Today, President Trump signed an executive order concerning marijuana.

The action reclassifies marijuana from a Schedule I drug to Schedule III. That keeps it illegal under federal law, but it is now considered less harmful, and punishments for possession will be less severe.

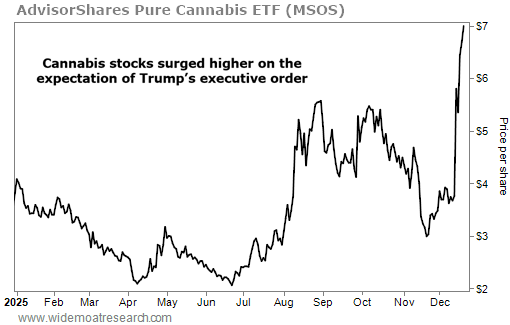

The news of a potential signing sent cannabis stocks soaring, as seen below via the AdvisorShares Pure U.S. Cannabis ETF (MSOS).

Some people will cheer this development. Some people won’t. And I understand both sides. It’s a hotly contested issue everywhere you look.

In the medical community, for instance, some see marijuana as effective treatment for everything from depression to debilitating nausea – including the kind associated with chemotherapy – to chronic obstructive pulmonary disease (“COPD”).

Others link it to aggressive levels of psychosis, cannabinoid hyperemesis syndrome (which produces severe nausea), and breathing issues.

In social circles, some groups view it as perfectly acceptable recreation. Others see it as a drain on civilization.

I guess that Trump’s order takes a middle stance on the issue. But it will be a drastic game-changer nonetheless, impacting marijuana-related taxation, medical access, real estate, and federal enforcement.

Let’s consider a few implications…

A Marijuana Tax Deduction?

From a tax perspective, one of the immediate benefits of rescheduling is relief from IRS Code 280E, which prevents businesses handling Schedule I or II substances from deducting standard operating expenses. Simply put, the move to Schedule III reduces the federal tax burden for operators and makes them more feasible.

This would obviously mean more profit potential for cannabis and cannabis-related businesses, which have been struggling for years under an onslaught of competition. Frankly, as states keep legalizing the substance, the market keeps getting more saturated.

That has caused a lot of problems for real estate investment trusts (“REITs”) that cater to the field. So, I understand why the promise of a more pro-marijuana executive order has caused people to rethink these investments.

Personally, I would still advise caution, though. The way I see it, most marijuana REITs aren’t out of the weeds just yet.

The Rise of the Marijuana REITs

The first mover in the cannabis REIT sector was Innovative Industrial Properties (IIPR). Founded in June 2016, it went public on the New York Stock Exchange (“NYSE”) by that December amid a lot of fanfare. And it’s still the only cannabis REIT on the NYSE today.

IIPR’s original business model centered around buying up land and buildings from cash-strapped marijuana operators, then renting them right back in sale-leaseback transactions. This gave it long-term tenants, while the operators got an instant influx of cash from a reliable source.

This aspect is a very big deal considering how – regardless of whether it’s classified as Schedule I, II, or III – cannabis isn’t something traditional banks want to touch, since they have to abide by federal regulations.

