I’ve already written about real estate investment trusts (“REITs”) twice this week.

I’m covering them again tomorrow, both right here at Wide Moat Daily and on my YouTube show.

And, yes, I’m writing about them today, too.

As I explained on Monday and Tuesday, the Federal Reserve is almost certain to cut rates this month. The last three months’ jobs data, including intensely negative revisions to previous calculations, were damning enough.

But then yesterday, we learned that the U.S. economy has been in trouble for much longer than that. All those amazing jobs reports we kept seeing in 2024 were incorrect, it turns out.

Astoundingly so.

According to preliminary evaluations, the U.S. probably added 911,000 fewer jobs than previously reported between April 2024 and March 2025. That would mean slightly more than half of the supposed job gains were a mirage. If true, that would be the largest revision ever in the Bureau of Labor Statistics’ history.

I’m unimpressed with the collection and analysis skills (or lack thereof) being highlighted here. It means the preliminary results were off by so much as to basically be worthless.

But for those of us in the REIT-watching world, there is a silver lining.

Not only will we now see a rate cut next week… the chances of seeing another one in October and another one in December just went up. The market agrees. The prevailing opinion is that the Fed Funds rate will be 350 to 375 basis points by year-end. That would be a 75-basis-point cut from current levels.

That should be good for U.S. businesses in general and REITs in particular, including in the health care sector.

