Last week, with the winter storm bearing down on us, I decided to stay with my mom for a few days.

She’s still quite the capable woman, but the meteorologists in Greenville, South Carolina, were forecasting significant ice. Possibly the loss of power, too, for up to a few days.

That’s just not something I wanted to risk.

Holed up with all the bread, water, milk, and snacks we could need, we ended up scanning Netflix for something to watch. That’s how I found Secret Mall Apartment, a documentary about a group of young people who lived rent-free at the Providence Place Mall for four years.

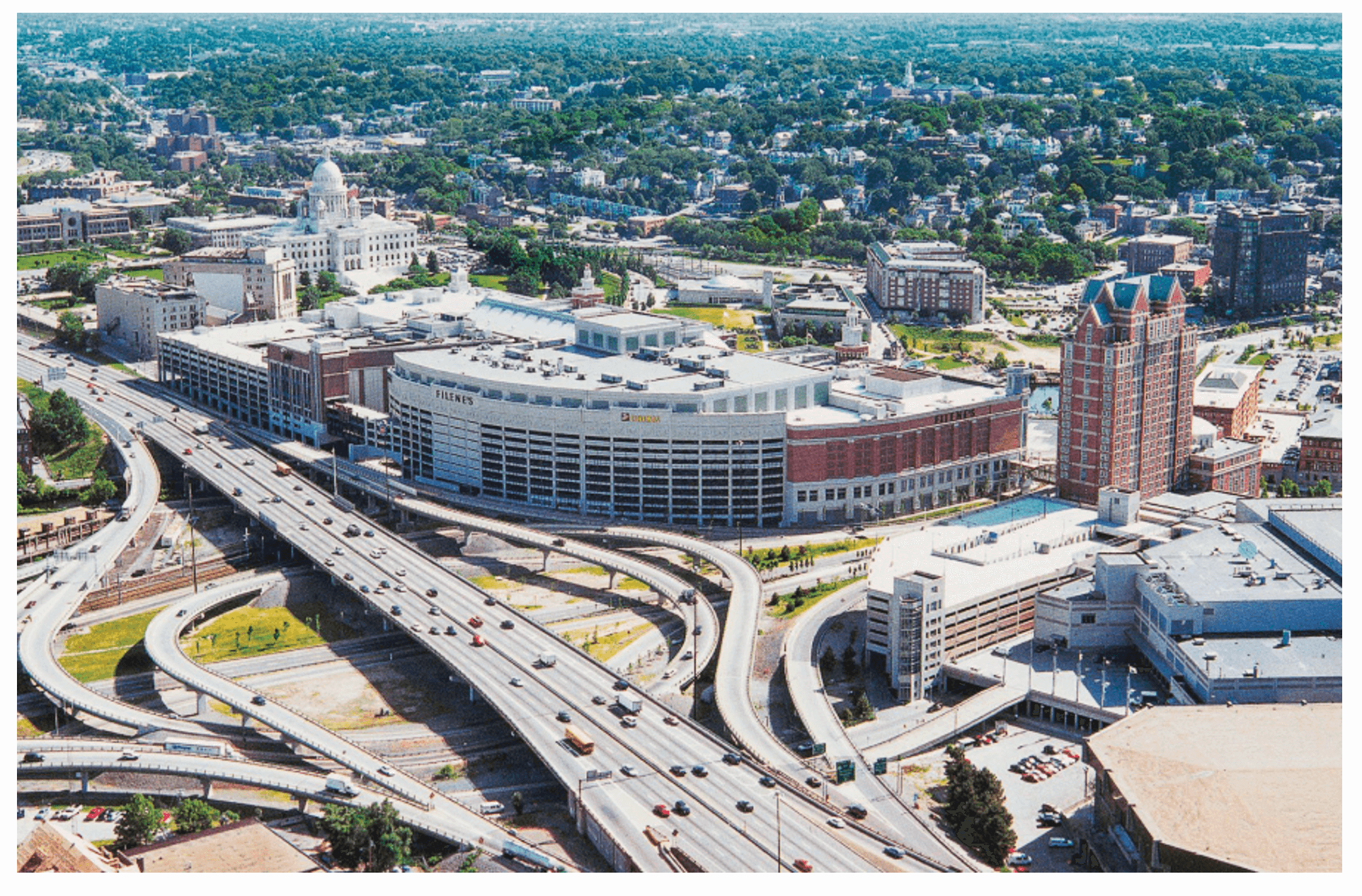

The 1.4 million square-foot Rhode Island retailer in question opened in August 1999. At the time, it was the country’s largest indoor mall, though that wouldn’t be its only claim to fame.

As the story goes, eight artists discovered a hidden 750-square-foot space inside the expansive building and claimed it for themselves. They hauled in furniture, niceties, and even ran electricity, turning it into their home for quite some time.