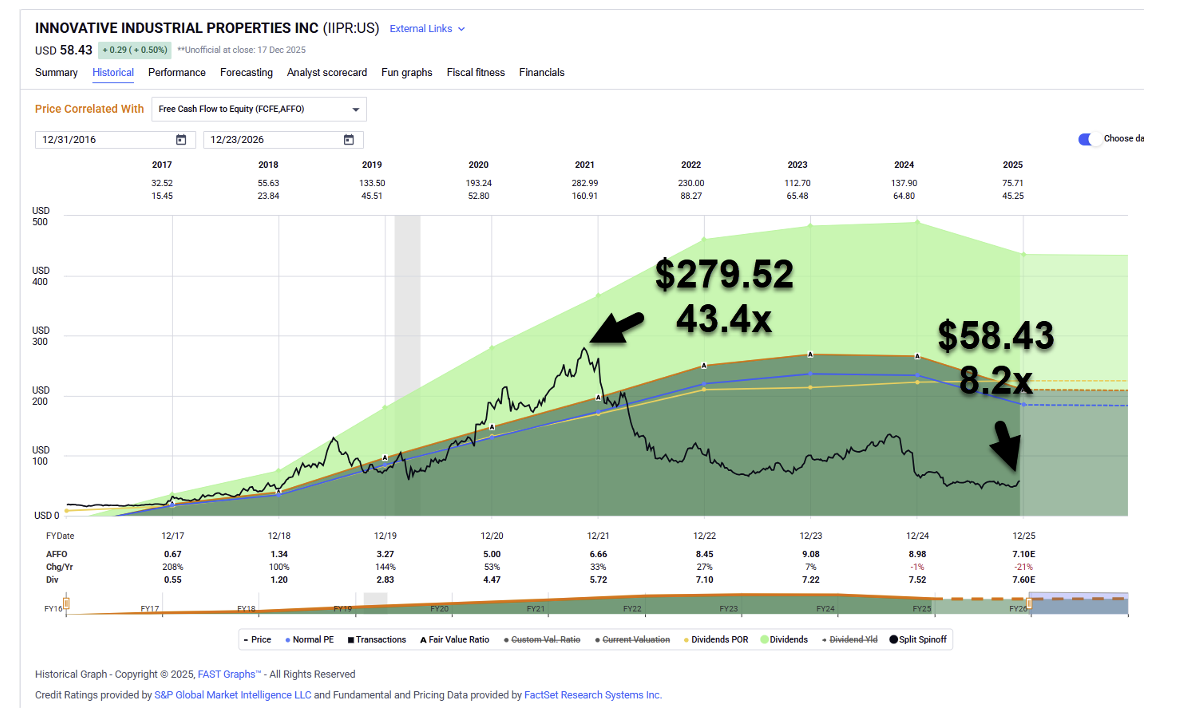

As you can see below, the company grew like a tech stock from 2017 through 2019, growing adjusted funds from operations (“AFFO”) by an average of 150% per year. Then, in 2021, shares hit an all-time high of $279.52 with a multiple of 43.4 times.

Many people thought it would just keep climbing from there.

Source: FAST Graphs

But as the FAST Graphs chart also shows, it didn’t live up to that hype. Shares have since tanked to $58.43, with a price-to-AFFO (P/AFFO) multiple of 8.2 times.

Far from the growth stock it used to be, IIPR actually generated negative 1% growth in 2024 and negative 2% so far in 2025. That might be why it recently began venturing into the life-science sector, with a $270 million structured investment in private REIT IQHQ.

It should be pointed out that IIPR’s co-founder and executive chairman, Alan Gold, also founded IQHQ. He did step down from the latter last December, but there’s still clear potential for conflicts of interest. Plus, we now have to wonder whether IIPR is really committed to cannabis at all.

Has it decided the sector it pioneered wasn’t worth the effort after all? We shall have to wait and see.

The Rest of the Motley Marijuana REIT Crew

Even if IIPR is souring on marijuana, that still leaves us with NewLake Capital Partners (NLCP). Founded in 2018, it also acquires properties it then leases to leading operators in the state-licensed cannabis industry.

However, unlike IIPR, it trades over the counter instead of on a major exchange. And while its earnings grew by 48% in 2022, it has been flat this entire year, with a negative 7% consensus growth forecast for 2026.

