it’s creating opportunities in one corner of the market I follow closely. This may go down as Trump’s final deal, and it could be one for the history books. See the full presentation – and learn which stocks I’m recommending as part of this thesis – right here.

Imagine an investor with 50% of their net worth in a few tech stocks. The rest is scattered across other industries.

That certainly seems like a big bet. The investor must have a lot of conviction in those few tech stocks, right?

In reality, they don’t even know what they own… how much they own… or at what price.

Despite being heavily allocated to one sector, this investor probably thinks they’re very diversified and conservative. After all, they “own the market.”

This is not hypothetical. Nor is it rare. Millions of individual investors do precisely this. In fact, many bank their retirement goals on it.

In today’s edition of the Wide Moat Daily, we’re busting the myth about “owning the market.”

Once I reveal the truth, you’ll finally understand why ultra-high-net-worth investors, endowments, and sovereign wealth funds play a totally different game than your co-workers and neighbors.

Top Heavy

Most people diligently invest into the SPDR S&P 500 ETF (SPY). SPY is one of the most-traded exchange-traded funds (“ETFs”). In essence, it lets you “buy the S&P.” And by owning it, many believe they are investing across the entire U.S. economy.

And that’s true… with one major caveat.

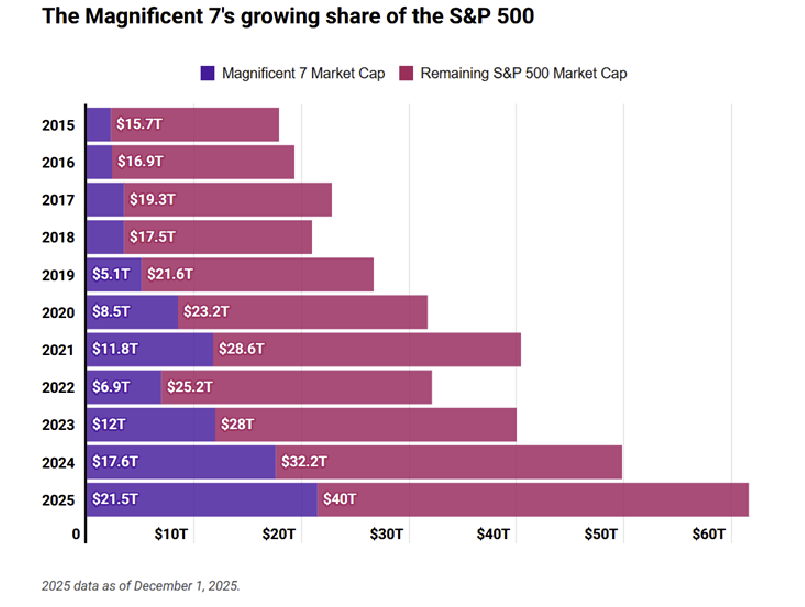

The S&P 500 – and therefore SPY – is very top-heavy.

Source: Motley Fool

The S&P 500 uses a free-float market capitalization method. Larger companies have greater influence and vice versa. That sounds reasonable until you take a close look under the hood.

The market capitalization of the Magnificent Seven is nearly $22 trillion and represents 37% to 38% of the S&P 500. If we add in key companies valued heavily on the expansion of artificial intelligence, like AMD (AMD) and Applied Materials (AMAT), it’s another $5 trillion to $6 trillion. We are now up to roughly 50% of the index.

If companies were instead equal weight (which many investors incorrectly believe is the case), each would be just 0.2% of the index. Yet Nvidia (NVDA), which is only one of the 500 stocks, is 8% to 9% of the index.

The average passive investor isn’t a passive investor at all. They are “all in” on seven mega-cap tech stocks and 16 to 18 supporting AI companies without even realizing it.

Public Stocks ≠ the Economy

In the 1960s, the London Stock Exchange boasted 4,400 publicly traded stocks. Today, it’s barely 1,200 companies. Despite the U.S. economy growing 4 times its size since the early 1990s, the number of publicly traded companies has fallen from a peak of 6,700 to 4,400 today. On the other hand, there are now roughly 19,000 private U.S. companies with annual revenues above $100 million. In fact, it’s estimated that 87% of all companies with revenue above $100 million are privately owned and not traded on any stock market. Apollo Global Management (APO) and Hamilton Lane’s research shows that 90% to 95% of large companies in the U.S. are private.

The vast majority of U.S. companies aren’t accessible through public stocks.

