Editor’s Note: We don’t usually cover digital assets at Wide Moat Research. But with bitcoin hovering near all-time highs, we know it’s a topic of interest for readers. That’s why we’re sharing another essay from Eric Wade, editor of Crypto Capital, published by Stansberry Research, a corporate affiliate. Eric believes bitcoin could reach $1 million per coin in our lifetime. And it all has to do with surprising innovations in the space.

In 1934, the U.S. government changed the way Americans buy houses…

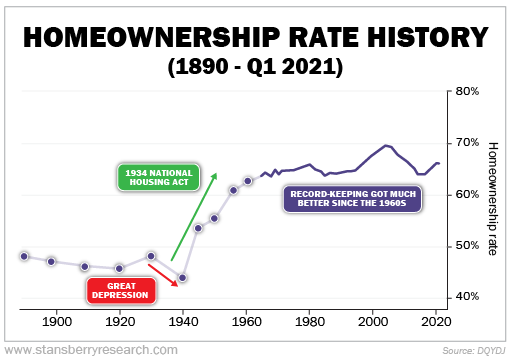

Prior to the 1930s, mortgage loans were largely private affairs, devoid of federal oversight or insurance. The terms of these early loans were exceedingly stringent. Borrowers were typically required to make substantial upfront payments, often as high as 50% of the home’s purchase price. And the remaining balance was typically due within a very short span, usually five to 10 years.

A common structure involved borrowers making interest-only payments for the loan term, culminating in a large lump-sum “balloon payment” of the remaining principal balance at the end. Loans often featured interest rates that could fluctuate, and loan amounts were frequently restricted to 50% of the home’s market value.

The 1934 National Housing Act changed all that by paving the way for the government to create the Federal National Mortgage Association (“FNMA”) in 1938.

FNMA buys and holds loans that meet its strict criteria. So once a home is purchased using a mortgage that conforms to FNMA criteria, the mortgage holder can sell the mortgage to FNMA. FNMA will hold the mortgage and wait as long as 30 years for the payoff.

Selling the “paper” to FNMA means banks and savings and loan firms that issue mortgages can immediately receive their funds and go back into the community and lend again.

After FNMA’s launch, down payments could be as low as 3.5% of the value of the loan. Loans were amortized and lasted 15 to 30 years. Interest rates were fixed.

More people than ever before could get a mortgage. Homeownership went from less than 50% before 1934 to nearly 70% by the late 1960s.

For many Americans, their home is their most valuable asset. The National Association of Realtors says the value of most Americans’ homes exceeds the rest of their financial assets by 10 times.

But in today’s world, we’re often seeing digital asset ownership that could surpass the value of our homes…

A Bitcoin Mortgage

That’s why many people see digital assets like bitcoin, which has grown from virtually free in 2009 to worth more than $100,000 today, as a way to build wealth. Unlike the dollar or other fiat currencies, bitcoin was designed to have a capped supply (of 21 million coins, which is estimated to be reached around the year 2140).

But like homes before the proliferation of mortgages, most crypto purchases required cash up front – until now.

As I’ve shared with Crypto Capital subscribers, we’ve uncovered a platform that lets investors, traders, speculators, and even long-term holders buy bitcoin (and one day, other cryptos) with up to a 30-year mortgage and as little as a 2% down payment.

Today, virtually nobody thinks of buying bitcoin with a 30-year loan. But in time, when bitcoin is held in national and corporate Treasury securities, investors who want to own bitcoin could increasingly turn to these loans.

How big can this be?…

Home mortgages created trillions of dollars of wealth. I believe digital-asset mortgages will do something similar as buyers lock in lower bitcoin prices as the asset continues to hit new all-time highs.

Just consider… the total housing market in the U.S. is worth around $50 trillion. Americans owe nearly $13 trillion on 85.1 million total home mortgages, with $1.69 trillion of that originating in 2024 alone.

Bitcoin is currently worth more than $2 trillion, while the current bitcoin mortgage industry is only worth $427,000. So, there’s a lot of room to grow.

