There are moments in your career when the market teaches you something no textbook ever could.

One of those moments for me happened in Cullman, Alabama – a place you’ve probably never heard of.

At the time, I was developing freestanding net-lease properties for chains like Dollar General (DG), Sherwin-Williams (SHW), and Blockbuster Video. My model was simple, repeatable, and it made me a pretty penny in the process.

I would start out by locking in a “wide moat” client, construct a single-tenant building to spec, clip a steady development yield that was typically around 10%… then move on to the next job prospect on my list.

Since there was always someone out there looking to expand, I had no problem finding that next job. It was practically like printing money.

But, as it turned out, there was better business to be had.

I found that out while scoping out a site for Advance Auto Parts in Cullman, only to find myself in a quandary. The perfect location I’d identified happened to be part of a larger parcel of land that belonged to someone who told me he’d sell it altogether… or not at all.

Most developers would have walked away, but I decided instead to expand my vision. With Advance Auto’s permission, I bought the entire plot with the intention of creating a small shopping center.

And it worked. Only having to pay one engineer, one architect, and one contractor to construct a space for multiple tenants led to cost savings I’d never considered before.

My development yield jumped north of 12%, and, just like that, my business went from good to great.

What does this mean for investors today?

Shopping Centers Are Fundamentally More Profitable

I’m still a fan of single-tenant net-lease properties today. But I also have a much greater understanding of how their landlords’ upside is capped, whereas shopping centers offer:

-

Higher blended rents

-

Tenant mix optimization

-

Better releasing spreads

-

Outparcel optionality

And, most importantly, pricing power over time.

Shopping centers aren’t just buildings, you see… they’re value-compounding ecosystems. That’s why some of today’s most compelling public real estate investment trusts (“REITs”) are shopping center landlords – particularly those with strong grocer anchors, necessity-based tenants, and embedded rent growth.