The squatters were eventually caught, but they mostly got away with it regardless. Only one of them was ever arrested for the long-term trespassing, and they were all invited back to the mall as local celebrities after Netflix aired its documentary last year.

Source: Rhode Island Monthly

And while Providence Place is mostly known for the story of these long-time squatters, I know it for a different reason.

It was a posterchild for the chaos in malls over the last several decades…

The Sorry Saga of Some Malls Since 2000

Providence Place Mall, the site of that now-famous rental theft, was originally developed and owned by General Growth Properties (“GGP”), a real estate investment trust (“REIT”). But it didn’t stay that way for long.

In April 2009, 10 years after the shopping center opened, GGP filed for bankruptcy. The company simply couldn’t keep up with the Great Financial Crisis (“GFC”) and its prolonged, widespread effects.

A group of investors led by Brookfield Asset Management (BAM) provided capital for GGP until August 2018, when BAM acquired it altogether. But even that wasn’t enough to keep it completely solvent.

In late 2024, Centennial Real Estate Management began managing Providence Place after the mall experienced prolonged financial difficulties and entered receivership.

This sad story is hardly uncommon, and we can’t blame it all on the GFC or even the COVID-19 shutdowns. Both were damaging, yes. Yet many malls’ fates were signed and sealed long before those crises.

Truth be told, there were simply too many malls created in the 1990s. The mantra “build it, and they will come” reigned supreme back then, resulting in over 5,000 malls operating across the U.S. by the end of the century.

The situation was never sustainable, made even less so by the rise of e-commerce. Soon enough, mall stores and big-box retailers alike found themselves struggling to keep up as online resources ate away at their margins.

Providence Mall, for instance, started out with three anchor stores: Lord & Taylor, Filene’s, and Nordstrom. But retail isn’t always the easiest business to manage.

So the former closed and was replaced by JCPenney in 2004. And Filene’s was converted to a Macy’s two years later.

The property was still open and operating in the 2010s when the “retail apocalypse” narrative surfaced. But that was partially because the U.S. mall count had dropped to around 4,000 as hundreds of weaker malls fell apart and the consequences of overbuilding were finally felt.

Put simply, there was less competition – though still more than enough to keep weakening the competitors left standing. That’s why, by 2019, the number of malls in the U.S. had declined even further to around 1,500.

And yet I was still bearish on the space back then. There was more consolidation that needed to happen, I said.

Little did I know how immediate and brutal that consolidation was about to become.

The Beginning of a New Mall Era

In August 2019, I warned investors on Seeking Alpha:

I know we’re not telling you anything you haven’t heard before, but we are becoming increasingly skeptical about the fate of malls in smaller markets. Our recent downgrade for Macerich (MAC) and PREIT demonstrates our conservatism on the subject – and the potential for large-scale department store closures over the next few years.

I then wrote a Forbes article to close out the year, titled, “It’s a Sad Day for My Hometown Mall.” It included this assessment (emphasis added):

As a REIT analyst these days, it’s become painstakingly evident that we built way too many retail projects. The future couldn’t hold them all. And so we’re now living in an era in which retail space is being rationalized, especially malls… Our research suggests there will be a wave of department store closures over the next decade.

Source: Forbes

The 2020 shutdowns fast-tracked that prediction. A rash of department store chains – from JCPenney to Neiman Marcus, Lord & Taylor, Sage Stores, and Stein Mart – either closed dozens of locations or filed for bankruptcy altogether.

Thankfully, our team was able to telegraph this to investors in advance of the mall meltdown. We understood the sector was becoming a game of “survival of the fittest.”

And there were survivors. The savviest, strongest mall owners not only made it through each new wave of retail chaos… they ended up thriving.

