On January 12, I wrote about “Trump’s War on Corporate Landlords.”

It detailed big companies that buy up single-family homes to turn them into rental properties, and how – out of the blue – President Trump decided to target them as perpetrators of today’s housing crisis.

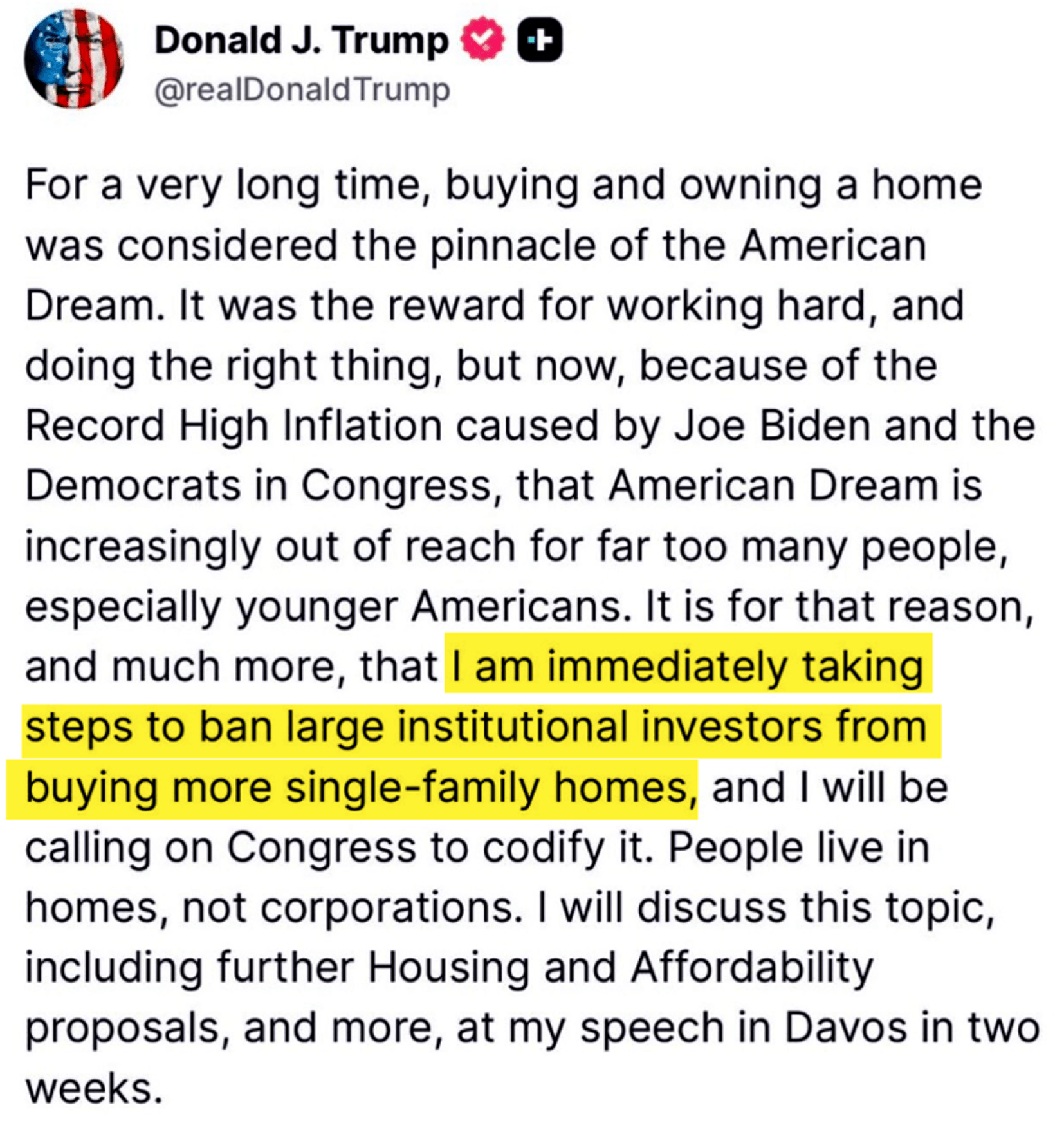

Here’s what he wrote on Truth Social days before (emphasis added):

