As my loyal readers know, I’m a big college basketball fan. I played it back in my own school days, and I enjoyed pickup for over 30 years altogether.

I officially gave up the sport around a decade ago after suffering too many injuries. (Those are the literal breaks sometimes.) But my love for the game remains very much alive and well.

That’s why I was so excited to meet my oldest daughter and her husband in Chapel Hill on Saturday to watch the University of North Carolina (“UNC”) play Virginia Tech. It has been over a decade since I attended a game at UNC, so I was thrilled to get a ticket – especially in the front row.

Source: X (@bradthomas)

Spoiler alert: North Carolina won 89 to 82. So the Tar Heels now have a set-in-stone, top-tier spot for the upcoming March Madness competition…

Which kicks off on Tuesday, March 17, with the "First Four" games.

That’s still two weeks out, though. So, in the meantime, I thought I’d get started on a small tradition.

This is the time of year I like to put together my own competition, though not of college teams… of real estate investment trusts (“REIT”).

Over the next few weeks, I’ll be compiling a matchup analysis of my top REITs. We’ll work through various sectors to find those that belong in the:

-

Sweet 16

-

Elite 8

-

Final Four

And we’ll start with…

Nothing but Net

I usually like to start out these “games” by looking at the tried-and-true net-lease REIT space.

Since 1994, this sector has returned an average of 14.2% per year compared with 11.6% for REITs in general. And so far this year, they’ve advanced 17.9%, making them the third-best performer.

Farmland takes first place at 35.1%, data centers are second with 22%, and self-storage and shopping centers tie for fourth at 17.1%.

Those are all attractive returns, but there really is just something special about net-lease REITs. Good times or bad, there’s very little drama here thanks to their long-term leases that require tenants to pay most or all of the properties’ operating and management expenses.

This includes taxes, insurance, and maintenance, including utilities.

As such, exceptionally stable companies – often national chains like McDonald’s or 7-Eleven – tend to sign with net-lease REITs. And they then pass their consistent income generation, appreciation, and inflationary hedge qualities on to their landlords… even when the economy is down or inflation is elevated.

There are 21 publicly traded REITs within the U.S. net-lease sector that we cover here at Wide Moat Research. They add up to a market capitalization of over $154 billion.

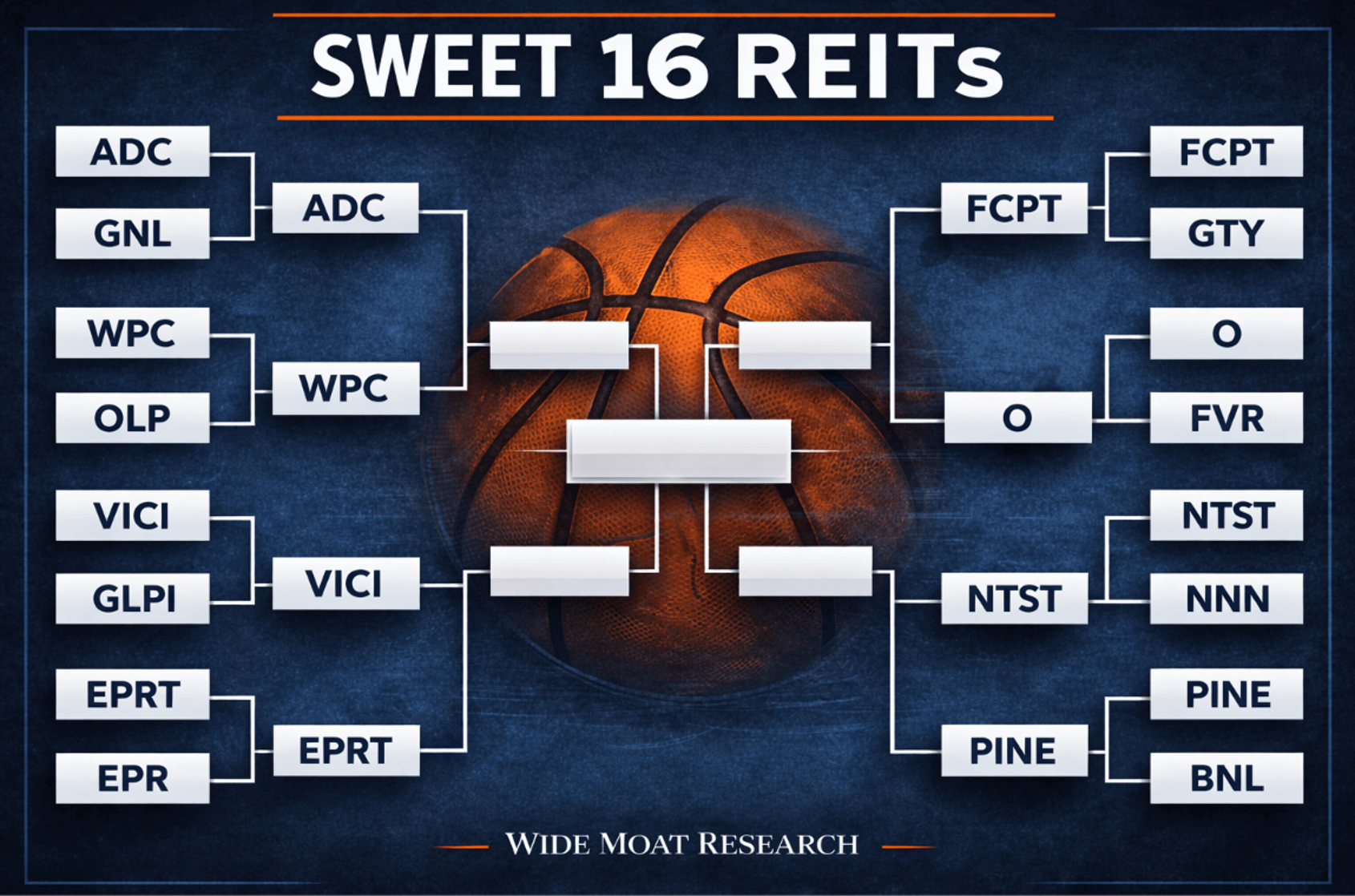

But today, we’re going to narrow that field down to 16: eight matches we’ll evaluate to see who advances to the next round of the REIT March Madness competition.