Now, I know this comparison isn’t direct. People live in homes, so they provide more value than just an appreciating asset. But with digital asset ownership growing every year, bitcoin mortgages could appeal to investors.

And just like with a home mortgage, you might own the bitcoin, but you’re not free and clear until you’ve made your last payment. But just like owning a house with a mortgage, all the upside is yours.

This concept might sound far afield, but we’ve never been closer to seeing it…

The GENIUS Act

Last month, Congress passed the GENIUS Act, a landmark law establishing a regulatory framework for dollar-pegged stablecoins, requiring issuers to hold 1-to-1 reserves in liquid assets like U.S. dollars or Treasury bills and disclose reserve compositions monthly.

This legislation, signed by President Trump, aims to legitimize stablecoins as a mainstream payment mechanism. This government backing will help consumers and retailers trust stablecoins. Since they have lower fees and fewer complex processes than traditional banking, stablecoins could parallel the mortgage industry’s post-1938 expansion, where FNMA’s backing enabled broader homeownership.

The GENIUS Act’s clarity is attracting new investors, particularly in underbanked regions. This positions stablecoins as a tool for financial inclusion while reinforcing the U.S. dollar’s global dominance.

Stablecoins like Tether (USDT) and USD Coin (USDC), with a combined market cap exceeding $200 billion, are attracting a new wave of investors to the crypto market by offering stability amid the volatility of assets like bitcoin.

These digital tokens, pegged to fiat currencies, provide a low-risk entry point for retail investors hesitant to navigate crypto’s price swings… much the way low-down-payment mortgages opened homeownership to millions.

But something else exciting is happening… Crypto holdings may soon also help you buy a house.

In June, the director of the Federal Housing Finance Agency ordered Fannie Mae and Freddie Mac to develop proposals to consider crypto holdings as assets in mortgage originations. In other words, cryptos could become an officially recognized piece of folks’ net worth by the organizations backing most of America’s residential mortgages.

In coming years, is it too outlandish to think that mortgages backed by cryptos such as bitcoin might find their way onto investors’ balance sheets?

We’re Already in a Blockchain Rally

Bitcoin surged past $70,000 when Trump was elected to $123,000 last month. But beyond that big crypto leader, the entire blockchain universe is on the rise. Total crypto market capitalization, including other big names like Ethereum (ETH), is up more than 30% year over year.

Blockchain’s decentralized ledger technology enables secure, transparent, and instantaneous transaction processing, which could revolutionize mortgage origination and servicing.

We’re at an exciting convergence… Real-world assets such as real estate, private credit, and even Treasurys are seeing their ownership and value moved onto blockchain. And at the same time, entrepreneurs are creating ways to buy digital assets via payments just like you’d use a mortgage to buy a house or a loan to buy a car.

By “tokenizing” real estate assets, blockchain platforms allow fractional ownership and streamline title transfers, reducing costs and intermediaries. This rally, fueled by growing institutional interest and retail investor enthusiasm, mirrors the transformative impact of the 1934 National Housing Act, which democratized homeownership.

As blockchain adoption accelerates, we could see mortgage markets become more accessible, with smart contracts automating loan agreements and reducing default risks.

And conversely, by mortgaging digital assets, more people could buy low-inflation blue-chip cryptos like bitcoin and pay them off with dollars that are continuously losing value.

Putting all these factors together, you can see that the current blockchain rally isn’t a blip or a bubble. It’s the start of a financial revolution that will drive the values of bitcoin and many other cryptocurrencies.

Regards,

Eric Wade

Editor, Crypto Capital

Editor’s note: As we mentioned above, Eric says that as soon as next week, Trump’s Treasury could stun the market and unveil a $2 trillion financial maneuver… designed to rescue America’s debt markets.

Back in May, Eric attended an elite financial conclave with the likes of the Trump family, JD Vance, and other billionaires and White House insiders. On the agenda? A radical plan to reboot America’s financial system.

Insiders are bracing for this major financial realignment. And, according to Eric, it could trigger a market move like we have never seen – and the biggest, most asymmetric trading opportunity of his career. You can get all the details for yourself right here.

|