The push for artificial intelligence (“AI”) is enormous these days – more so than you probably realize.

My trusted associate, Leo Nelissen, recently showed how AI data center capital expenditures (capex) “now accounts for 1.2% of total U.S. GDP.” Not technology in general. Not even artificial intelligence in particular. It’s the capital to support the infrastructure for it.

The last time we saw such an imbalance, he notes, was in 2020, when telecom spending took up 1% of GDP. “The only spending that was much higher was railroad spending in the 1880s, which makes sense,” as it’s “much more capital-intensive and… the 1880s economy wasn’t very diversified.”

Leo went on to write how:

… AI is so disruptive that the Big Tech companies all have to spend hundreds of billions of dollars to stay ahead of the game, as falling behind in this trend could be costly.

The four biggest AI hyperscalers in the U.S. alone, Alphabet (GOOGL), Amazon (AMZN), Meta (META), and Microsoft (MSFT), spent $72 billion on capex in 2020. This year, that number is expected to be $278 billion. In 2027, it could exceed $330 billion.

Again, this is from just four companies.

Despite these massive expenditures, Big Tech is anything but cheap after generating so much hype for so long.

Enthusiasts will argue this conclusion discounts AI’s massive growth potential. And in that, they’re somewhat right.

A company’s fair market value is rarely based on its current performance alone. It also takes future growth into account – but only up to a certain point. And I think we reached that point quite a while ago.

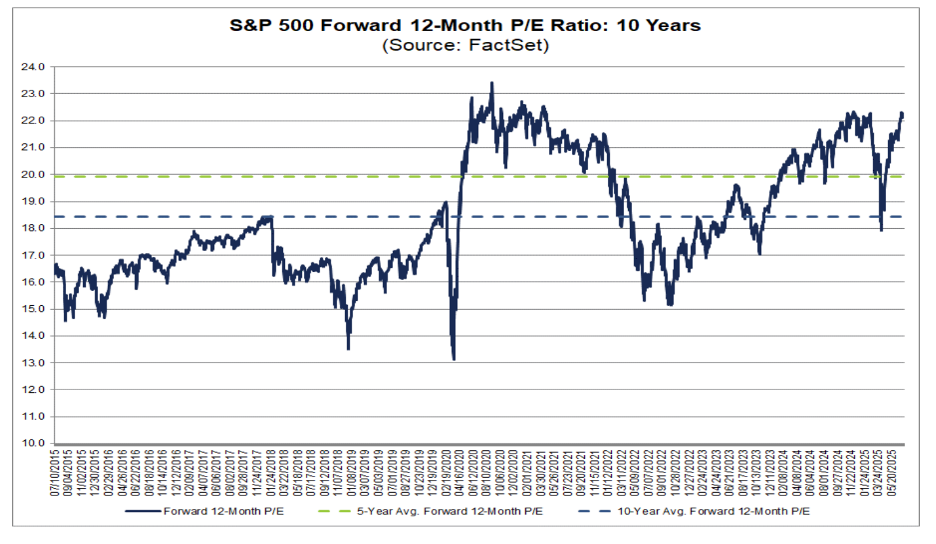

When the S&P 500 trades above 22 times forward earnings, almost exclusively because of Big Tech pricing power… it’s wise to look elsewhere.

Source: FactSet Earnings Insight

So that’s precisely what Wide Moat Research is doing.

AI Investing Has Gone Overboard

Remember, the S&P 500 is a cap-weighted index. The bigger a company is, the more weight it gets. And the Big Tech firms are very, very big.

The top 10 holdings in the S&P are:

-

Nvidia (NVDA)

-

Microsoft (MSFT)

-

Apple (AAPL)

-

Amazon (AMZN)

-

Meta (META)

-

Broadcom (AVGO)

-

Alphabet (class A) (GOOGL)

-

Alphabet (class C) (GOOG)

-

Berkshire Hathaway (class B) (BRK-B)

-

Tesla (TSLA)

Combined, these 10 companies make up about 38% of the index’s weighting. And with the sole exception of Berkshire, they’re all tech.