Source: Truth Social

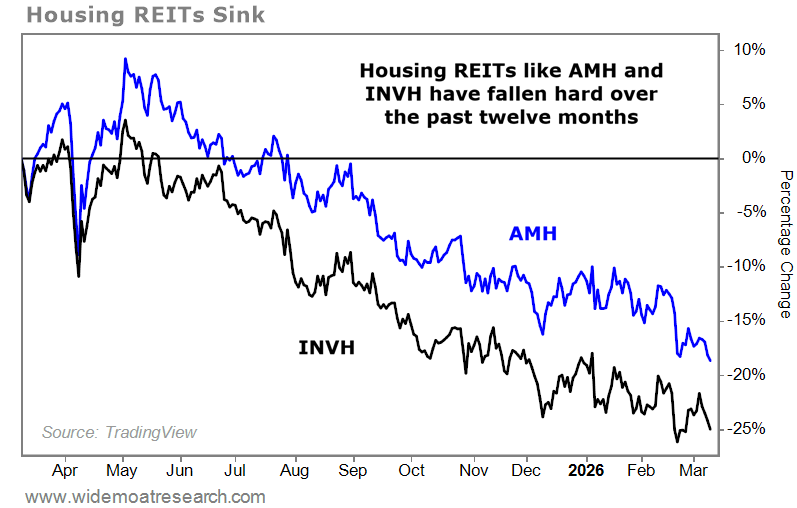

As I noted in my subsequent article, “Just like that, the markets lost confidence in” single-family rental (“SFR”) real estate investment trusts (“REITs”), “sending them down about 6% in a single day.”

And they’ve continued to struggle ever since.

Now, on the one hand, I get the frustration. For many, the American Dream of owning your own home is just that – a dream.