Source: Wide Moat Research

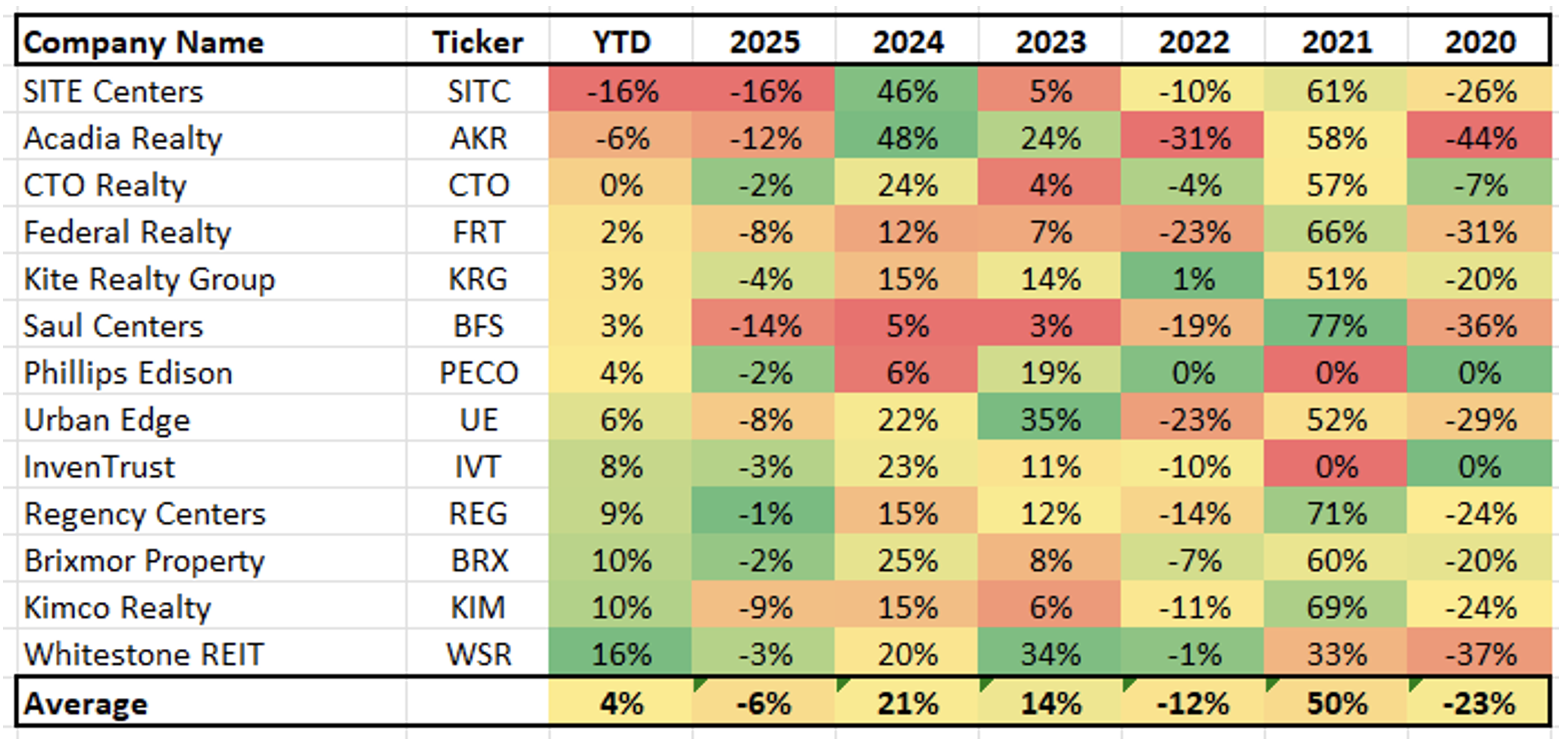

Once I learned that lesson, I started attending the International Council of Shopping Centers (“ICSC”) conference every year in Las Vegas. That’s where I could mingle with gigantic retail REITs like Simon Property (SPG), Kimco Realty (KIM), and Macerich (MAC) that could bring in big business.

Much has changed since those first days of attending, with some companies crumbling under the pressure of the 2020 shutdowns… but many more ended up selling to larger competitors.

For instance, Kimco bought out Weingarten Realty Investors for $3.9 billion in 2021. Regency Centers (REG) acquired Urstadt Biddle Properties for around $1.4 billion in 2023 (after purchasing Equity One for $15.6 billion in 2017). And Blackstone Real Estate took Retail Opportunity Investments private just last year for $4 billion.

Meanwhile, a slew of new REITs went public, such as CTO Realty Growth (CTO) in November 2020, Phillips Edison (PECO) in July 2021, and InvenTrust Properties (IVT) that October.

Source: Wide Moat Research

Even with moderating job growth and consumer pressures, retailer demand for space remains solid. In fact, supply remains minuscule at 0.2% of inventory, with major retailers continuing to sign long-term leasing contracts.

