The Supreme Court made its decision on Friday.

Six of the nine justices ruled that President Trump violated the International Emergency Economic Powers Act (“IEEPA”) when he imposed tariffs on most of America’s trading partners last year.

The European Union certainly lit up at the announcement. Both French President Emmanuel Macron and German Chancellor Friedrich Merz were quick to express optimism that their 2025 agreement – involving 15% tariffs on most of their exports and none on most of ours – will be at least lessened going forward.

However, President Trump immediately fired back by promising a 10% global tariff via different legal channels. And the very next day, he bumped that figure up to 15%.

I wouldn’t bet against him on this. Where there’s a will, there’s a way. And Trump certainly has the will. It seems safe to say we’re in for more volatility while all this drama gets sorted out.

So, what is an investor to do in the meantime?

The Year of the Dividend

I read a recent Barron’s article where author Jack Hough called current stock action “the Great Rotation.” He accurately pointed out how “value has beaten growth” this year, “small companies have raced ahead of large, and dividends have shined!”

He’s spot-on about all of that. In fact, the difference in the usually stodgy dividend category is significant.

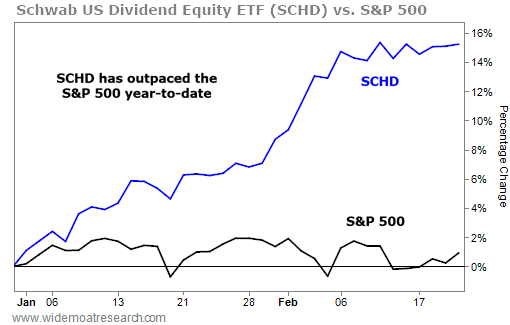

Look no further than the Schwab U.S. Dividend Equity Fund (SCHD). SCHD tracks and mimics the performance of the Dow Jones U.S. Dividend 100 Index. It’s up about 15% year to date.

SCHD includes sectors such as energy, both consumer defensive and cyclical, health care, industrial, technology, financial, communication, and basic materials.

What it does not include is real estate investment trusts, or REITs.

REIT share growth was outright unimpressive in 2024 and most of 2025. Investors neglected real estate stocks due to their interest-rate sensitivity, believing – inaccurately – that the Federal Reserve’s hawkish policy was an automatic death knell for such assets.

Late in 2025 though, I wrote an article titled, “The Best Time in Years to Buy These REITs.” There, I explained how “I really believe this will be remembered as the best time in years to buy high-quality REITs. And that’s because so many great REITs are trading at levels that look ridiculously undervalued.”

Today, I continue to believe that there are very good things up ahead for this investment class. With the world so uncertain about everything from Trump’s tariffs… to whatever is going on with Iran… to artificial intelligence (“AI”) valuations…

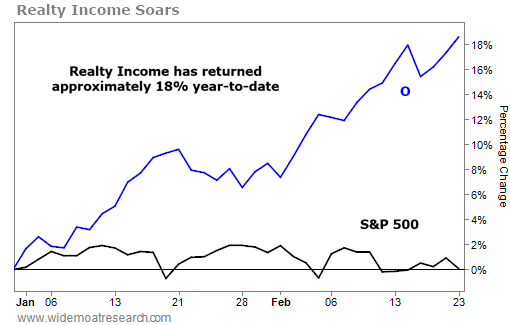

People are seeking out safety more and more. And you don’t get much safer than REITs like Realty Income (O) – up 18% so far this year, outperforming SCHD by several percentage points.

Yet despite that very nice uptick, it remains underappreciated as we wind up the second month of 2026.

A Flight to Quality

Net-lease REITs like Realty Income are often viewed as “flight to quality” investments during periods of economic uncertainty. This makes sense considering how they combine bond-like income stability with real asset backingand long-duration contractual cash flows.

These landlords typically work with single-tenant properties leased out under long-term contracts of typically 10 to 20 years with built-in rent escalators. Plus, they don’t pay taxes, insurance, or maintenance. That’s all on the tenants, allowing net-lease REITs to more easily attain:

- Minimal operational risk

- Highly predictable cash flows

- Low lease rollover risk

- Fairly stable earnings

As a result, like long-duration bonds, they’re known for offering fixed-income streams and stable dividend histories. In the case of companies like Realty Income, they also offer consistent dividend hikes.

So, it only makes sense that many of them carry investment-grade ratings, well-laddered debt maturities, and access to public bond markets to boot.