Source: FAST Graphs

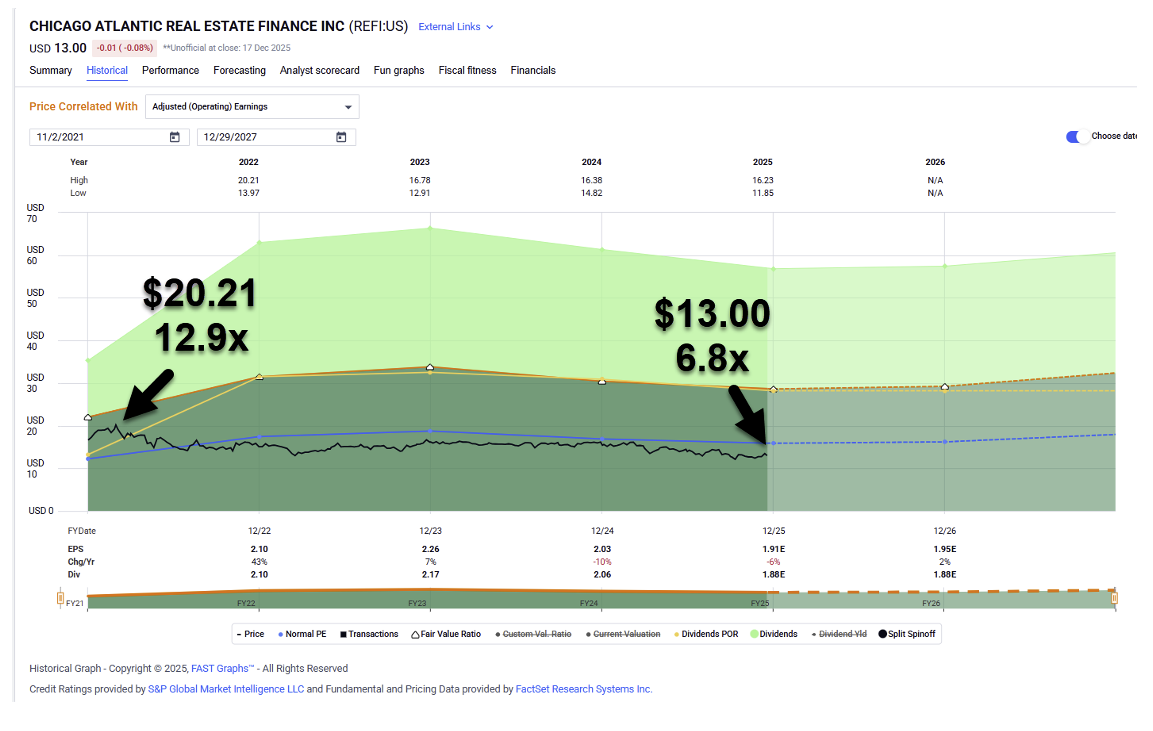

Chicago Atlantic Real Estate Finance (REFI), meanwhile, is a mortgage REIT (“mREIT”) that began trading in December 2021 on the Nasdaq. This means it doesn’t own any physical real estate. Instead, it makes property loans to tenants licensed in their respective states.

For mortgage REITs, we use the standard stock-evaluation tool of price to earnings (P/E) instead of P/AFFO. As you can see below, REFI traded as high as $20.21 with a P/E of 12.9 times in 2021… and now trades at $13 and 6.8 times, respectively.

Source: FAST Graphs

Even worse is Advanced Flower Capital (AFCG), another mREIT based in West Palm Beach. It listed in July 2020 on the Nasdaq and has been a trainwreck ever since as far as performance.

Shares traded as high as $17.12 with a P/E of 20.7 times. But they now sit in “cigar butt” territory with a P/E of 4.3 times.

Source: FAST Graphs

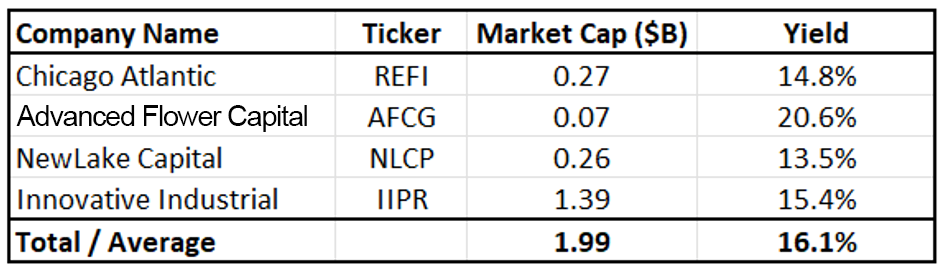

All in all, it’s been a bumpy ride the past few years with these stocks, as the table below will show.

Source: Wide Moat Research, Public Data

I’m Looking Elsewhere for Great Value

There has clearly been a lot of value destruction within the cannabis REIT sector over the past few years. And I’m not confident its outlook will improve much going forward, even with President Trump’s expected reclassification.

That executive order will certainly help its customers improve their margins, putting them in better standing to pay their rent and loans. And I don’t think this will be the last bit of good news for the industry. It’s just a matter of time before additional reforms are addressed, including banking and insurance…

In which case, marijuana operators won’t have to run to REITs for money anymore. They’ll have plenty of other options to work with.

I know these real estate stocks look very cheap right now, with average yields of 16.1%. However, that doesn’t make them bargains. I wouldn’t recommend owning them unless you’re taking small, speculative positions.

Source: Wide Moat Research

And if you feel you simply must dip a toe into the cannabis REIT sector, the strongest one is likely NLCP. Its solid financial performance and strong management team put it ahead of its competitors in the space. Plus, its dividend coverage of 82% is within its target range.

The company also said on its recent earnings call that it was open to diversifying beyond cannabis if attractive opportunities arise. Plus, it maintains one of the strongest balance sheets in the sector, with $432 million in gross real estate assets. And it boasts a conservative debt profile of just 1.6% debt to total gross assets… and no maturities until May 2027.

Overall, though, while this latest move by President Trump might mean we’re right on the cusp of a major turnaround for cannabis companies, I’m not doing jumping jacks to become a landlord.

My advice is to focus on REIT sectors that offer more sustainable growth backed by some of the strongest tenants on the planet… and operate in sectors without such thorny regulatory headwinds.

With that in mind, I you might find this interesting. It’s a special presentation I recently put together detailing how the Trump administration is going all-in to support one corner of the commercial real estate market. If I’m right, it could set up a handful of REITs to climb much higher in the years ahead. You can access it right here.

Regards,

Brad Thomas

Editor, Wide Moat Daily

|