McKinsey Research recently indicated that a highly selective real estate rebound is underway where “special sectors are surging.”

While there are still opportunities to be had in traditional real estate fields such as apartments, office buildings, and retail, they’re hardly the most interesting properties out there anymore.

The real estate investment trust (“REIT”) space has changed a lot in the past 15 years. Up until the Global Financial Crisis hit in 2008, the most “unique” REIT category was probably for-profit prisons – a sector that disappeared during the Obama years.

But numerous niche REIT categories emerged post-2010. These companies sought to capitalize on specific economic brackets, unique tenant relationships, and high barriers to entry.

Naturally, not every single new venture is a good one. And even the better ones can have significant ebbs and flows in favor.

Today, we’ll explore the lengthening list of niche REITs, assessing each one as individual businesses for what they’re worth.

Not All Specialties Can Shine

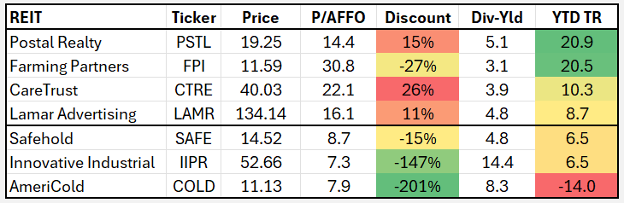

Americold Realty Trust (COLD) traces its origins back over a century. But it officially changed its legal structure in 2018 when it listed as the world’s first publicly traded cold‑storage REIT.

These facilities tend to be large, climate-controlled warehouses that store food before those items end up on grocery-store shelves.

Unfortunately, its business sits at a tricky intersection of real estate, logistics, and food supply – all of which are capital-intensive and cyclical in nature. So, Americold has struggled at various times as a result.

In addition, cold‑storage facilities require energy‑hungry climate-control systems, which result in higher maintenance and utility costs than standard warehouses. And those in turn are more exposed to spikes in electricity or fuel prices.

Don’t get me wrong: Americold still benefits from secular tailwinds such as growth in fresh and frozen food logistics and the rise of online grocery delivery. However, those positive points have been slower to translate into consistent profits.

Shares have actually returned negative 14% year to date, with no signs of when they’ll rebound.

Safehold (SAFE), meanwhile, was founded in 2017 by iStar and specializes in modern ground leases. This means it rents out land for decades at a time, allowing tenants to build on it – only for those buildings to revert to Safehold once the long-term contract is up.

The REIT owns land beneath 164 assets with a total book value of around $7.1 billion. Yet the stock has underperformed over the past several years despite its steady income.

This is mainly because the market has grown cautious about its execution risks and complex financial structure, concerns that have left it gaining just 6.5% so far in 2026.

Moving on to the cannabis sector, Innovative Industrial Properties (IIPR) was the groundbreaker here. Founded in December 2016 to lease land to marijuana farmers and producers, it became a REIT in 2017.

Innovative Industrial owns 111 properties across 19 states with over 35 tenants. But its business model involves long-term, triple-net leases… in an unregulated industry that’s overgrown to the point of becoming unprofitable.

In late 2024, PharmaCann – IIPR’s largest tenant, which represents about 17% of its revenue – defaulted on rent for six of its properties… which then triggered cross-defaults across all 11.

Since similar troubles have occurred with other tenants, it’s no surprise that IIPR remains a riskier play.

Source: Wide Moat Research

But the Profit Story Changes for These Niche REITs

One relatively new specialty REIT worth mentioning is Postal Realty Trust (PSTL). Having listed shares in 2019, it currently owns over 1,900 free-standing properties leased to the U.S. Postal Service (“USPS”). Hence its name.

Postal is the largest owner of USPS facilities in the country. It boasts a practically perfect retention rate of 99.5% alongside 5.5% same-store net operating income (“NOI”) growth.

Year to date, shares have surged, returning 20.9% as this mission-critical landlord continues to deliver steady and growing dividends. Shares are a tad rich right now, however, so I recommend waiting on a pullback.

Billboards are another niche REIT sector worth examining, with old-timer Lamar Advertising (LAMR) easily standing out. Founded in 1902, it converted to a REIT in 2014 and owns over 361,000 advertising displays in 45 states and Canada.

Back in August, I wrote about Berkshire Hathaway’s (BRK-A)(BRK-B) $142 million investment into Lamar. And it shouldn’t be surprising that shares have returned around 19% since that disclosure.

Just like Postal Realty, Lamar enjoys an enviable scale advantage, where it can continue consolidating within a highly fragmented industry. I suspect Lamar will also continue to execute merger and acquisition (M&A) deals going forward to further expand its market share.

CareTrust REIT (CTRE) is also worth mentioning. This health care REIT owns 297 properties consisting of:

-

Senior housing (41.7%)

-

Skilled nursing (57.6%)

-

Small business health options program, or SHOP, offices (0.7%)

Skilled nursing and senior housing are critical components of health care infrastructure driven by the growing senior population. And CareTrust’s well-constructed portfolio of quality assets and talented operators drive top- and bottom-line financial results.

That, in turn, led to superior earnings growth of 17% in funds from operations (“FFO”) per share last year and 14% in per-share funds available for distribution (“FAD”).

The REIT recently announced a 16.4% dividend increase payable on April 15 – and remember that the safest dividend is the one that has just been raised.

I also want to mention Farmland Partners (FPI), which owns around 71,600 acres across 11 states, plus land and buildings leased to agriculture equipment dealerships in Ohio.

The farmland space it operates in is one of the largest commercial real estate sectors, valued at around $3.8 trillion. Yet it also features the lowest institutional ownership. So, Farmland Partners can continue to capitalize on growth by consolidating within this emerging REIT sector that boasts a near-zero vacancy business model.

Get Rich With This Niche

Let’s face it, though… Data-center REITs still steal the scene these days.

Deal volume has surged 37% year to date, making the sector a global dynamo that’s lighting up many next-tier markets. And as shown below, data centers have been the top-performing property sector over the past decade.

Source: Wide Moat Research

I’ve been covering the sector for over a decade. So, I’ve closely watched the industry’s dramatic evolution through two powerful trends: the demand for cloud computing and the growth of AI.

AI training and inference require massive computational power, which in turn needs enormous, specialized data centers. Companies like Microsoft (MSFT), Amazon (AMZN), and Alphabet (GOOG) are expanding their capacity rapidly, driving rents and utilization higher for companies that own or operate these facilities.

Year to date, data-center REITs have returned 23.8%, led by:

-

Iron Mountain (IRM), up 28.2%

-

Equinix (EQIX), up 26.6%

-

Digital Realty (DLR), up 16.1%

Markets now see data-center REITs more as infrastructure or tech‑adjacent assets – something closer to utilities with greater growth upside. But the fact is that they remain real estate plays, nonetheless.

Regards,

Brad Thomas

Editor, Wide Moat Daily

|