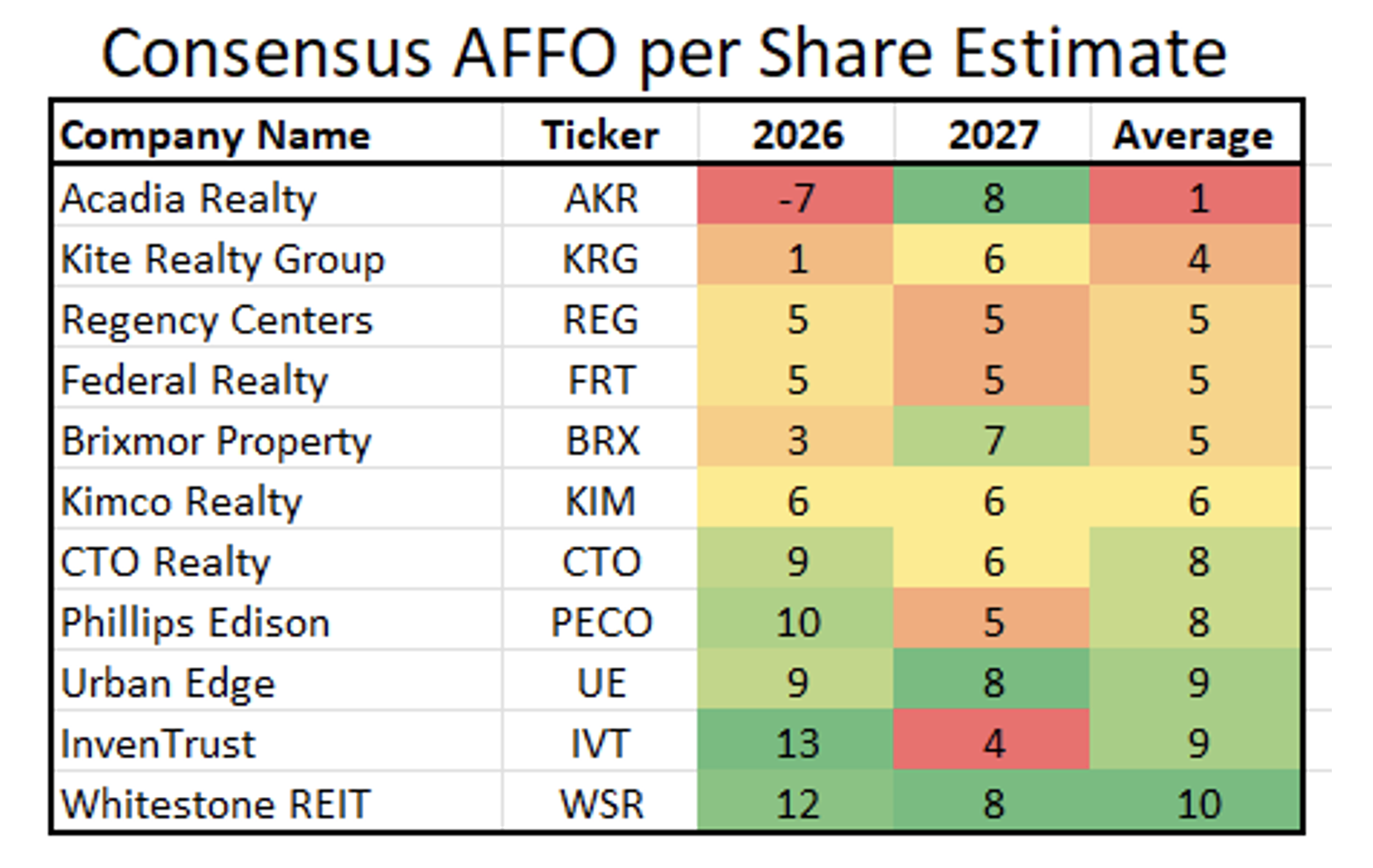

Shopping center REITs are expected to grow per-share funds from operations (“FFO”) by around 5% this year. That would be solid performance given demand uncertainty across various other areas of REIT-dom, such as single-family, multifamily, and storage.

