There’s a lot going on in the world.

But, just for today, let’s go back to the very beginning. Today, I’ll tell you what I know to be true about investing. And I’ll share one reliable dividend payer I’ve had my eye on.

If you’ve been reading my Wide Moat Daily columns for long, you know how much I love dividend stocks. The reason is simple.

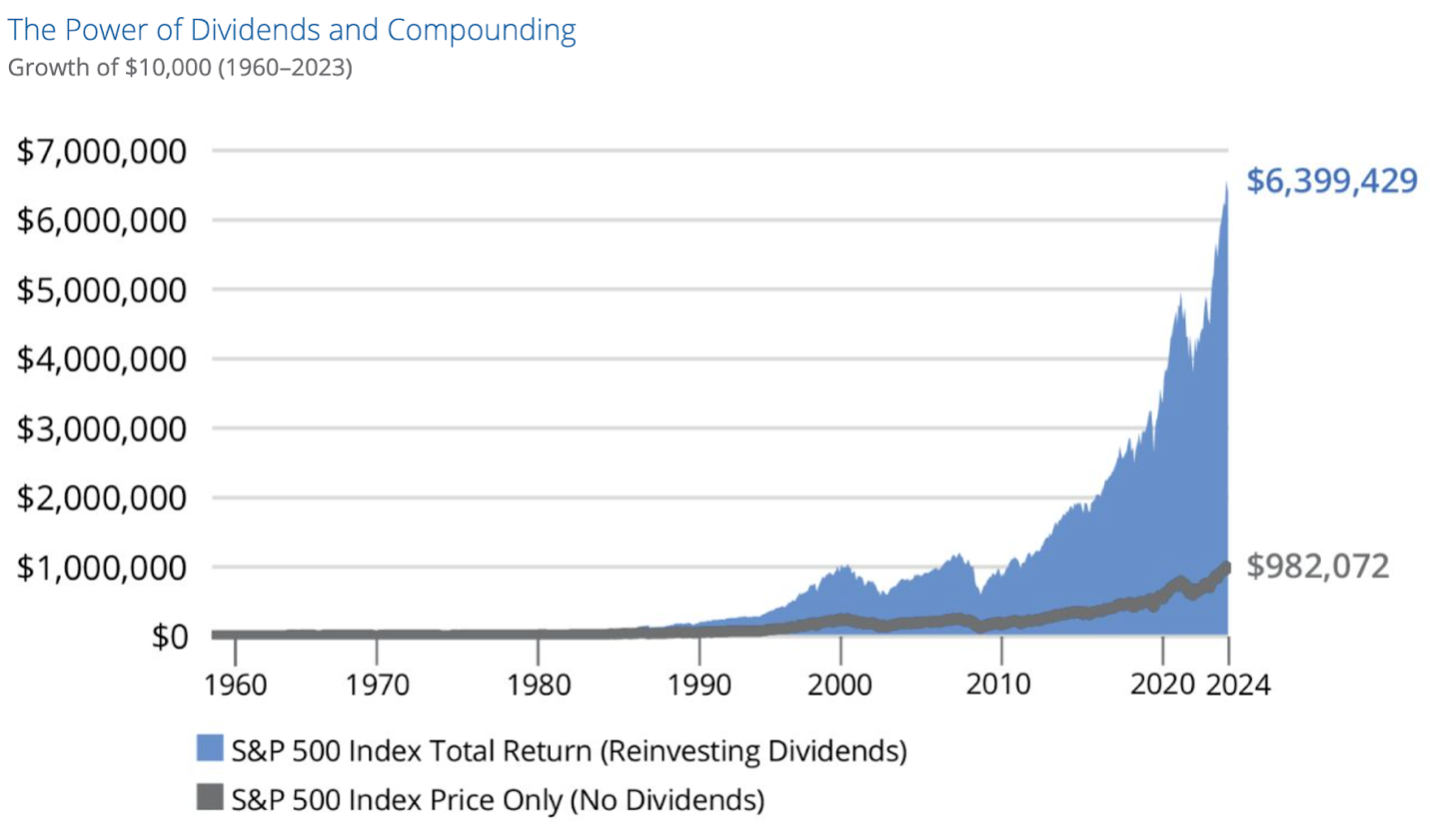

For the long-term investor, reliable, rising dividends is a recipe for outperformance. We’ve shared this chart before, but it never gets old.

Source: The Hartford Fund

That chart is a great illustration of what patience, consistency, and the process of compounding can deliver.

Dividends are also appealing for another reason.