It’s Tanger’s Time

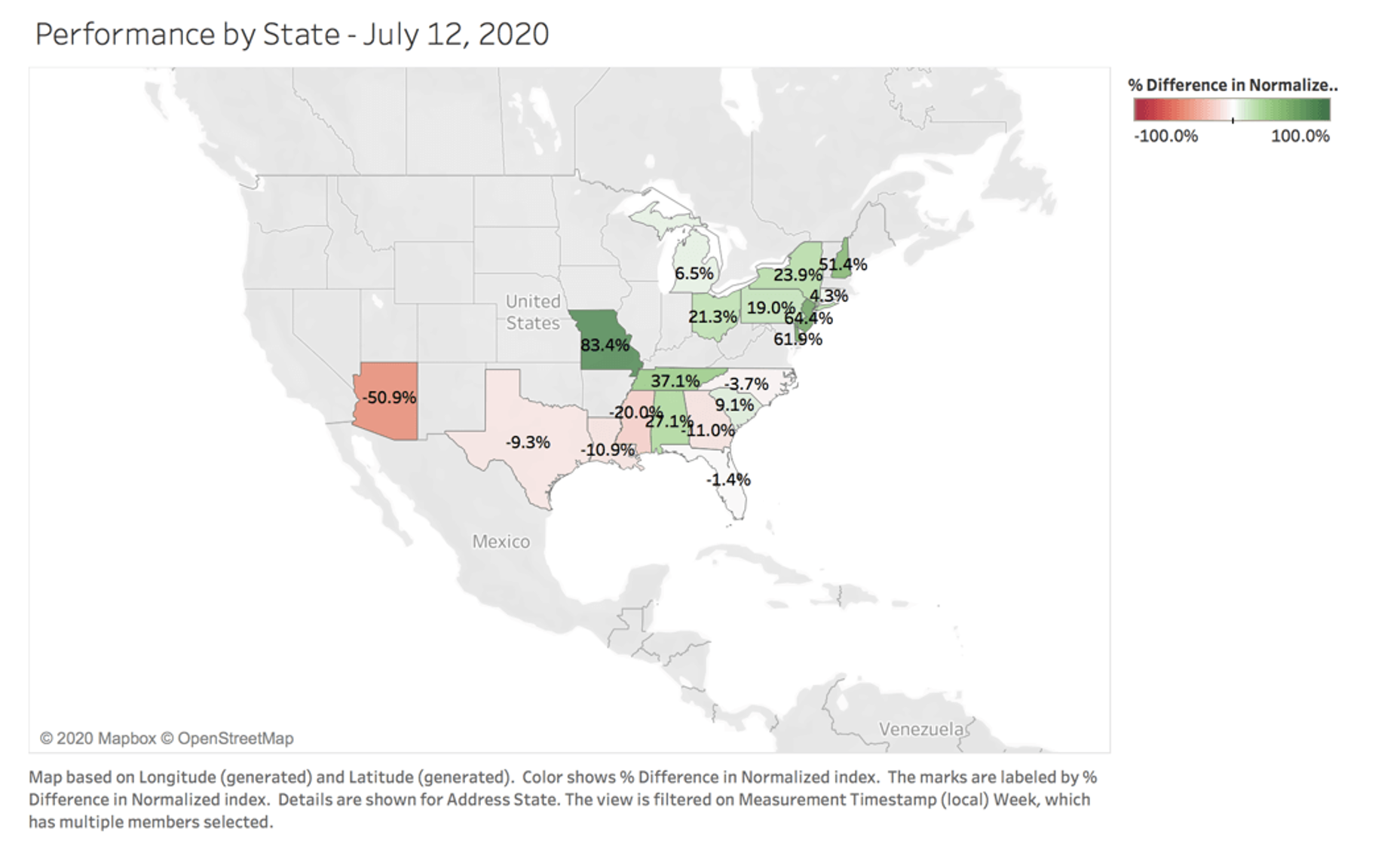

Back at the turn of the decade, my team and I used Orbital Insight technology. It allowed us to analyze billions of cell-phone location data points to understand foot traffic in areas of interest.

We already thought that outlet stores would recover faster than indoor malls, considering their fresh-air appeal. Remember, this was 2020. “Social distancing” was still top of mind. But we wanted to make sure before we made any recommendations.

As I explained in a Seeking Alpha article back then, “We know that indoor malls are generating poor traffic for the most part. But outlets appear to be coming back to life.”

Source: Seeking Alpha

Sure enough, “based on Orbital Insight’s analysis,” we could see that Tanger Factory Outlet’s (SKT) “business model is alive and well. In some instances, there’s even more traffic than before. And while Arizona has been impacted the worst, cell-phone records suggest that rent levels could be in the range of 75% to 80% even there.”

We recommended Tanger at $6.71 back then – and shares have surged a whopping 500% since, while the S&P 500, in comparison, is up just 116%. In fact, the greatly downsized mall REIT sector was a top performer in:

-

2021, up 92%

-

2023, up 29.9%

-

2024, up 27.4%

Investors who avoided dangerous high-yield plays like CBL & Associates (CBL), Washington Prime, and PREIT, and focused on power plays like Tanger and Simon Property Group (SPG), came out ahead.

I don’t think either major retailer has seen the end of its profitable run yet. However, I’m not recommending either right now. Both could use a price pullback first – Tanger to the $30 per share level and Simon down a few dollars as well.

If they do hit a bit of turbulence going forward, they could easily provide safe, growing profits.

In the meantime, there’s another mall REIT I’m interested in, this one up in Canada. I’m currently researching it for my Wide Moat Confidential service, where I recommend small-cap companies with high upside potential. Subscribers to that service should be on the lookout next month.

For now, suffice it to say that the mall industry is far from “dead.” But this isn’t the 1990s either. Investors will need to enter this industry carefully.

Best guess: The strong will continue to get stronger. The weaker players will find their properties transformed into something.

Who knows? Maybe the struggling malls will become multifamily housing units – legal ones, this time.

Regards,

Brad Thomas

Editor, Wide Moat Daily

|