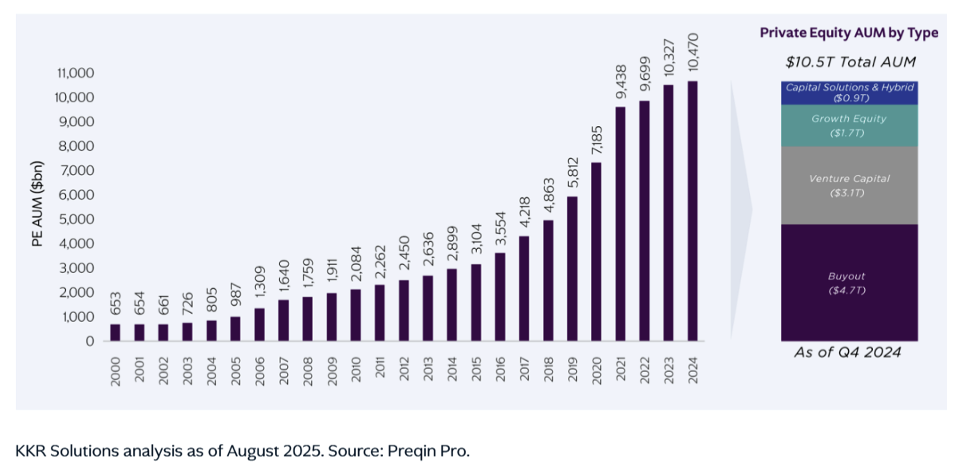

As a direct result, private equity has grown from $653 billion in the year 2000 to over $10 trillion today. For many years now, private firms have generated more capital and job formation than public companies.

Many retail investors hear private equity and think “outrageous fees” or “more Wall Street trickery.” I’m not here to take sides. But the most sophisticated investors in the world have not increased their exposure to private equity by over 15 times in the past 25 years (and beaten the S&P 500 in the process) because they like gambling. It’s the opposite. They increase investment into private equity as more of the economy is tied to those companies.

These firms are doing what most retail investors think they are doing when they claim to “own the market.”

More Than Stocks – and Even Bonds

It’s crystal clear that owning publicly traded stocks alone is not representative of the broader economy. But the extent of how far away most investors are from truly diversifying across the economy is far worse than that.

According to Zillow, the current (2025) housing stock in the U.S. is valued at over $55 trillion. Adding in commercial real estate is another roughly $20 trillion. If you add in other types of real estate, like farmland and timber, it exceeds $100 trillion.

But even without doing that, just residential and commercial real estate are easily the largest category in the U.S. economy. This may not surprise you since many of us have large portions of our net worth in real estate as a result of owning your home. And many of the millionaires in our network did so using real estate.

But you’d never guess that if you just owned the S&P 500, real estate is only 3% of the index. Health care and financial services are 50% larger in the real economy than their proportion of the S&P 500. You get the idea.

The real economy is also heavily dependent on credit to function and grow. That includes direct lending, private loans, asset-backed lending, venture debt, and infrastructure financing. Only a tiny portion of this multitrillion-dollar market is accessible in mutual funds or through the bond desk at your brokerage firm.

Final Thoughts

Public equities, especially in the U.S., are, in many ways, a miracle. Through 401(k)s and IRAs, they’ve helped create a middle class that is the envy of the world. But that doesn’t mean we can’t do even better.

Large financial institutions with armies of skilled investment professionals aren’t allocating to infrastructure, private equity, private credit, and real estate to keep themselves busy.

Malaysia’s Khazanah Nasional was the top-performing sovereign-wealth fund in 2024, generating a 24.6% return. Twenty-five percent to 30% of its investments were in private equity, real estate, and infrastructure. Less than 20% was in U.S. stocks.

Abu Dhabi’s $2.5 trillion sovereign-wealth fund is one of the largest globally and consistently holds 40% to 60% of its assets in alternative investments. Singapore’s are even more aggressively tilted toward private markets.

Now, if you feel like these investments are restricted to a club you can’t join, don’t. In my High-Yield Advisor service, for example, I strategically recommend publicly traded business development companies (“BDCs”) that are among the best in the world at direct lending.

These BDCs are currently trading at the best valuations in years, and many yield over 10%. They exist specifically to provide credit to the thousands of private U.S. companies that are the real fuel behind the U.S. economy and job growth.

I also recommended under-the-radar bonds backed by some of the highest-quality infrastructure assets in the world. We invested in those with incredible 30% to 35% discounts to par value with yields well above 7%.

The point is, you don’t need to be ultra-wealthy to take advantage of these opportunities. But you do need to understand parts of the market that most others don’t.

If you want our help and are interested in using these strategies to generate current income 50% greater than U.S. high-yield bonds with historically less risk, the easiest way to learn more would be to reach out to our customer support team. Just tell them you’re interested in learning more about High-Yield Advisor, and they’d be happy to help. You can contact them here.

Regards,

Stephen Hester

Chief analyst, Wide Moat Research

|