When dividends are paid, it’s a tangible return on investment. Capital gains are wonderful, of course. But the truth is, you have to sell a stock before you realize that return.

Until you do, it’s a paper gain only… which always runs the risk of turning into a loss.

That’s not the case with dividends. Once a company declares a dividend, it’s yours. There’s no waiting months, years, or more to cash out.

And while we’re generally proponents of dividend reinvesting for those building their wealth, the dream of many retirees is to simply live off their dividend income in their golden years.

Dividends are also a key indicator of the overall health of a company. When a business makes one of these payments, that almost automatically means it’s making a profit.

It can’t just pay out money it doesn’t have, after all. Not unless it’s financially engineering the dividend (i.e., robbing Peter to pay Paul).

And in those cases, the payout ratio – the percentage of earnings going toward dividend payments – offers a clue.

When that figure is elevated, it’s time to investigate further. It could just be that the company is temporarily going through a rough patch… or that it’s straining its finances in order to pay its shareholders.

This brings me to a third reason I like dividend-paying companies so much: Their dividend history can provide so many valuable clues about their overall health.

If the company has a chronic record of dividend cuts, for instance, it might be operating with a flawed business model or a poor management team, and the stock should be avoided.

But if they perpetually offer higher dividends year after year, while maintaining a reasonable payout ratio, it’s a sign of strength.

My Favorite Kind of Dividend Companies

I like owning stocks with steady and predictable dividends. That’s one of the reasons why I like real estate investment trusts (“REITs”) so much – my topic from yesterday.

These corporate landlords are my specialty and an asset class I’m proud to cover.

I’ve personally seen how the right REITs can transform a portfolio over time. These mandatory dividend payers are governed by strict rules that tend to keep them more conservatively managed.

In exchange for an income tax exemption, REITs pay out at least 90% of their otherwise taxable income annually to shareholders. This setup tends to mean that they pay higher dividends than other companies, not to mention more stable ones, too.

However, as I also added:

Dividends are well and good. But when it comes to share price appreciation, REITs haven’t done much lately. In fact, they haven’t done that well since the Fed began raising interest rates in early 2022. And while REIT enthusiasts like me certainly hoped this year would mark their big share price return…

That just hasn’t happened yet.

Not that this has stopped Simon Property Group (SPG) from thriving. The mall REIT just announced a $0.05 per share dividend increase this week, representing a 4.9% year-over-year increase.

That’s something beautiful to behold.

When I saw the news, I knew that Simon’s business model was performing well – very well, in fact. Otherwise, the management team would have maintained its current distribution.

And this is despite the continuing power of e-commerce and struggling consumers.

Simon Says the Time Is Right

Simon Property Group also reported second-quarter results on Monday, and they were solid:

-

Funds from operations (“FFO”) per share of $3.05, up 4.1% year over year

-

A 4.2% spike in net operating income

-

A 96% lease rate, up 40 basis points year over year

-

And it raised full-year FFO guidance 9% to a midpoint of $12.36.

Meanwhile, its fortress balance sheet includes $9.2 billion of liquidity with 5.5 times leverage. That remains a key competitive advantage as the company is more bullish on external growth and redevelopment.

As of the second quarter of 2024, Simon’s redevelopment pipeline stood at about $1 billion (with roughly 9% yields). And it expects to deploy approximately $260 million in second half of 2025, funded through its annual $1.5 billion in free cash flow.

Simon already acquired its joint-venture partner’s interest in the retail and parking facilities at Brickell City Centre in Miami for $512 million last quarter. I’ve visited this property on many occasions, and I can attest that it’s a real gem.

I’m certain the return on investment will be above average.

As for the rest of its external expansion plans, CEO David Simon explained on Monday’s earnings call:

… we’re going to be picky on what we buy and what we want to do. But we’re able to do it because this company doesn’t need to sell a bunch of assets [and] doesn’t need to bring in a new management team. It doesn’t need to downsize its platform. It doesn’t need to do it because it’s outperformed over a 30-plus year period that no one else has done.”