Source: Wide Moat Research

The Shopping Center REITs I’m Most Interested In

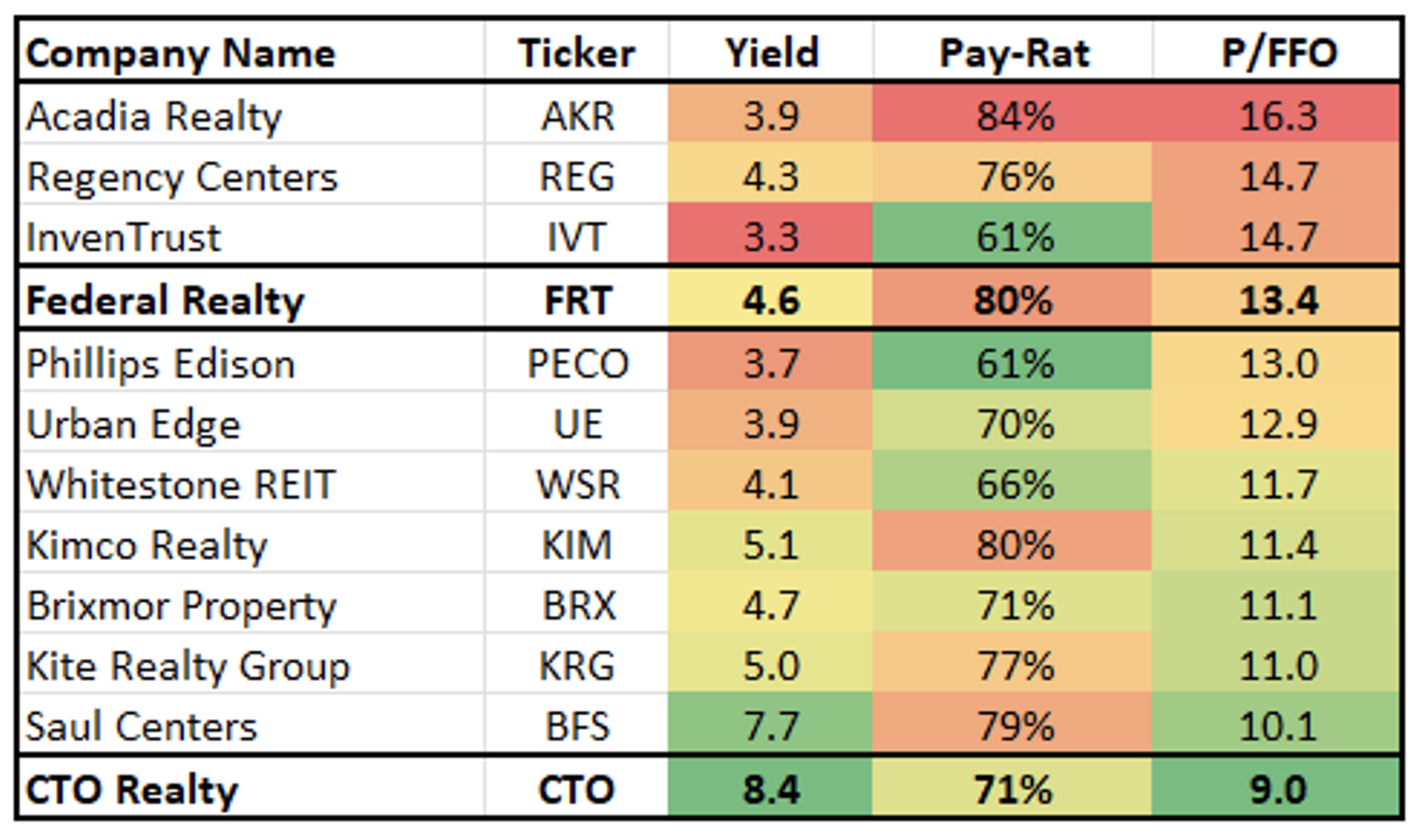

Last week, I wrote about the only REIT Dividend King, Federal Realty (FRT), and its portfolio of 104 open-air properties. Its primary “moat” is how it caters to high-income consumers within dense urban populations.