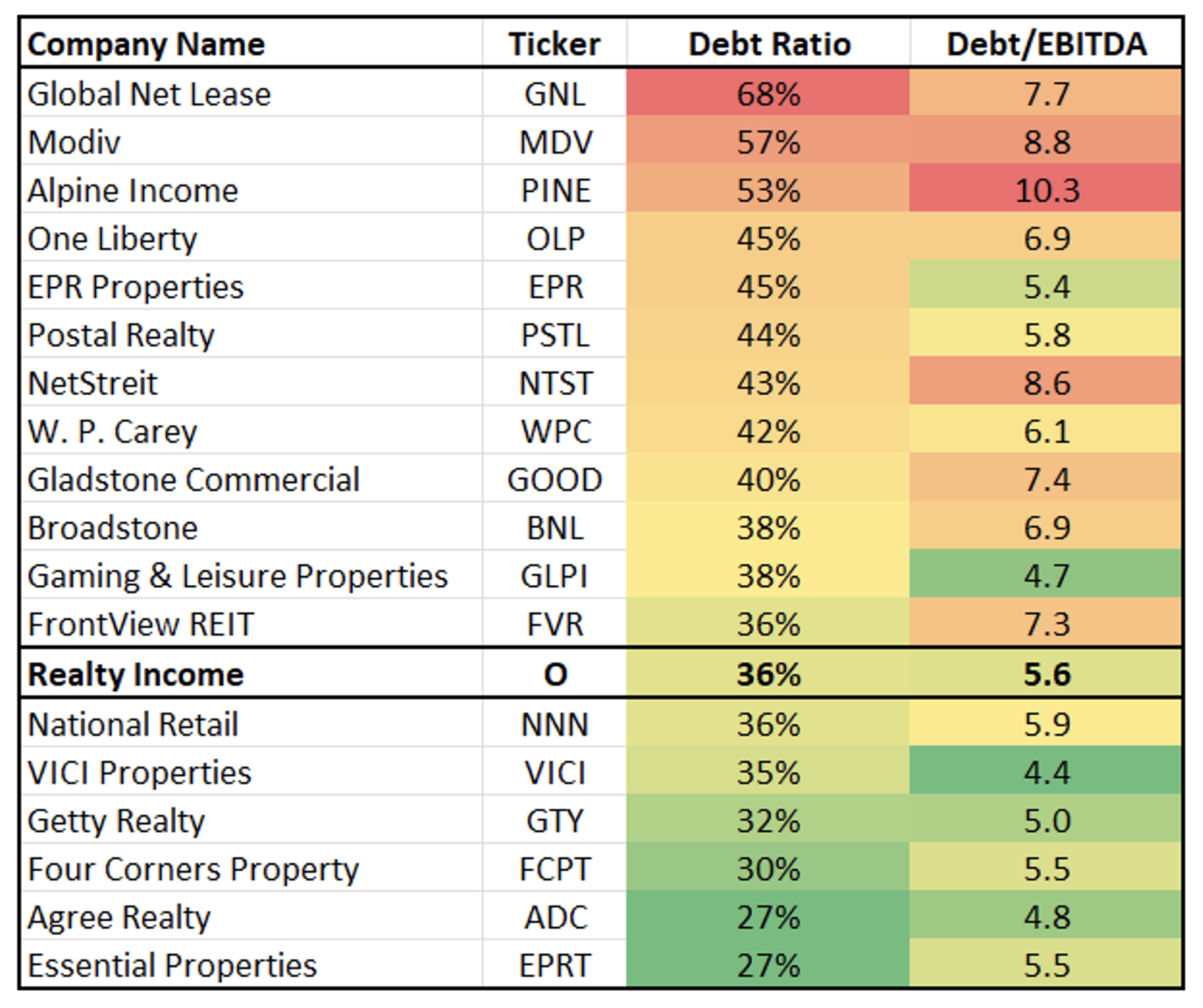

Source: Wide Moat Research

Now, as the chart above shows, not every net-lease REIT is created equal. Some are struggling these days, while others – like Realty Income – keep killing it. That particular landlord has a rock-solid balance sheet with A ratings from S&P and Moody’s, giving it consistent low cost of capital and strong access to debt markets.

As such, it’s well-positioned to snap up deals as they come.

Sure, it’s already one of the world’s largest net-lease owners with over 15,000 properties across every U.S. state. But it has also been snapping up prime European holdings since 2019, and it sees more deals opening up this year.