When I said the S&P 500’s forward earnings are “almost exclusively because of Big Tech,” I wasn’t being hyperbolic. To quote DV Investment:

Microsoft just hit a record high, driven by AI, cloud services and stable earnings – now worth more than Germany’s DAX index and bigger than the UK economy. Nvidia [NVDA] is bigger still, holding 7.3% of the S&P 500…

Microsoft, Apple, and Nvidia now make up over 20% of the entire S&P 500. The top 10 stocks make up 38%. That’s the most concentrated we’ve seen the index in over 50 years.

As for the S&P 500 itself trading 22 times forward earnings, that’s a level we haven’t seen since the go-go years of 2020 and 2021 and only exceeded by the dot-com era.

As our own Nick Ward put it in a recent update to Wide Moat Letter subscribers:

Those premiums [for the S&P 500] are concerning in their own rights. If the S&P 500 were to see its multiple contracts fall in line with [historical] levels, we’d be looking at a significant double-digit sell-off between now and the end of the year.

But what makes matters worse, is that full-year S&P 500 [earnings-per-share] expectations are being built upon the back of accelerating growth expectations into the end of the year… and there are no guarantees that will actually happen.

This is something I’ve warned about more than once over the past few years. I’m old enough to remember what happened to the dot-com bubble in 2000 and the housing market in 2008.

Too much enthusiasm led to too little wisdom… which led to large losses I don’t want any part of. I already experienced the devastation firsthand 17 years ago. And I know many other people who suffered the same in similar market collapses.

Buying into overvalued assets is simply not a risk I’m willing to take today.

But, believe it or not, none of this is meant to put a damper on any tech enthusiasts out there. Brick-and-mortar guy though I am, I fully understand the excitement about today’s technological advancements and their investments potential.

I’m even personally invested in some and/or recommend them.

It’s just that, overall, considering current multiples, I prefer a backdoor approach to buying AI assets. And one of my favorite ways is through mission-critical data centers.

Energy Is a Great Way In

Back in June, I wrote how:

Artificial intelligence requires enormous amounts of data and compute to operate. And while the data AI consumes in its quest to “learn” already exists, it then produces even more.

That information needs to be processed and stored somewhere… which is why McKinsey Quarterly predicts global data-center demand could almost triple between now and 2030.

When these companies are properly priced, they can lead to impressive short-term and long-term gains alike.

I stand by that evaluation today. And I’m sure I’ll be writing about data-center opportunities again before long regardless of whether we see an AI market correction.

These companies aren’t just dependent on Big Tech. Their customers range across every single industry – from banks to builders to beverage makers. And as each one of those increases their AI reliance, they’ll automatically need more data-center power as well.

But there are other asset classes that can claim the same, with energy being one of them. To quote Leo again, “energy is critical for global prosperity and inflation resilience.” Plus, despite negativity, oil and gas demand will likely keep rising for decades, driven by growth and AI.”

That kind of thinking is precisely why Wide Moat Research includes the Midwest-focused WEC Energy Group (WEC) in our Wide Moat Letter‘s Core Portfolio. Since June 2024, when we first recommended it, shares have generated total returns of approximately 39.5%.

In that initial coverage, we noted that:

On May 8, Microsoft announced plans to invest $3.3 billion into AI-related infrastructure projects in Southeast Wisconsin. This investment should account for roughly 1,000 megawatts of demand, roughly 10% of WEC’s current power load in Wisconsin.

This past June, then Microsoft’s Corporate Vice President, Rima Alaily, praised those specific efforts, saying:

A year ago, alongside our $3.3 billion infrastructure investment, we committed to using the power of AI to help advance the next generation of manufacturing companies, skills and jobs in Wisconsin and across the country. Thanks to our partnership with WEDC, TitletownTech and UWM, we’re delivering on this commitment. With access to cutting-edge AI technology and technical guidance to bring their ideas to life, we can’t wait to see what Wisconsin companies will build.

AI will only get bigger from here, which is why it’s so worthwhile to invest in it. It’s just a matter of finding assets trading at reasonable levels… and not being pulled higher on excitement alone.

WEC is up 16.5% year to date. That puts it at around $110 per share, which is fair value… for now. Due to the success of Microsoft’s Midwestern tech hub, however, we expect to see other Big Tech firms allocate capex to the region.

That bodes well for WEC’s electricity demand metrics… and ultimately, its earnings and dividend growth prospects.

Regards,

Brad Thomas

Editor, Wide Moat Daily

|