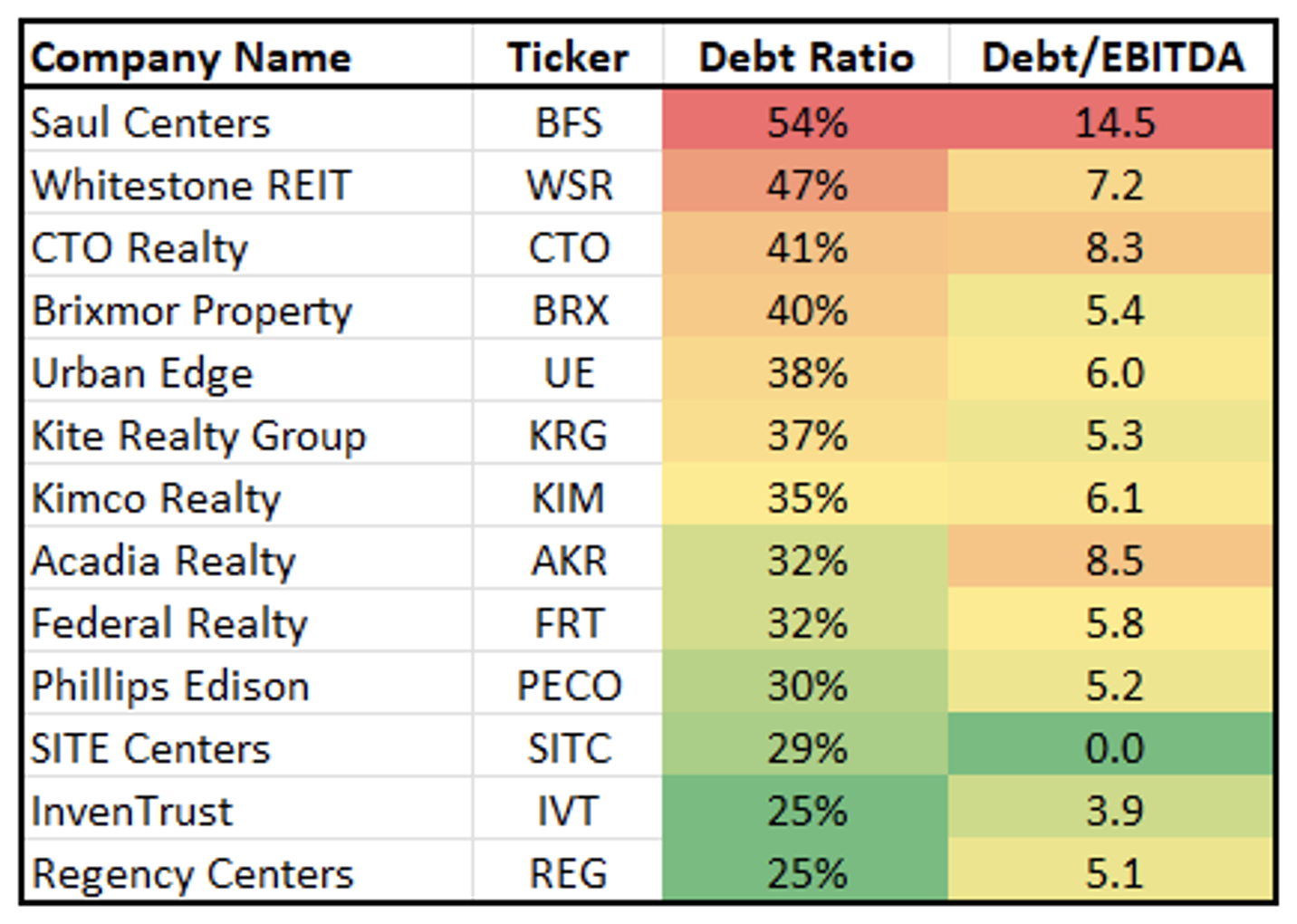

Another shopping center name I like is Brixmor Realty (BRX). A Blackstone (BX) spinoff, it has a strong balance sheet with 5.4 times debt to EBITDA (earnings before interest, taxes, depreciation, and amortization) and one of the best organic growth profiles around with 5% same-store net operating income (“SSNOI”) guidance this year.

Regency Centers and InvenTrust (IVT), however, stand out even brighter with their low leverage, with around 25% debt ratios. Regency has an A3 and A- rating from Moody’s and S&P, respectively, and nearly full capacity on its $1.5 billion credit facility. While InvenTrust has around $480 million in liquidity with a weighted average interest rate of 4%.

Source: Wide Moat Research

Over on the small-cap side, Whitestone REIT (WSR) – which predominantly operates in Phoenix, Arizona, and Texas – has seen a surge in its share price as a result of years of restructuring, debt reduction, and management changes. Plus, activist pressure has attracted buyers like Blackstone and TPG (TPG).

(I wouldn’t be surprised to see Regency go after Whitestone as well.)

Another small-cap REIT worth considering is CTO Realty (CTO), once known as Consolidated-Tomoka Land. It used to own large tracts of land around Daytona Beach, Florida. But over the past decade, it sold off most of that, then recycled much of the sizable proceeds (via the 1031 exchange vehicle) into income‑producing real estate across the U.S.

This shift turned CTO from a lumpy, land‑sale company into a steady cash‑flow REIT specializing in retail and mixed‑use properties in the Sun Belt and other growth‑oriented markets.

Altogether, shopping center REITs are trading at a relatively attractive average 6.7% implied cap rate. That translates to a 15.2% discount to net asset value (“NAV”) despite increased direct capital inflows into the sector.

Looking at the wide spread of opportunities here, I recommend a “pair trade” of owning both Federal Realty and CTO Realty. With current yields of 4.6% and 8.4%, respectively, that averages out to 6.5%.

I’m forecasting these REITs to each return around 20% over the next 12 months.

Source: Wide Moat Research

Regards,

Brad Thomas

Editor, Wide Moat Daily

PS: I’m off today to Myrtle Beach, South Carolina, to speak at Coastal Carolina University, where my youngest daughter is a freshman. Naturally, I’m talking about REITs, and I’m excited to share my lecture with you all later this week.

|