I met with my mother over the weekend to discuss a rental property of hers.

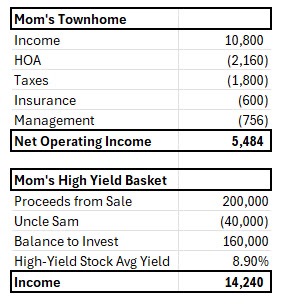

She has owned this townhome for over 25 years now and is currently renting it at a below-market rate. So below market, in fact, that after deducting HOA expenses, taxes, and management fees… she has very little left over for herself.

So, is it really worth the hassle?

Neither of us think so.

She could get a new tenant, sure. But that would require replacing the carpet and repainting the inside of the property. Plus, she’d still have to deal with the draining three Ts. Those would be the profit-reducing, time-consuming issues of taxes, trash, and tenants.

Another option would be to make a 1031 exchange, where she sells the property and puts the proceeds into a new one. In so doing, she’d avoid capital gains taxes from the sale. But all the other taxes (and the other two Ts) would still be her burden to bear.

Or she could invest the proceeds in a Delaware Statutory Trust (“DST”). This is similar to a 1031 exchange but is designed to aggregate fractional stakeholders, much like a real estate investment trust, or REIT.

Unfortunately, her equity here is under $250,000, whereas most DST investors have over $1 million to invest.

My mom wouldn’t have to deal with common landlord issues anymore after that, it’s true. However, DSTs aren’t that liquid, leaving her at an automatic investment disadvantage.

Recognizing all of this, she has decided to do something very simple – sell the property outright and put the proceeds into a high-yield investment.

So, I’m exploring some options for her.

There are several investment categories that offer this kind of potential, including business development companies (“BDCs”), mortgage REITs (mREITs), and “regular” equity REITs.

But it can take significant time to sort through them. Fortunately, that’s what her son does for a living…

Here’s what I came up with.

My BDC Pick for Mom

Business development companies are closed-end funders specifically designed to assist companies that would otherwise struggle to get loans.

To be clear, these companies don’t struggle for loans because they’re bad businesses. Very often, it’s because they’re medium-sized businesses – the type that are too big for a community bank but too small for the mega-banks (JPMorgan Chase, Goldman Sachs, et al.) to bother with. This middle ground is where BDCs thrive.

Like the REITs I write about so often, they pay no taxes on their annual income. In return, they distribute at least 90% of that money to their shareholders.

There are risks, of course.

As I wrote a few weeks ago:

Their typical clients are smaller companies valued at less than $5 billion – often those that have been taken private in leveraged buyouts.

If that sounds a bit risky, it can be. That’s why BDCs tend to come with double-digit yields that could tempt even an investment saint. These days, most yield 11% or higher.

And every once in a while, that yield is a true bargain.

That’s my assessment of the BDC, Blue Owl Capital Corp. (OBDC), which boasts a well-covered payout ratio of 94% and a solid balance sheet. Leverage sits at 1/17 times debt to equity, and S&P gives it an investment-grade BBB- rating.

Yet shares have sold off over the past few months, taking its dividend yield up to 12.2%. That’s because we’re in an interest-rate-cutting environment, and BDCs tend to do much better under higher-rate conditions.

Certainly, Blue Owl has around 98% of its portfolio anchored by floating-rate loans. So, there will almost certainly be a decline in net interest income, BDC’s proxy for earnings.

But I’m confident that Blue Owl will survive and even thrive nonetheless, given its safer payout ratio. Likewise, its portfolio has real credit quality, with only 0.8% of assets at real risk of default.

And we can’t ignore its ties to the parent company, Blue Owl Capital (OWL). That asset manager – which has over $152 billion of assets under management – is OBDC’s “big brother” that provides significant sourcing options and a significant overall advantage for OBDC.

Shares are now trading at $12.14 per share with a price-to-earnings (P/E) multiple of 7.5 times compared with its normal 9.3 times. While I don’t expect considerable multiple expansion here, I could see shares returning 15% over the next 12 months – mostly from their 12.2% dividend and some modest capital gains.

My Commercial mREIT for Mom

Mortgage REITs, like BDCs, are lenders and debt owners. And since they handle real estate-specific assets, they’re extremely sensitive to interest rates and a whole host of other factors.

That’s why I usually don’t recommend them to retirees – or at all.

Ladder Capital (LADR) stands out from the pack, though. As a commercial mREIT, it generates income from its diversified investments of:

-

Senior secured loans ($1.9 billion)

-

Securities ($1.9 billion)

-

Commercial real estate equity ($960 million, mostly consisting of net-lease properties)

This REIT lender focuses on smaller loan sizes, averaging around $30 million, one of several aspects that differentiate it from its peers. It’s therefore isolated from large write-offs that can significantly hurt it and its investors.

Ladder also has a better balance sheet than the competition, not to mention a reliable funding profile. As of the third quarter of 2025, its liquidity was $879 million, comprised of cash and cash equivalents and undrawn capacity of $850 million on its unsecured revolver.

Shares are now trading at $10.58 with an 8.7% dividend yield. Their P/E multiple is 10.9 times compared with the norm of 11.4 times.

What excites me most about Ladder is its consensus estimates of 28% in 2026 and 18% in 2027. This suggests more dividend growth in the future, as well as enhanced total return prospects.

It also doesn’t hurt that management and directors own around 11% of the company. So, their interests are directly aligned with investors.

I suspect shares could return 15% or more over the next 12 months, including that 8.7% dividend I mentioned and modest appreciation in the share price.

My Equity REIT for Mom

Finally, we have Mom’s equity REIT pick, a category that has much more to offer in this high-income, low-risk quest. Though few picks are quite as impressive as the monthly dividend favorite Realty Income (O).

This net-lease REIT owns a portfolio of over 15,500 properties in the U.S. and Europe. Its highly diversified customer base includes many well-known brands such as 7-Eleven, Dollar General, FedEx, Tractor Supply, and Home Depot.

O’s European exposure provides it with even further geographical diversification, plus cheaper debt issuance, which reduces the company’s overall cost of capital.

Another advantage for Realty Income is its balance sheet. Rated A- by S&P, its net debt to annualized pro forma earnings before interest, taxes, depreciation, and amortization is 5.4 times. It has a fixed-charge coverage ratio of 4.6 times. And it also boasts $3.5 billion of liquidity.

Shares are now trading at $56.38 with a 5.7% dividend yield and a price to adjusted funds from operations multiple of 13.3 times. That’s extremely low compared with its normal 17.2 times.

Considered one of the safest equity REITs out there, Realty Income has a track record of paying and increasing its dividends for over 30 years in a row.

Given its margin of safety, dirt-cheap valuation, dividend yield, and forward dividend growth of about 4% per year, I expect a 20% to 25% return over the next 12 months.

The Sum of the High-Income Parts

Using an equal-weight portfolio, the average dividend yield for this three-stock suggestion is 8.9%, with an average total return target of 13%.

After selling her townhouse and paying Uncle Sam his (hopefully modest) fee, my mom can invest the proceeds into these liquid stocks.

If all goes well, she can generate around 160% more income than she’s currently getting… while simultaneously giving up the stress that automatically comes with the landlord’s three Ts.

It seems like a win-win to me.

We’ll see if Mom agrees.

All the best,

Brad Thomas

Editor, Wide Moat Daily

|