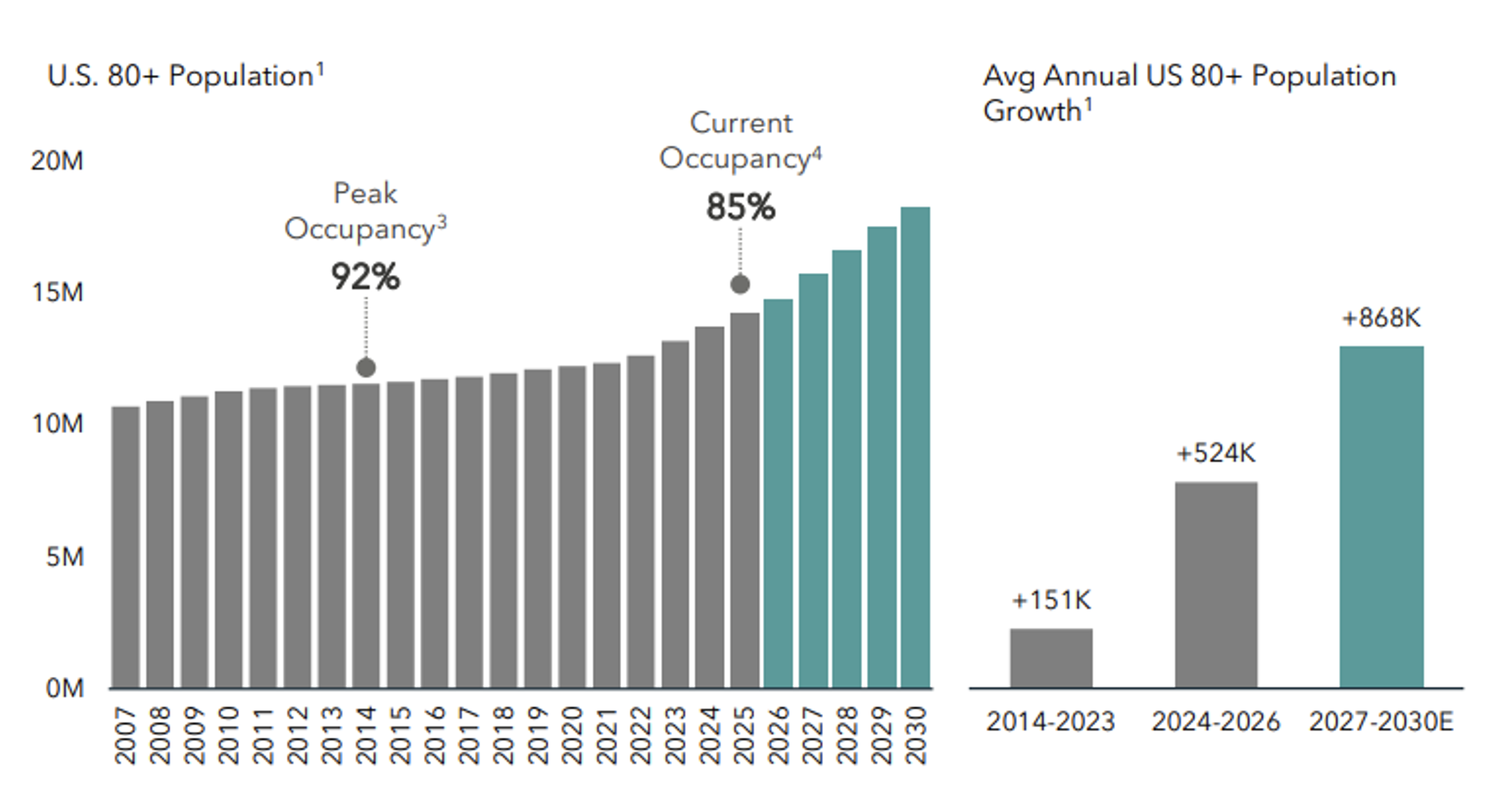

More Evidence of the Silver Tsunami

Longtime readers will know I’ve been following the “silver tsunami” trend for some time. In short – the country’s population of Baby Boomers are getting older (all 73 million to 76 million of them). And as they age into their golden years, they’ll make use of more health care and long-term-care facilities. The jobs report from Friday seemed to confirm that.

The report showed that of the 38,000 jobs added in the private sector, 46,800 came from health care and social assistance. That’s right. Were it not for jobs growth in health care and related industries, the already poor job growth from August would have been negative.

We’ll see if these figures are eventually revised away. But for now, it suggests that the only meaningful employment growth is happening in health care. That may not be ideal for the labor market in general. But it’s one heck of a macro tailwind for health care REITs.

Mission Critical

As I explained in REITs for Dummies, health care REITs account for 9% of the U.S. equity REITs, consisting of these categories:

-

Senior housing properties (i.e., assisted or independent living)

-

Skilled nursing (i.e., nursing homes)

-

Medical office buildings (aka MOBs)

-

Hospitals (including outpatient facilities)

-

Life-science labs

These properties all offer important and even necessary services, making them fairly predictable income producers. Plus, their demand should only escalate from here considering the so-called silver tsunami.

As such, the next five years are going to see a lot of growth opportunities for health care facilities. Their landlords, too.

Source: Ventas Investor Presentation

Now, a rising tide (or falling interest rates) lifts all ships, but that doesn’t mean you should buy just anything on the market. We still want to identify quality companies at bargain prices.

