Politics isn’t my usual beat here at The Wide Moat Daily. It’s markets… with special attention given to commercial real estate.

But, sometimes, those two things overlap…

With that in mind, I wanted to discuss New York City real estate under incoming Mayor Zohran Mamdani. As I wrote on Thursday, “Being a commercial real estate guy, I can tell you right now: This will not end well.”

This is based on Mamdani’s promises to:

-

“… immediately freeze the rent for all stabilized tenants…”

-

“… triple the City’s production of permanently affordable, union-built, rent-stabilized homes…”

-

“… overhaul the Mayor’s Office to Protect Tenants and coordinate code enforcement under one roof, making sure agencies work together to hold owners responsible for the conditions of their buildings…”

These plans might sound right and even righteous on paper. But they don’t work in real life.

It’s All About Incentive

Are New York City housing prices astronomical? The easy answer is “yes.”

A studio apartment – which has no actual bedrooms, just a bathroom and an all-use area – costs an average $3,000 per month. And that’s just an average. Many are much higher.

But none of that is necessarily the fault of landlords. New York is a high-demand market. And as a densely populated city, real estate is at a premium. Throw in the rising costs from inflation and the labyrinth that is New York bureaucracy… and it all trickles down to the rent tenants pay.

Putting all the responsibility on landlords is not the solution. It will only make things worse.

Business podcaster Xavier Miller laid this out on Thursday, writing how:

Every time politicians try to control rent or force affordability by decree, developers stop building and landlords stop maintaining. Supply dries up, the quality collapses, and the few properties that remain skyrocket in price.

There’s plenty of research to back him up. In 2019, the American Economic Review published a study that looked at the effects of an expanded rent control law in San Francisco in the early ’90s.

The study found that:

[W]hile rent control prevents displacement of incumbent renters in the short run, the lost rental housing supply likely drove up market rents in the long run, ultimately undermining the goals of the law.

There’s almost no chance this time around will be different. After all, many New York City landlords are already struggling under the burdens of increased property taxes, maintenance, insurance, legal fees, and mortgages.

As a former real estate developer and landlord, I’ve put up with all those headaches before. It can be a nightmare. And the only reason that developers continue to build and maintain properties is because of the incentive that is rental income.

Freeze that rent – or limit the landlord’s ability to raise it in the face of rising costs – and you take away the incentive. Then, all you’re left with are the headaches. It’s a recipe for diminishing supply.

Worst-case scenario – the policies could leave America’s largest city in a 1970s-style lurch it hoped to never see again.

Drop Dead City

New York City’s crisis of the 1970s was caused by a variety of factors. But unchecked government spending definitely played an enormous part.

To quote The New Yorker 100‘s review of Peter Yost and Michael Rohatyn’s historical documentary on the subject:

The story set out in Drop Dead City remains startling even half a century later. In 1974, New York’s new mayor, Abraham Beame, took office believing that the city was two billion dollars in debt. For the previous four years, he’d been the city’s comptroller, so he oughta know.

However, his young successor in that office, Harrison Goldin, conducted an audit and discovered that the debt was actually about six billion dollars. The finances were in total disarray… the city was meeting payroll by issuing round after round of short-term bonds, underwritten (i.e., purchased for resale) by banks.

In order to deal with the resulting financial reality, the city’s budget was slashed. Police officers were laid off, as were firefighters, teachers, and sanitation workers – with predictable results.

Trash piled up. Property valuations fell, and wealthy residents left. In the process, many residential buildings fell into disrepair and were abandoned altogether, adding to already elevated levels of vagrancy and crime.

It wasn’t pretty, to say the least. And it could be even worse this time around, considering how the city is already in a state of crisis.

It has been ever since COVID-19 hit, the shutdowns commenced, and regulations skyrocketed.

I already mentioned on Thursday how many people have left New York City in the past five years. That’s part of the reason why:

State Comptroller Thomas P. DiNapoli recently forecast that New York City’s budget shortfall will be a whopping $13 billion within the next three years… And we’ve known for months that, since its 2023 fiscal year, NYC has spent more money than it’s received.

