The new year has only just begun, and it’s already pretty interesting.

Of course, there was the military intervention in Venezuela, which, according to the White House, doesn’t necessarily mean the U.S. is at war with the country.

But, just yesterday, President Trump did declare his own personal war – one on large financial institutions buying single-family homes (“SFH”).

I’ll have more to say on that latter topic soon. And watch for tomorrow’s issue, where Stephen Hester will break down what the Venezuela developments likely mean for the energy markets.

But, for right now, I’d like to continue our examination of which property sectors are likely to thrive in 2026 after an underwhelming run last year.

And today, we’ll turn to one of the unlikeliest places for shareholder returns…

No Muss, No Fuss

Maintaining real estate of any kind is almost always a time-consuming, money-draining venture.

Whether we’re talking about homeownership, where a 30-year mortgage can easily double the cost of a house – not to mention all the repairs, replacements, and renovations that tend to come up along the way – or commercial real estate (“CRE”) that suffers its own wear and tear, complete with typical (and atypical) tenant hassles…

It can be overwhelming.

Don’t get me wrong. I’m all about holding CRE. I’m the proud owner and partial owner of multiple properties in addition to my house. And I’m always looking to add to that portfolio.

It’s just that, as a landlord who has worked with big-name corporations from Walmart (WMT) to Papa John’s (PZZA) to Advance Auto Parts (AAP), and plenty of smaller businesses, too, I understand the cost involved. It can be pretty taxing, all things considered.

There are notable exceptions, however. And one such beacon of leasing ease is the self-storage sector.

You know what I’m talking about: those facilities down every other road that offer out-of-home “closet space” when people’s regular closets just aren’t big enough. They might seem like humble operations, but there’s much more to them than meets the eye.

Sergio Altomare, co-founder and CEO of Hearthfire Holdings – a real estate private equity and development firm with over $180 million in self-storage assets under management (“AUM”) – recently released his 2026 Self-Storage Investment White Paper. In it, he notes that this CRE sector “has transformed into a data-driven subscription business anchored in real estate, offering unparalleled investment opportunities.”

I agree. And I want to make sure you understand self-storage’s profit potential, too.

The Ins and Outs of the Self-Storage Business

Here are some stats Altomare cites about the self-storage industry:

-

It runs with 65% to 75% net operating income (“NOI”) margins, which are the highest you’ll find in CRE.

-

The fact that it works with month-to-month leases instead of annual contracts allows it to battle inflation much more easily than most other rental properties, giving it stronger pricing power.

-

Because people need storage space both when they’re downsizing during hard times and upsizing during good times, it features “recession-resistant demand with counter-cyclical characteristics.”

-

Large operators (i.e., real estate investment trusts, or REITs) are optimizing revenue even further with digital ecosystems that utilize omnichannel digital tools to lease space. These platforms include social-media accounts, call centers, click-to-chat website options, and contactless check-in.

I say “even further” because self-storage facilities, in and of themselves, are actually very cost-efficient from start to finish.

They require fewer bells and whistles to be built, for one thing. There’s minimal plumbing necessary, no bathrooms, few windows, and only the most basic electrical setups. And once the building is up and running, the plumbing is only necessary for fire-safety purposes, and lighting is used minimally.

After all, piles of furniture, boxes of old clothes, and assorted stacks of other stuff only need to be seen when a human is present. And humans mostly utilize their self-storage units when they’re moving in or moving out.

For that same reason, these buildings require minimal staff. Depending on the size of the facility, they might need one to three people manning the front desk, and then one to two people for security and/or maintenance purposes. That’s it.

As for self-storage customers, they tend to stick around for 18 to 24 months at a time. And once one leaves, another tends to step into that empty space quickly enough. Around 33% of Americans use self-storage at any given time, and another 18% say they intend to in the future.

All put together, these businesses – when run the right way – can be a great place to park one’s cash.