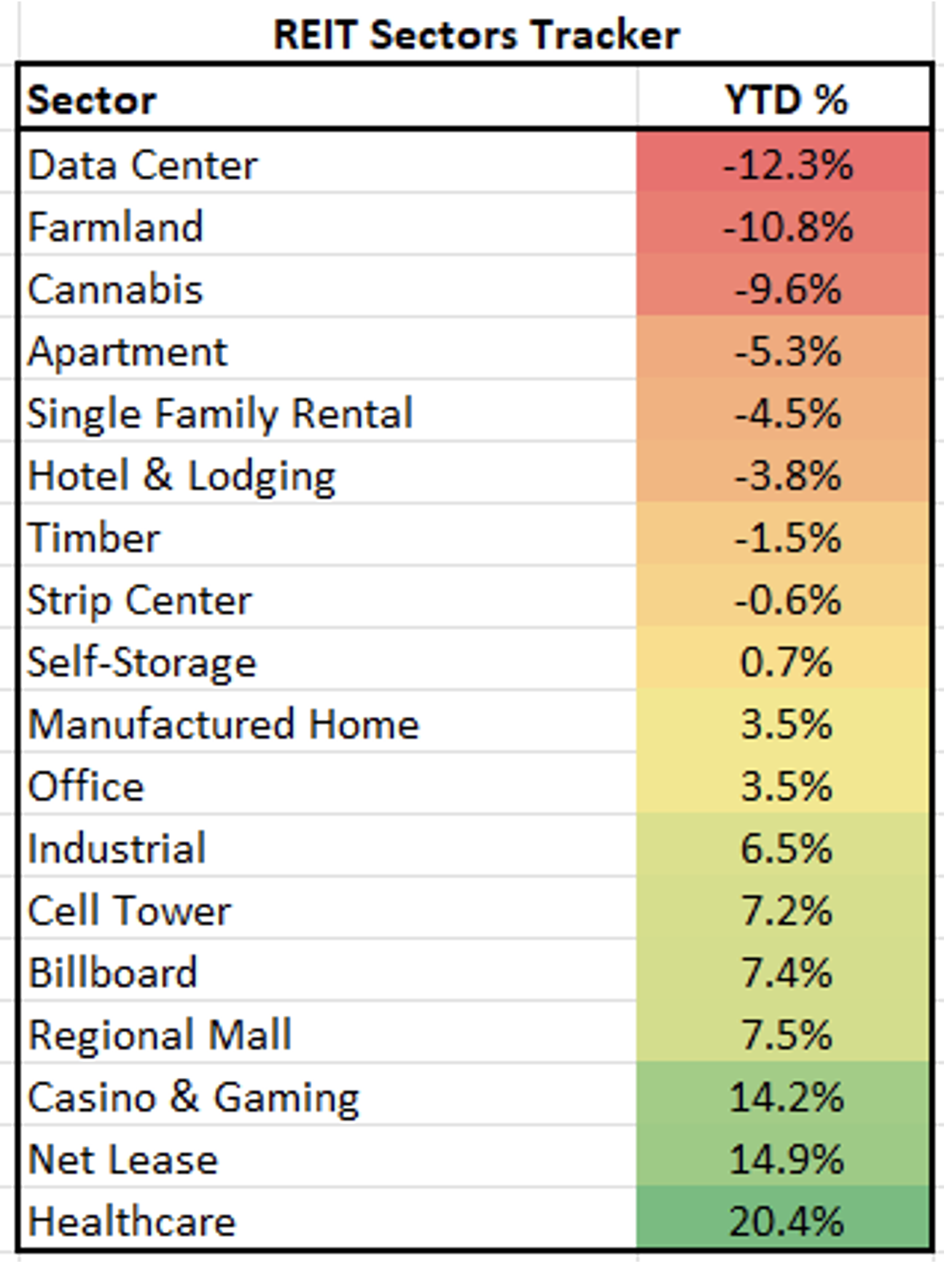

And health care REITs as a sector are up 20.4% so far this year – the most out of any other REIT category.

Source: Wide Moat Research

But with all the negative news pointing to multiple rate cuts from here, health care REITs have a very good chance of shining further this year and into 2026.

That’s why I want to review my top picks in this space today.

Health Care REIT 1: Alexandria Real Estate

Alexandria Real Estate (ARE) is a “garage startup” life science landlord founded in 1993 that went public in 1997. Today, it’s a $32 billion S&P 500 constituent with a 39.8 million square foot portfolio across:

-

Greater Boston

-

The San Francisco Bay Area

-

San Diego

-

Seattle

-

Maryland

-

North Carolina’s Research Triangle

-

New York City

Alexandria has a sector-leading client base of around 750 tenants. And 53% of its rental revenue comes from investment-grade or publicly traded large-cap tenants.

Plus, it boasts long-duration lease agreements with a weighted remaining lease term of 9.4 years for its top 20 tenants.

Alexandria also has a strong balance sheet rated BBB+, which puts it in the top 10 for all publicly traded REITs. The company has just 9% of debt maturing in 2027, with a weighted average debt term of 12 years.

For the record, that’s the longest among S&P 500 REITs.