Agree Realty (ADC) versus Global Net Lease (GNL)

GNL has a higher yield compared with Agree Realty. But it’s also a chronically weaker REIT with a history of dividend cuts.

Agree, on the other hand, has:

-

A strong balance sheet (A-rated)

-

Best-in-class cost of capital (5.4% equity yield)

-

High-quality retail tenants (majority investment-grade)

-

Conservative underwriting (steady dividend increases)

So the winner here is clear: Agree takes the game.

W.P. Carey (WPC) versus One Liberty Properties (OLP)

One Liberty Property is smaller in size and therefore can’t rely on the same level of scale as its competitor here does. Plus, it’s consistently underperformed, whereas W.P. Carey boasts:

-

A diversified net-lease platform (1,682 properties and 371 tenants)

-

A long track record (since 1973)

-

Institutional scale (with offices in New York and Amsterdam)

As such, we have another clear and easy winner in WPC.

VICI Properties (VICI) versus Gaming and Leisure Properties (GLPI)

This matchup is more evenly split, with Gaming and Leisure a strong contender. However, many of you know my thoughts about VICI and its:

-

Strong balance sheet (BBB- rated)

-

Long-duration triple-net leases (of about 40 years)

-

CPI-linked escalators (1.7% same-store rent growth)

-

Active expansion beyond casinos (wellness, theme parks, golf, etc.)

I wrote a recent article detailing my support of VICI, and that analysis holds up here as well.

Essential Properties Realty Trust (EPRT) versus EPR Properties (EPR)

EPR used to be known for its heavy concentration of movie theaters. So, when the pandemic hit and social distancing stretched on (and on and on), it got hit pretty hard.

It has done a commendable job of cleaning up its portfolio since then. There’s no doubt about that.

All the same, it still comes short compared to Essential Properties’:

-

Disciplined management team (about 30 basis points, or bps, of annualized credit loss)

-

No theater exposure whatsoever

-

Stronger growth profile (sector-leading annual adjusted funds from operations, or AFFO, growth of around 9%)

So, while I’m more than happy to acknowledge EPR’s resiliency, EPRT still wins today with its best-in-class growth.

Four Corners Property Trust (FCPT) versus Getty Realty (GTY)

Getty Realty is a consistent dividend payer that reported strong fourth-quarter results. However, it’s less clear how much growth it can muster over the next few quarters.

In contrast, Four Corners:

-

Continues to diversify away from Darden Restaurants (DRI) – owner of Olive Garden – into tenants with healthier prospects

-

Has solid financials and undervaluation

-

Boasts a stronger growth profile

Its balance sheet is stronger too, which is why Four Corners comes out ahead.

Realty Income (O) versus FrontView (FVR)

This one isn’t even close. Honestly, it’s an unfair matchup from start to finish, but that’s how March Madness goes sometimes. Not everyone can be a winner.

FrontView has 307 properties in 37 U.S. states, and its shares have risen about 26% over the past six months. So good for shareholders who got to ride that wave.

However, it might be in for a pullback now, whereas Realty Income is a best-in-class net-lease REIT with:

-

Over 15,000 properties throughout the entire U.S., as well as Europe

-

An A-rated balance sheet that gives it excellent cost of capital

-

New capital channels through ventures such as the private fund it just launched, raising $1.5 billion from over 40 institutional investors

You can read my latest article on Realty Income right here.

National Retail Properties (NNN) vs NetStreit (NTST)

National Retail Properties is a dependable choice in its own right. However, if you’re looking for a little pep in your net-REIT step, NetStreit is a winner.

A newcomer to REIT-dom, it listed shares in 2020 with solid fundamentals. And since then, it has claimed:

-

A proven track record of 99.9% occupancy with strong unit-level coverage (3.8 times)

-

Low leverage with no intermediate-term debt maturities (24% pro forma adjusted net debt/undepreciated gross assets)

-

High-quality tenants with strong credit profiles (58% investment-grade)

In short, NTST is smaller but faster growing with a better external growth runway. I also like its solid fourth-quarter earnings and recent reaffirmation of its 2026 guidance.

So it’ll be interesting to see how it fares in the next round of the competition…

Broadstone Net Lease (BNL) versus Alpine Income Property Trust (PINE)

Broadstone has a stable BBB credit rating and a higher dividend that could be tempting in a different matchup. But Alpine features a:

-

Stronger growth profile (in the double digits)

-

Well-laddered debt maturities

-

Solid dividend payout ratio

So PINE comes out ahead for now, and we wish Broadstone better luck next time!

In a few weeks, I’ll put together an “Elite Eight” article highlighting the winners of this round and my Final Four picks as we narrow the field down to find the ultimate net-lease champion.

Even though net-lease REITs have returned almost 18% year to date, I believe the sector will continue to deliver solid returns.

I hope you enjoyed this March Madness-themed article enough to stay tuned for the others I’ll be writing over the next few weeks. And tune in to The Wide Moat Show this week, where we’ll be discussing our all-encompassing stock market bracket.

Happy SWAN (sleep well at night) investing!

Regards,

Brad Thomas

Editor, Wide Moat Daily

|