How Self-Storage REITs Stack Up

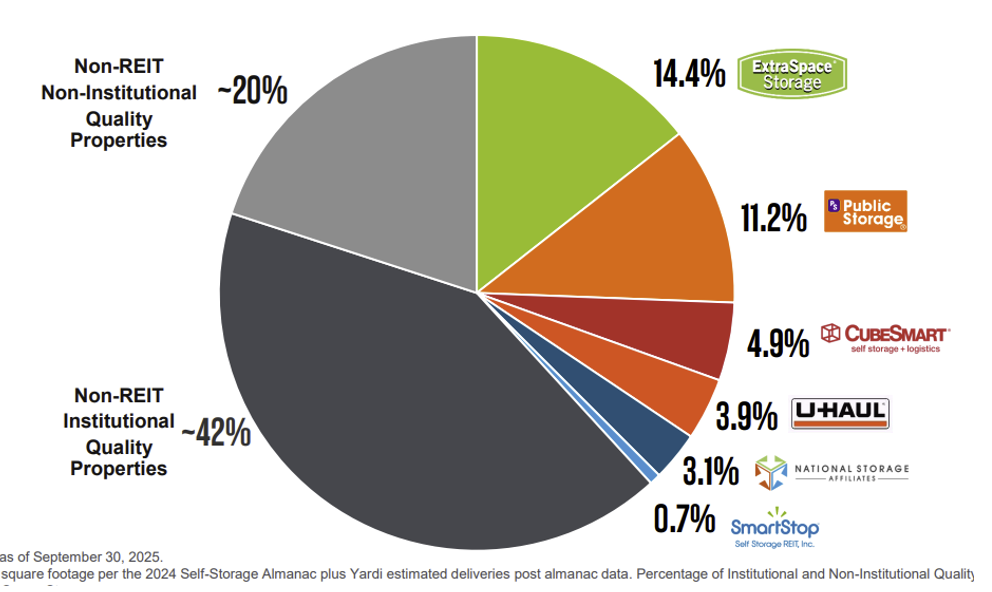

There are around 52,000 self-storage properties in the U.S., representing over 2 billion square feet of rentable space. U-Haul (UHAL) owns 3.9% of that market share, while another 35% is held by REITs.

Source: Extra Space Investor Relations

Now, I’ve already laid out how easy it is to own and operate a self-storage facility compared with other properties. But you can make it easier still when you invest in those REITs. That way, you don’t have to manage the properties, market the properties, or, most importantly, guarantee the debt on these properties.

When you own a REIT – any REIT – you’re essentially a virtual landlord. So you just sit back, collect your dividends, and watch your shares work for you while you sleep.

Some are better than others, of course. And that’s why the Wide Moat Research team designed a screening tool to highlight those with the best quality rating.

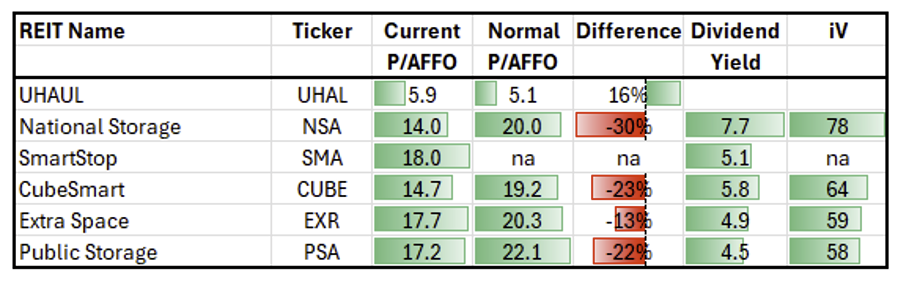

When it comes to the self-storage space, including U-Haul, here’s how these players rank:

Source: Wide Moat Research

[Notes: REIT growth refers to adjusted funds from operations (“AFFO”). UHAL growth is earnings before interest, taxes, depreciation, and amortization (“EBITDA”). iQ refers to quality score.]

As you can see, Public Storage (PSA) and Extra Space (EXR) screen the best with their superior debt ratings. And Public Storage specifically has the lowest payout ratio in the REIT sector based on AFFO per share.

Quality isn’t the only consideration we take seriously at Wide Moat Research, though. Price tags matter, too, so we also want to consider valuation.

Source: Wide Moat Research

[Notes: SmartStop held its IPO in April 2025. Therefore, we don’t have enough data to determine a “normal” valuation. iV refers to value score.]

National Storage (NSA) is the cheapest of the lot, trading at a 30% discount to its normal valuation multiple. However, that makes sense considering what shows in the first chart.

With an elevated payout ratio of over 100%, it’s at serious risk of having to cut its dividends. We therefore recommend avoiding it for the time being.

Instead, we’re turning back to Public Storage and Extra Space. Extra Space has better cost of capital and a safer dividend… but I’m also very bullish on Public Storage.

In fact, I featured it on today’s Wide Moat Show on YouTube as one of my top REITs to buy this year. You can discover the full list right here.

Storage facilities might not seem exciting, but that’s actually part of their appeal. For investors looking to build out the REIT segment of their portfolio for the new year, these businesses deserve some consideration.

Regards,

Brad Thomas

Editor, Wide Moat Daily

|