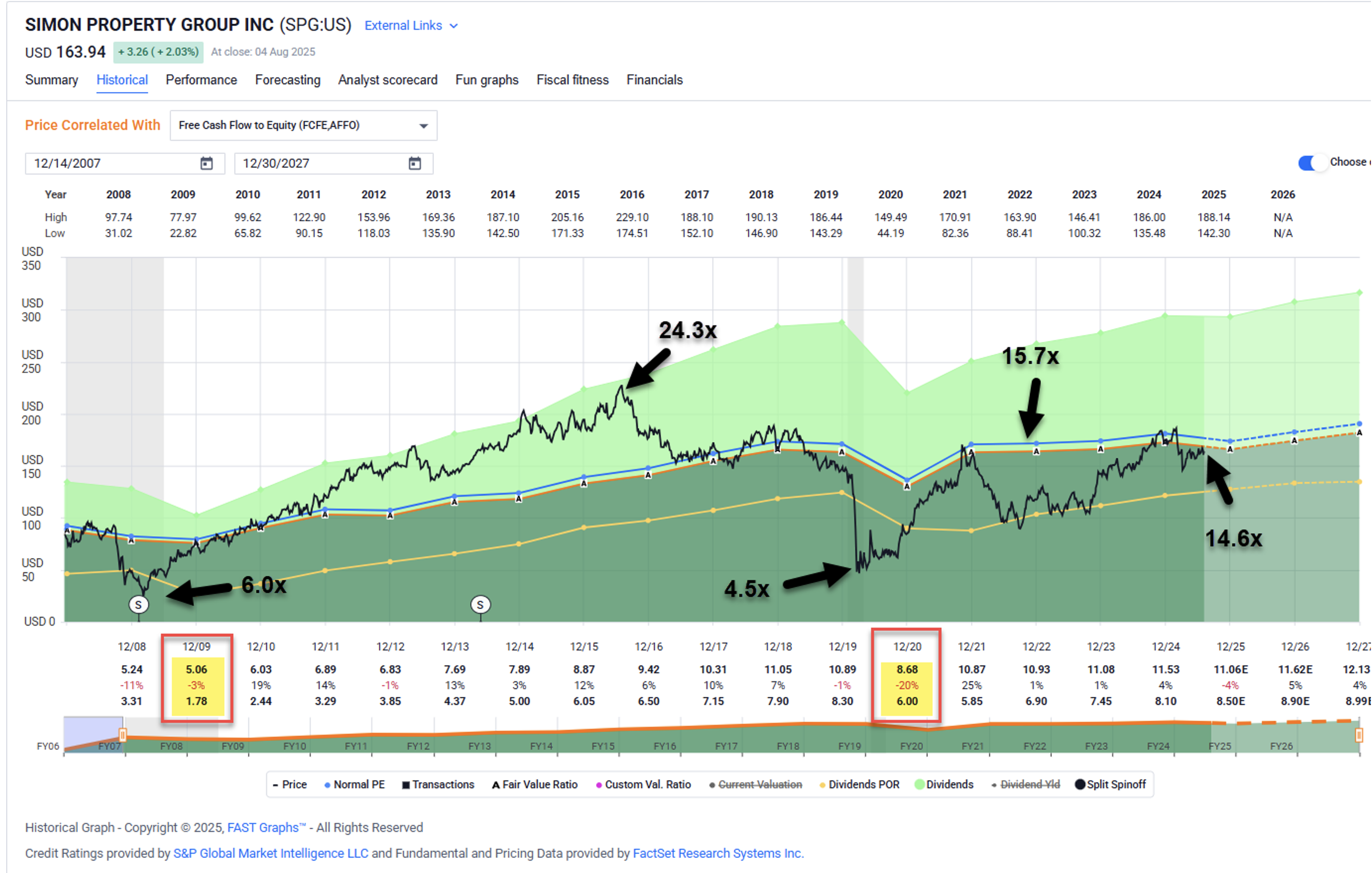

As you can see below, Simon was forced to cut its dividend during the Global Financial Crisis (2008-2009) as well as the COVID pandemic. At first glance, that might make an investor nervous.

However, both enormous, unpredictable, and unprecedented black swan events – ones that I don’t see happening again. And the company has always maintained a healthy balance sheet regardless, even in the midst of that mess.

Since COVID, Simon’s earnings stream (via adjusted FFO, or AFFO, per share) has continued to increase in line with its dividend. And based on analyst consensus numbers, Simon is expected to grow by 5% in both 2026 and 2027.

Source: FAST Graphs

In addition, as per the chart above, shares are now trading at 14.8 times price to AFFO. That’s below their normal valuation of 15.7 times. In 2016, shares traded as high as 24.3 times.

Simon’s dividend yield is currently 5.1% and well-covered based on a payout ratio of 76%. I can’t quite call this stock a bargain, but I do think it’s a worthwhile buying opportunity to consider nonetheless.

Regards,

Brad Thomas

Editor, Wide Moat Daily

P.S. How do you know what to buy and what to avoid? That’s what I’ll be discussing on my YouTube show this week. Be sure to tune in this Thursday!

|