On Alexandria’s second-quarter earnings call, management reiterated guidance for year-end 2025, with occupancy targeted at 90.9% to 92.5%. Funds from operations (“FFO”) per share, meanwhile – the real estate version of earnings per share – still sits as a midpoint of $9.26.

As you can see below, shares are trading at 11.6 times price to adjusted FFO (p/AFFO). That’s well below its normal valuation of 24.2 times. And its dividend yield is 6.2% and well-covered by a 73% payout ratio.

Source: FAST Graphs

Importantly, a reduction in interest rates could spark demand and reignite the fund flows from venture capital firms into the life science sector. This makes Alexandria a high-conviction pick that could return 30% or more over the next 12 months.

Health Care REIT 2: Healthpeak Properties

Healthpeak Properties (DOC) is a leading health care REIT that owns:

-

Life science properties (35% of revenue)

-

Medical office buildings (49% of revenue)

-

Senior housing properties (11% of revenue)

Collectively, its 700 properties amount to 49 million square feet of space worth an estimated $24 billion. And with its $13 billion market cap, Healthpeak is the fourth-largest health care REIT in our coverage spectrum.

Its nationwide markets include – but aren’t limited to – San Francisco (23%), Boston (10%), Dallas (8%), San Diego (5%), Houston (4%), and Tampa (4%). Meanwhile, its customer base consists of categories from health systems (it’s largest tenant type) to physicians, bio corporations, and medical device companies.

Healthpeak’s strong balance sheet is highlighted by 5.2 times net debt to earnings before interest, taxes, depreciation, and amortization. It has $2.3 billion in liquidity and a BBB+/Baa1 credit rating with a 38% debt ratio.

On Healthpeak’s second-quarter 2025 earnings call, CEO Scott Brinker pointed out that there has been “a couple of $10 billion” merger and acquisition (M&A) “deals recently, which allows capital to be recycled back into the ecosystem.” He believes those consolidations, “along with political and regulatory stability, should help jumpstart public and private capital raising, which is the key to an improvement in new leasing.”

As you can see below, shares are trading at 11.1 times p/AFFO, much lower than their normal 17 times valuation. The REIT’s dividend yield is 6.6%, and it’s covered by a 72% payout ratio.

Source: FAST Graphs

Similar to Alexandria, we see Healthpeak generating strong total returns of 30% or more over the next 12 months.

(We recently interviewed Healthpeak CEO for our Wide Moat Letter Premier members. That’s just one of the perks they’ve come to expect with this service.)

Health Care REIT 3: Global Medical REIT

Global Medical REIT (GMRE) is a net-lease health care REIT that owns 193 properties amounting to 4.9 million square feet. Seventy-one percent of its 297 tenants are in medical office buildings and 17% in inpatient rehab facilities.

GMRE’s portfolio is geographically diversified across, with its largest presence in Texas, followed by Florida and Ohio. Its average occupancy is 96.6%.

Although smaller than the previously referenced REITs with a market cap of $508 million, it’s still worth knowing about. New CEO Mark Decker, Jr. is working “to take [Global Medical’s] 100% unsecured balance sheet into more of a competitive advantage with the establishment of a long debt maturity ladder.”

I’ve known Decker for over a decade now in his previous executive and investment banking roles. So I have a good feeling about what he can do with GMRE… especially since he bought $1 million worth of shares after taking over as CEO, showing that he has skin in the game.

It also doesn’t hurt that the REIT cut its dividend right before he came. That means GMRE has more financial resources to work with now under his leadership.

As you can see below, shares are trading at 8.5 times p/AFFO – below their normal valuation of 13.2 times. And the dividend yield is a juicy 7.9%.

Source: FAST Graphs

Once again, I see Global Medical returning 30% or higher over the next 12 months.

Regards,

Brad Thomas

Editor, Wide Moat Daily

P.S. I hope you enjoyed this health care REIT article. And don’t forget I’ve got one more REIT review to do this week. Make sure to tune into The Wide Moat Show on YouTube tomorrow, where my co-host, Nick Ward, and I will be discussing “Nothing but Net-Lease” REITs.

|