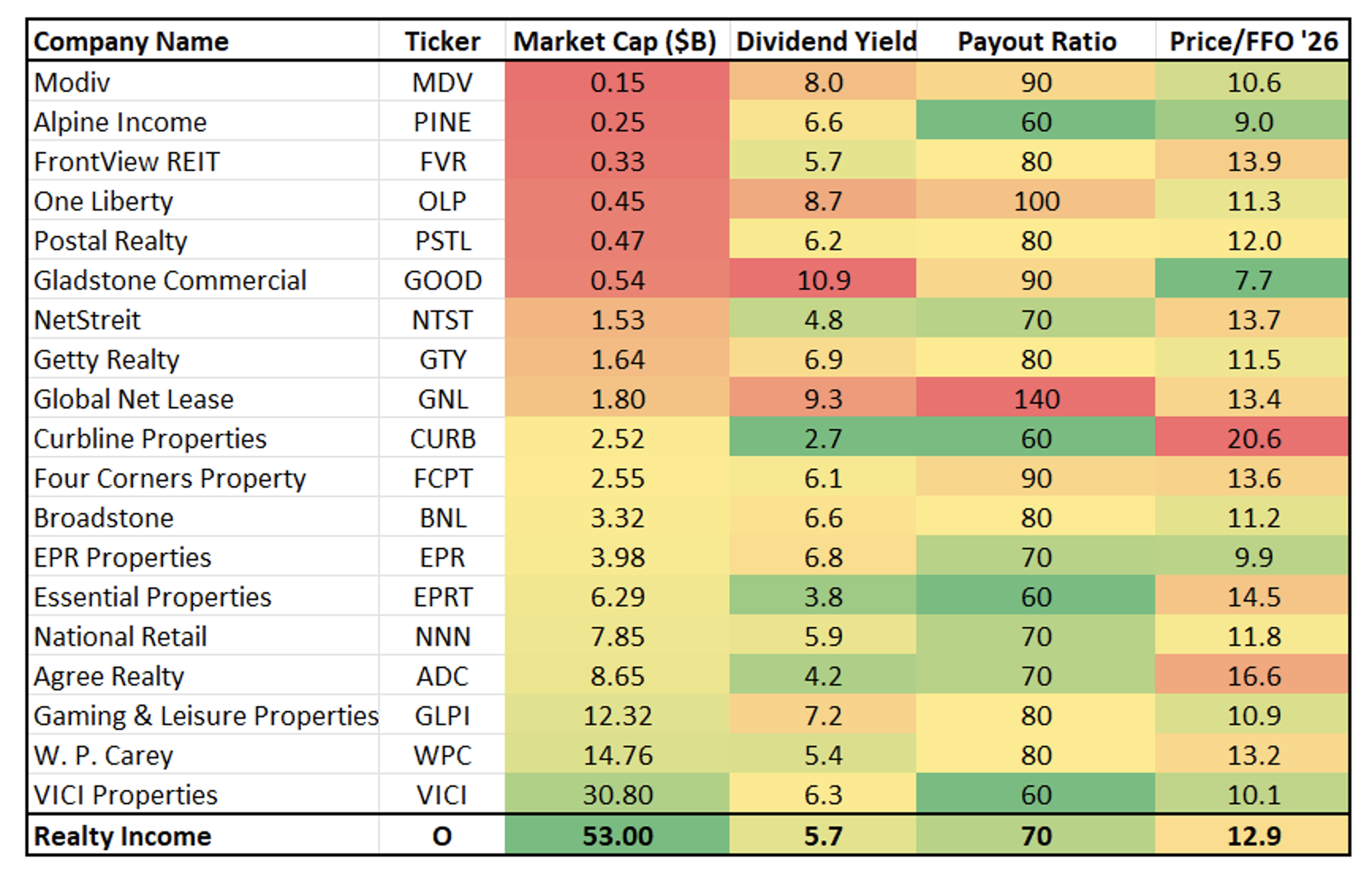

Shares are now trading around $66 with a price to funds from operations (P/FFO) multiple of 12.9 times. Its dividend is well-covered with a 70% payout ratio, and it was yielding a very attractive 5.7% at last check.

Even though shares have returned about 18% YTD, I’m still maintaining a Buy rating. The way I see it, this company is poised for growth no matter what tariff tensions, military conflicts, or AI surprises are headed our way.

Source: Wide Moat Research

Regards,

Brad Thomas

Editor, Wide Moat Daily

P.S. Tomorrow, I plan to provide an update on net-lease REIT VICI Properties (VICI) after Caesars Entertainment (CZR) said its Las Vegas segment showed “a quarterly sequential improvement in occupancy and rate trends.” And check out my REIT rap video on net-lease REITs in general right here.