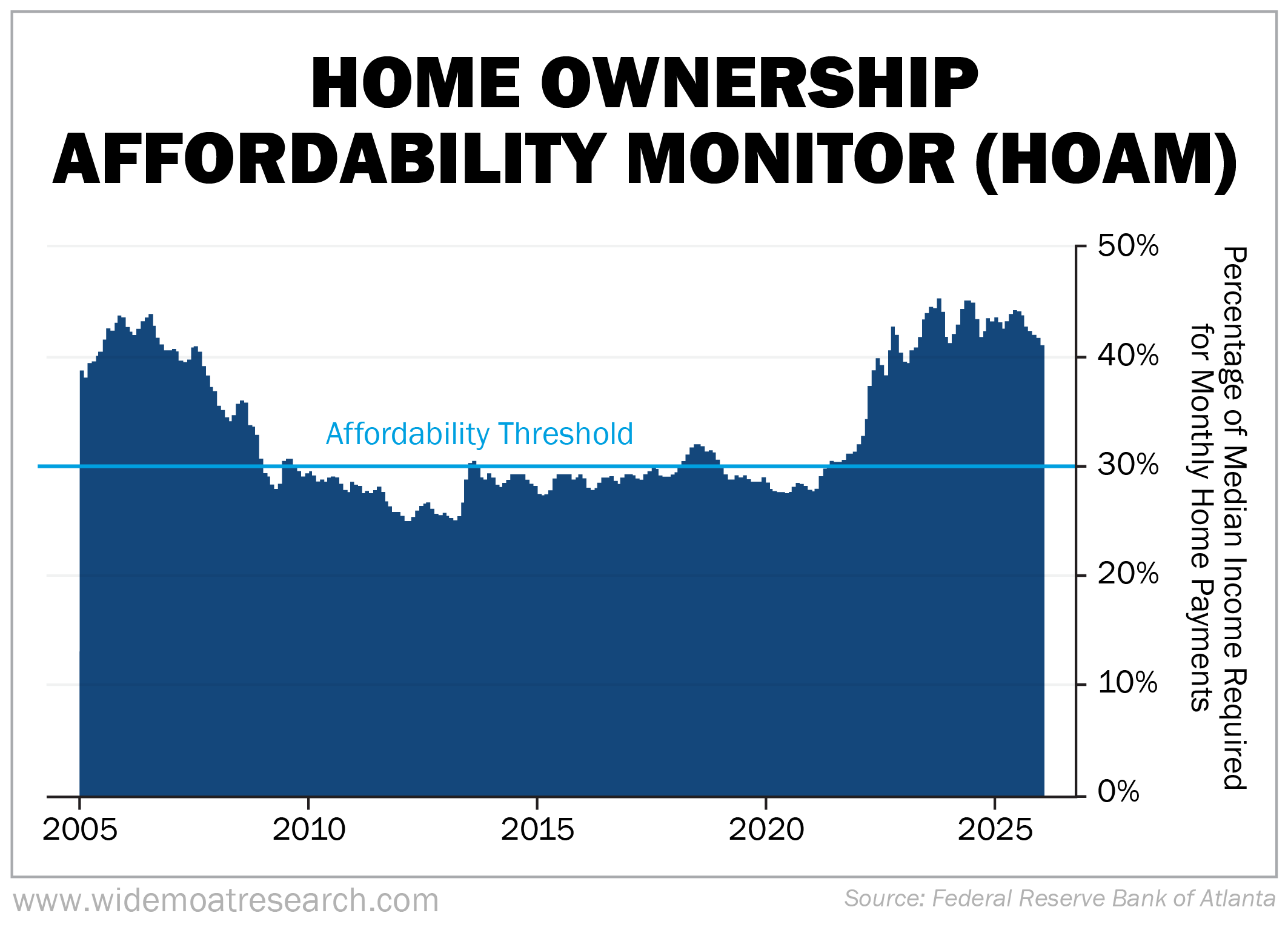

Housing is far from affordable right now. Have a look at the next chart.

This is the Home Ownership Affordability Monitor (“HOAM”) from the Atlanta Fed. It shows what percentage of a median income is required to make monthly payments on a median U.S. home. And at 41%, it’s well above what’s considered the “affordability threshold.”

So, yes, something should be done about housing affordability.

I just disagree with Trump that limiting SFR REITs is the best “something” available.

As I shared in the original article, institutional investors with more than 2,000 homes in their portfolios account for less than 0.5% of the U.S. single-family housing stock. Banning them from this market won’t meaningfully impact prices, but it will remove a source of liquidity that comes in handy during difficult housing markets.

My hope had been for wiser ideas to prevail, and that could still happen. But the Senate just advanced the ROAD to Housing Act of 2025 last week, which isn’t good for SFR landlords of any kind with over 350 properties.

And so, it’s time to revisit the war on corporate landlords.

The Ins and Outs of the ROAD to Housing Act

First, let’s discuss the “Renewing Opportunity in the American Dream” or ROAD to Housing Act. It seeks to boost the housing supply by:

-

Updating available financing options

-

Cutting, easing, or streamlining regulatory headaches

-

Improving oversight of federal housing programs

The Senate Banking, Housing, and Urban Affairs Committee all gave it unanimous support last July – a bipartisan miracle, it appeared – and then there was Wednesday’s action to approve its latest version altogether.

The current piece of legislation merges one bill from last year and another that the House passed in February, with more added into it along the way. So Congress’s next step is to agree on a final version… which it might manage to do in fairly short order.

After all, it was Senators Elizabeth Warren (D-MA) and Tim Scott (R-SC) who led this latest round of votes. And while some die-hard Trump supporters might doubt Scott’s conservative credentials, Treasury Secretary Scott Bessent has also come out in support of the ROAD to Housing Act.

So, it somehow seems to make everyone happy.

Everyone except SFR-investing and affiliated corporations, anyway. That’s because, to quote BMO Capital Markets:

The latest draft [of the ROAD legislation] would prohibit additional home purchases by investors above the threshold, while grandfathering existing portfolios. However, the revised bill calls for a 7-year disposition requirement on future homes acquired, including built-to-rent [“BTR”], which was a negative surprise.

Forced resales would likely inhibit capital to develop homes given greater uncertainty on exit economics. Homebuilders wouldn’t have the ability to de-risk with BTR to third-party investors/REITs. Also, if REITs aren’t able to grow, it may hinder reinvestment.

These are genuine concerns that should not be ignored.

Looking at the SFR REIT Landscape Today

There are four single-family rental REITs within our Wide Moat coverage spectrum:

-

American Homes 4 Rent (AMH)

-

Invitation Homes (INVH)

-

Bluerock Homes Trust (BHM)

-

NexPoint Diversified Real Estate Trust (NXDT).

And it must be noted that AMH and INVH, the biggest players, already saw softer-than-expected new-lease trends in the fourth quarter of 2025. That and weaker-than-expected pricing trends with the potential for higher churn.

Specifically, INVH reported core funds from operations (“FFO”) per share of $0.48, up 1.3%, and full-year 2025 core FFO of $1.91. It acquired 368 newly built homes in the fourth quarter for $123 million and sold 315 for $138 million.

AMH generated FFOD of $0.47 per share, up 4.1%, and full-year core FFO of $1.87 per share, which was up 5.4%. It sold 646 homes, generating $190 million in net proceeds, and 1,827 homes for the full year, with net proceeds of $570 million.

Those properties are regularly sold to individual homeowners, providing these REITs with a highly attractive form of capital to reinvest. And, as mentioned earlier, forced resales would probably do more harm than good, restricting capital to develop further.

Rich Hightower, managing director and REIT analyst at Barclays, recently hypothesized that:

The best thing for the [SFR] sector is probably just to get through the midterm elections because some portion of all of this has got to be election posturing and… some really counterintuitive ways to try to increase housing supply, which is, at the end of the day, what really solves the affordability problem.

