From 2003 to 2008, I worked alongside a regional homebuilder helping develop mixed-use communities in South Carolina.

My partners were highly successful businessmen who had already built thousands of homes over the decades. And while I was mainly involved in the commercial real estate side of the equation, I kept apprised of the residential business.

After all, it was the biggest component of that partnership. It would have been foolish not to.

As such, I knew that third parties did most of the actual developing. There are risks and rewards to self-developing lots, and my partners recognized that they could scale their business faster by using other people’s money in this regard.

Sure enough, they generated some pretty high margins.

Of course, when 2008 rolled around, everything they’d worked so hard on collapsed – including my side of the business. Those devastating losses were why I pivoted to become a Wall Street writer, first as an editor at Forbes and then as the most-followed analyst on Seeking Alpha.

But I never forgot how successful that partnership was… and how it could have continued to be so if we all had just handled it a bit more conservatively.

That’s why I was so interested when homebuilder Lennar (LEN) spun off some of its assets into a real estate investment trust (“REIT”) earlier this year. The new Millrose Properties (MRP) focuses exclusively on land-banking services for homebuilders.

This means it essentially buys up residential-zoned properties, then holds them – for a fee – until its clients are ready to utilize them. That’s just one reason why I think it’s in a great position to profit where my previous partnership ultimately failed.

Millrose’s Basic Business Model Is Working (So Far)

Millrose Properties purchases and develops residential land. Then it sells finished homesites to homebuilders through option contracts with predetermined takedown schedules.

It serves 12 homebuilder clients this way, with 138,691 lots for them to choose from as of the third quarter of 2025.

Almost 20% of these properties are in California. Another 18.4% are in Texas. And it has significant holdings in Florida (12.4%) and South Carolina (7.1%) as well.

Source: Millrose Investor Deck

Despite all the bad news you’ve heard about homebuilders – including here at Wide Moat Daily – Millrose is actually in a pretty good place in its maiden solo year.

For one thing, new home inventory is beginning to recalibrate as builders demonstrate production discipline. They’re learning to maintain homesite takedowns and flex margins rather than seek option terminations.

They’re also doing a lot more land-banking these days. Over the past five years, public homebuilders have increased their exposure to optioned lots from 52% to 74%.

That’s perfectly fine for Millrose. Its proprietary technology-based platform for high-volume, complex transaction processing offers real-time data capture that drives smarter, more informed decisions.

Source: Millrose Investor Deck

In the third quarter, MRP generated net income of $105.1 million, or $0.63 per share. Driven by $179 million in option fees and development loan income, it was nonetheless negatively impacted by one-time expenses associated with debt financing activities.

Its underlying cash-generating capacity, however, remained untouched.

After adjusting for the one-offs and other non-cash items, Millrose’s adjusted funds from operations (“AFFO”) – the REIT equivalent of earnings – was $122.5 million, or $0.74 per share. Of that, it paid out $0.73 in dividends, translating into a 9% yield.

Source: Millrose Investor Deck

Obviously, there’s little history to work with here. But the REIT said on its earnings call that it’s “committed to distributing 100% of earnings to shareholders.”

It’s also “raising guidance for full-year 2025 new transaction funding under other agreements to $2.2 billion, up from previous guidance, and also raising year-end AFFO quarterly run rate guidance to a range of $0.74 to $0.76 per share.”

Evaluating Millrose’s Balance Sheet

This brings me to Millrose’s balance sheet, where its leverage currently sits at 25% net debt to capitalization. Better yet, management has indicated it won’t move above a 33% threshold.

The company is capitalized with $2 billion in senior notes on $9 billion of total assets. It has ample liquidity of about $1.6 billion through cash and its revolving credit facility capacity. And it sports a Fitch investment-grade rating of BBB-.

Not too bad, right?

MRP received $893 million in total takedown proceeds ($852 million net of deposit) for the third quarter. Coupled with $975 million in net borrowings, these finances have been redeployed into new acquisitions with Lennar and other customers.

And the REIT can continue generating compelling returns with its adjusted weighted average yield of 11.3% on new acquisitions.

Source: Millrose Investor Deck

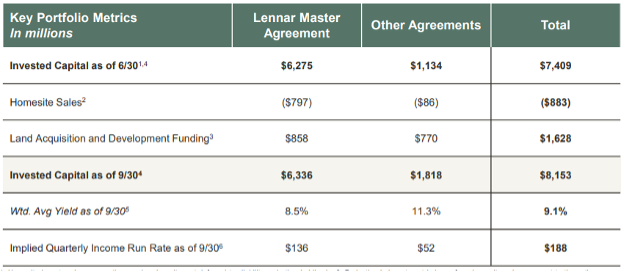

As shown above, the company grew its investments by $770 million in acquisitions and development funding. That brings its invested capital to approximately $1.8 billion.

All told, Millrose’s portfolio-weighted average annualized yield for both Lennar and other customers climbed 20 basis points quarter over quarter to 9.1%.

Source: Millrose Investor Deck

MRP Is a Well-Priced REIT

Because of what it does and how it does it, Millrose doesn’t have any direct peers for comparison purposes. Even so, I consider this “new kid on the block” to be an attractive buy at $33.21, trading at a 12 times multiple.

One analyst I follow uses net-lease REITs as a valuation proxy here. I’m not sure how well that fits, personally, since MRP’s contracts are shorter in duration than the typical net-lease sector’s terms of 15 years or more.

Even so, I think his $40 target and 13 times multiple seem reasonable based on estimated 2026 AFFO.

This would mean 30% returns, which implies around 21% from capital appreciation and 9% from the dividend – a payout that should keep growing based on the demand pipeline of $0.77 in 2026 and $0.79 in 2027.

From everything I see, MRP seems to offer both high income and potential outsized price appreciation. My biggest concern is that it’s externally managed, which can – but doesn’t have to – lead to reduced shareholder power.

The entity in question is Kennedy Lewis Land and Residential Advisors, a wholly owned subsidiary of Kennedy Lewis Investment Management. It’s an institutional alternative investment firm with extensive experience in outsourcing, underwriting, capitalizing, and financing land and homebuilder finance investments.

This past quarter, its management fee expense was $25.9 million, which is calculated at 1.25% of gross tangible assets.

I’ve reached out to a few of its principals over at LinkedIn and hope to speak with them shortly.

In the meantime, Wide Moat Research is officially adding Millrose Properties to its coverage spectrum as a Buy. This is one uniquely positioned REIT where I think you can have both your price-appreciation cake and (9.1%) dividend-yield icing, too.

Regards,

Brad Thomas

Editor, Wide Moat Daily