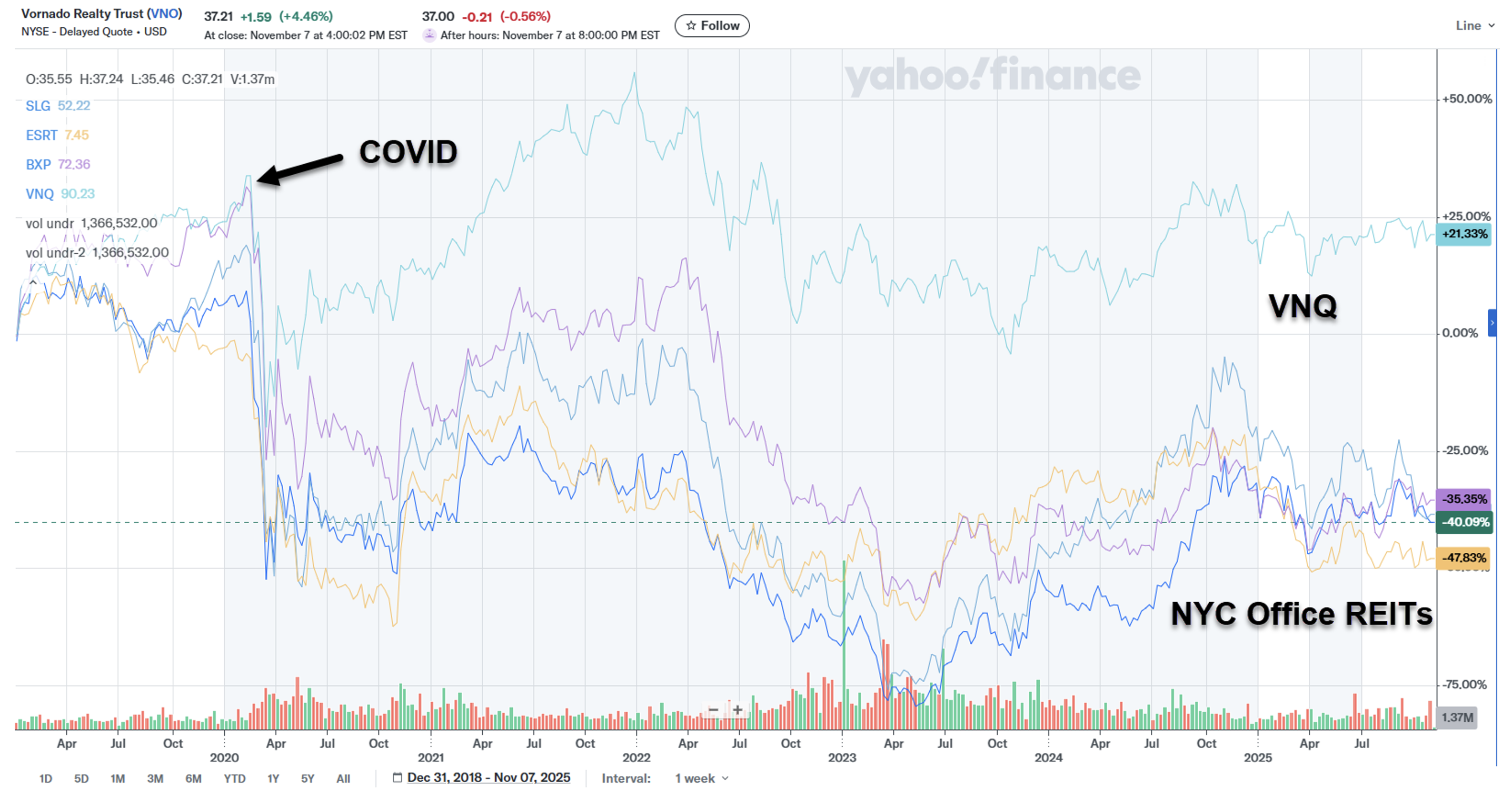

New York City’s properties haven’t recovered yet either, as evidenced by its real estate investment trusts (“REITs”). Those once-mighty corporate landlords still aren’t trading at their pre-COVID levels.

For proof, just look at the Vanguard Real Estate Index Fund (VNQ) compared with just the New York City office REIT space:

Source: Yahoo Finance

It’s not even close.

The NYC Versus Florida Disparity

It should come as no surprise, then, that New York County has lost quite a few residents as well.

Its population plunged by 110,958 (or 6.9%) between July 2020 and July 2021 alone. And people have continued to relocate since. Not at the same intense rate, but it’s still happening.

Florida has been one of the biggest beneficiaries of this migration, to be sure. In fact, between July 2020 and July 2024, over 24.7% of the entire United States’ total net relocators moved there.

To illustrate the effect of all this on real estate, just consider President Trump’s properties in the two states. I covered all his holdings almost a decade ago in my book, The Trump Factor: Unlocking the Secrets Behind the Trump Empire, including:

-

Trump Tower, which was one of the first mixed-use buildings along Fifth Avenue, with retailers occupying levels 0 to 4, offices on levels 4 to 26, and residential space from 27 to 68. I valued it at $803 million in my book, which was published in 2016. But my back-of-the-napkin estimate puts it down about 25% since then to around $640 million.

-

The 72-story 40 Wall Street, which I initially valued at $565 million, is likely just $450 million today.

-

1290 6th Avenue – of which Trump owns 30% and NYC REIT Vornado Realty (VNO) owns 70% – used to be worth $1.6 billion. But I would now put this 2.1 million square foot office building at $1.3 billion.

The story is very much different down in Florida, however.

In 2016, I valued Mar-a-Lago at $300 million, for instance, including accessories and art. Judging by the Sunshine State’s ongoing economic boom, it’s worth an easy $600 million today by my estimation.

That’s just what happens when people are running to your state, not away from it.

The Flight to Florida – and Elsewhere – Continues

As I explained in my article last week, “ABC7 News reported poll findings that close to 9% of people will flee the city if Mamdani becomes mayor.” That’s another 765,000 residents on top of the hordes that have already left.

Florida real estate brokers have already reported an uptick in calls from New York investors and ultra-wealthy buyers. And I’m hearing the same thing here from my contacts in South Carolina.

The numbers into New York, meanwhile, are not reciprocal.

That’s why I’m going to reiterate what I said on Thursday: There are greener pastures to invest in.

Take my home state of South Carolina. It recorded the highest GDP growth in the entire country in the first quarter. And it’s still growing at an impressive clip as the year winds down.

New York is a large and wealthy city, but it can be easy to forget what made it that way… and how quickly things can go wrong. Mr. Mamdani cannot solve the New York affordability crisis with his desired policies. In all likelihood, it’ll just get worse.

Regards,

Brad Thomas

Editor, Wide Moat Daily

|