He added, “All you can hope for is that saner heads prevail in Congress, and we’ll see what happens… Maybe gridlock is the ideal scenario.”

As it is, single-family rental REITs trade at about a 30% discount to net asset value (“NAV”). And they could be headed lower still.

I continue to believe these companies can find a way through this mess. They were literally forged from bad times. Many sprang up in the aftermath of the mortgage crisis post-2008. It proved that necessity really is the mother of invention.

This is why I’m not ready to shun the sector altogether – especially at such bargain-bin prices. But it is looking like their existence will become more complicated than I had previously hoped.

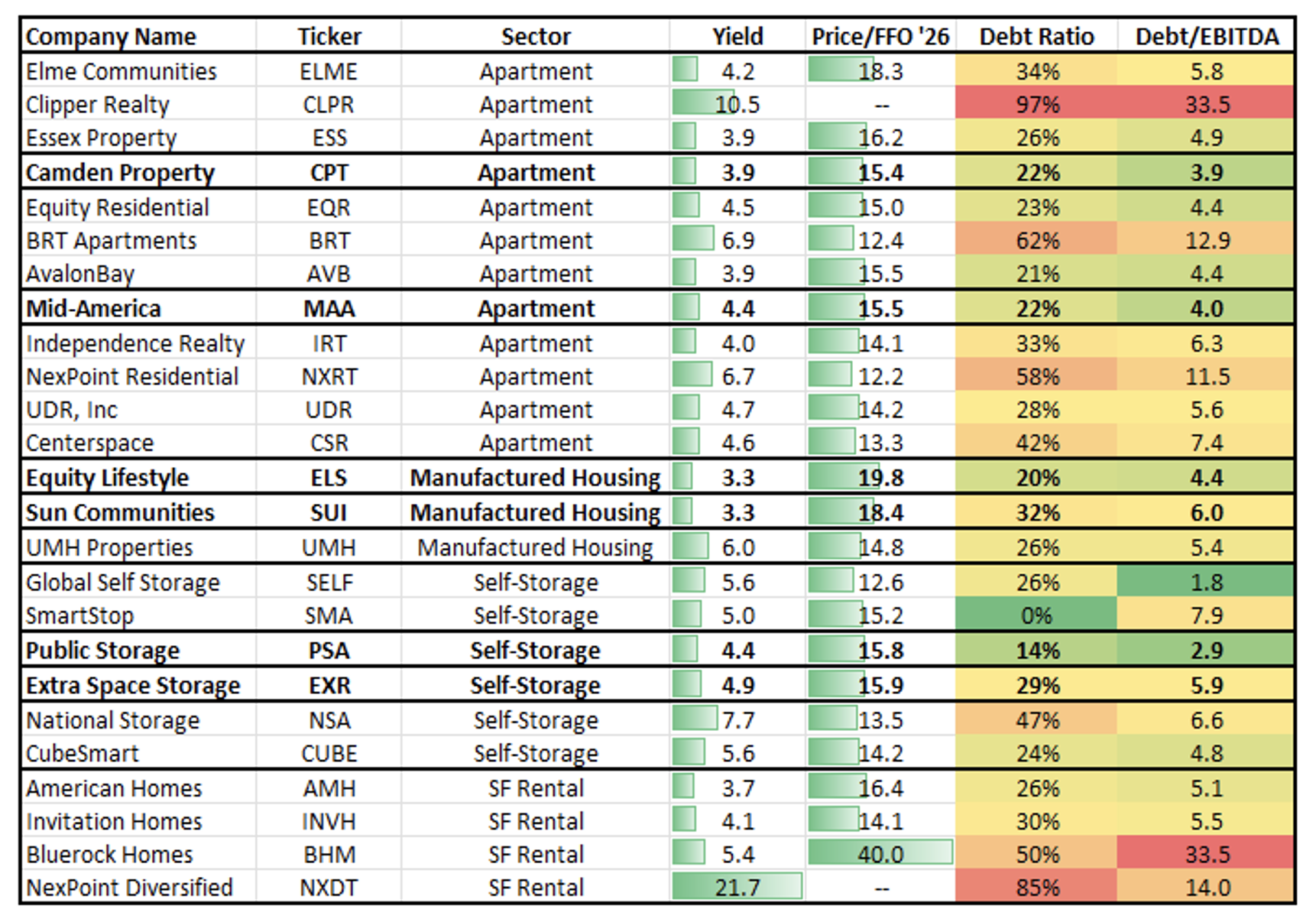

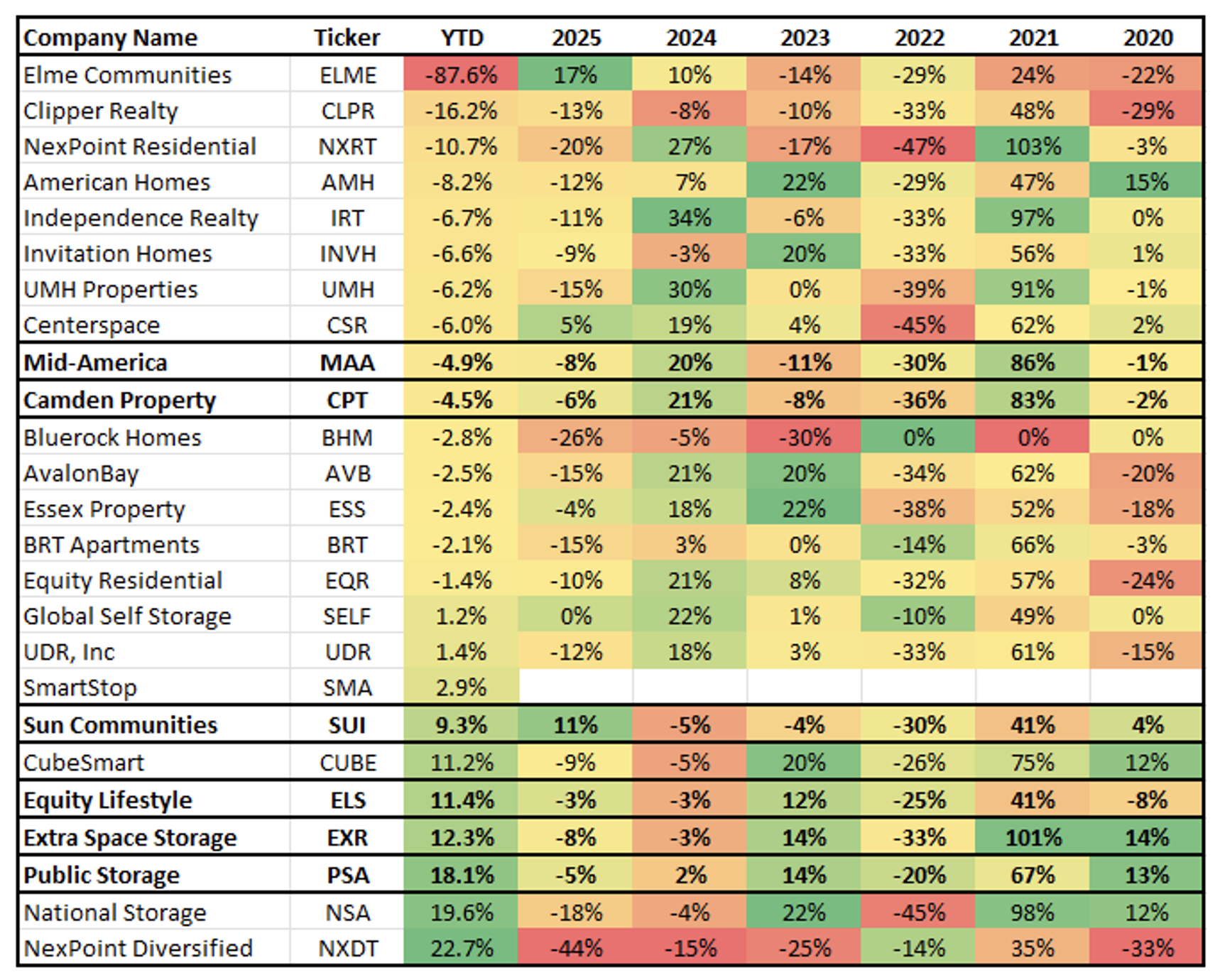

So, for those who aren’t willing or able to take a chance… consider moving your money to apartment REITs with stable occupancy and renewal rates. Self-storage, apartments, and manufactured housing, with their steady pricing updates and improved occupancy, could be other worthwhile considerations.

Source: Wide Moat Research

My top picks in these categories include Mid-America Apartment Communities (MAA), Camden Property Trust (CPT), Public Storage (PSA), Extra Space Storage (EXR), Sun Communities (SUI), and Equity LifeStyle Properties (ELS). They’re each strong, stable companies with promising futures.

Better yet, there’s no reason for the government to pick on them anytime soon.

Source: Wide Moat Research

Happy SWAN (sleep well at night) investing!

Brad Thomas

Editor, Wide Moat Daily

|