October 2025 has been a busy month so far, and we’re not even quite halfway through it.

For one thing, there’s more trade tension and talks (or talks about talks) between the U.S. and China. That has led to some noticeable market volatility, as Nick Ward shared with Wide Moat Letter readers yesterday.

Though President Trump took to Truth Social the other day to tell everyone “not to worry about China.” “It will all be fine!”

Judging by yesterday’s market gains, that reassurance seemed to have worked.

Amazon (AMZN), for its part, doesn’t seem worried one bit. Despite an enormous reliance on China, with around 70% of goods sold on its website produced there, it announced that it will be hiring 250,000 seasonal workers for the third year in a row.

Meanwhile, artificial intelligence spending continues to skyrocket. We now know that OpenAI and Broadcom are partnering to produce AI processors. And Oracle and Meta are hashing out a $20 billion cloud computing deal.

(Read my data-center article from last week here.)

With all that big news going on, today’s topic might be a surprising one – cold storage. But that doesn’t mean there’s not real money to be made in this under-the-radar part of the global food chain.

Packaged meat, frozen dinners, dairy products, and even fruits and vegetables: The vast majority of it doesn’t go right from farm to table. Instead, there’s a supply chain that involves a very important midway stop in the form of cold-storage facilities.

These buildings are often warehouse-sized with specific temperature-controlled features that keep food from spoiling too quickly. And they’re full of foods from a range of customers, including big-name brands like Kraft, Heinz, Perdue Farms, and General Mills.

Although there are many small and smaller companies that own and operate cold-storage facilities, they’re not always investable – unlike Americold (COLD) and Lineage (LINE).

These two real estate investment trusts (“REITs”) are mission-critical warehouse owners that are hard to ignore once you know they exist.

Opening the Door to Americold and Lineage

Americold is currently trading at $23.45 per share, down 40% this year and the lowest price since its 2018 IPO. That’s the first thing you need to know.

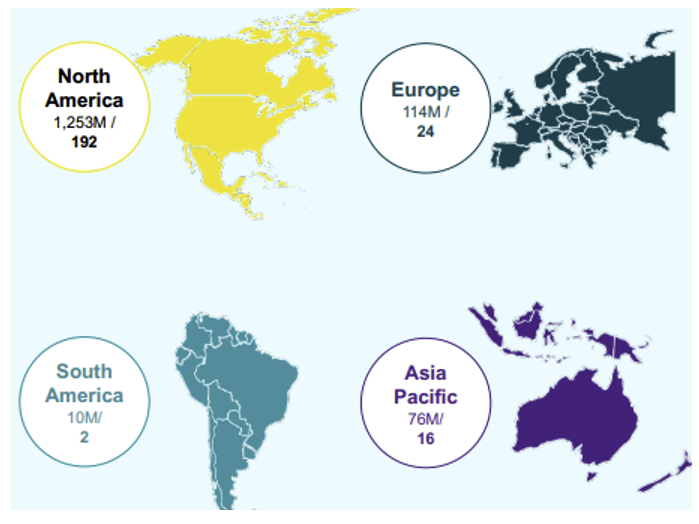

As shown below, Americold owns 237 warehouses with a 20% market share. The company has over 3,000 customers that serve North America, Europe, Asia Pacific, and South America.

Source: Americold Investor Relations

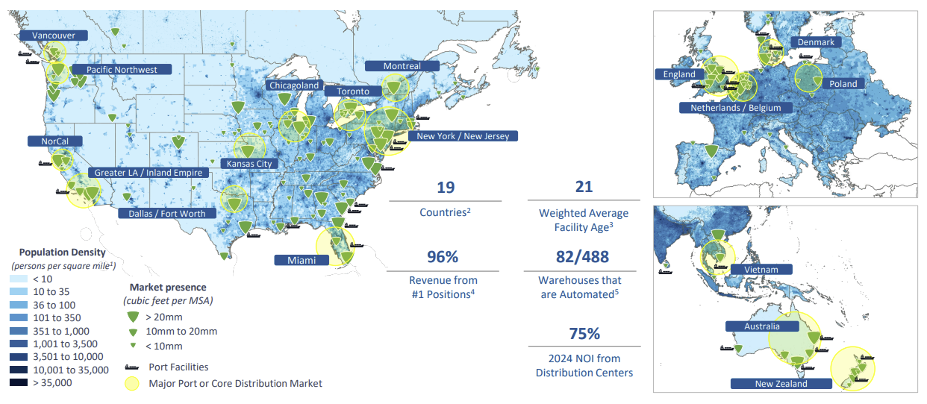

Then there’s Lineage, which is the largest cold-storage REIT with its 488 warehouses in 19 countries. It single-handedly controls about one third of the North American market.

Source: Lineage Investor Relations

Lineage has over 13,000 customers that occupy over 86 million square feet. Yet it’s off by 30% this year, taking it down to around half its IPO price of $78 from back in July 2024.

So what’s going on?

It wasn’t that long ago that cold-storage companies were beloved by REIT investors. During the 2020 shutdowns, Americans stayed at home and prepared their own meals, meaning there was increased activity at grocery stores… and thereby increased need for temporary food storage.

Americold, for its part, peaked in April 2021 at $40 per share. But that’s three times its current share price.

Investors just don’t see their value the same way in October 2025 for a variety of reasons.

First off, we all know demand in this area isn’t as strong as it was during COVID-19. People have other places to go than just the grocery store now. That’s driven downward sentiment.

On Americold’s second-quarter 2025 earnings call, CEO George F. Chappelle said:

Based on our conversations with customers, we expect these headwinds [i.e. tariffs, inflation, and government benefit reductions] will likely continue into the second half of the year as they remain hesitant to build inventory in an uncertain demand environment. With inventory levels low across the supply chain, we are also seeing customers taking the opportunity to leverage available capacity in their own infrastructure rather than utilizing third-party storage provide.”

As a result, Americold is “taking a more conservative view of the market for the second half of the year.” This means it will be “removing the traditional seasonal inventory build that we had been forecasting” as it “expects occupancy levels to remain pressured for the balance of the year.”

With that said, there are a few reasons why this space could be interesting for real estate investors…

The Time Is Ripe for Cold-Storage REITs

I recently evaluated America’s two farming REITs, noting how they’re in completely different situations despite working in the same field. That’s the difference management and corporate structure can make.

However, even the best leaders can find themselves at a temporary disadvantage in challenging environments. And that’s precisely what we’re seeing in the cold-storage space right now.

Lineage is seeing the same trends as Americold, with its CEO, Gregory Lehmkuhl, explaining how:

Late in the second quarter, when inventories historically started to decline, we saw muted seasonality in occupancy. This trend continued into the third quarter, and we’ve only recently seen a positive inflection in their inventories.

This delayed occupancy improvement, combined with persistently high freight prices, tariff uncertainty, and elevated customer inventory carrying costs, drove our decision to lower outlook for the second half of the year.

It’s clear then that neither cold-storage facility has high expectations for 2025. Then again, 2025 is coming to a slow but steady close. And while both REITs are unloved right now, they’re very cheap, and vital to the global food supply. And they both have solid balance sheets as well.

At the end of the second quarter of 2025, Americold had total net debt of $3.9 billion. Its total liquidity, meanwhile, was approximately $937 million. And net debt to pro forma core earnings before interest, taxes, depreciation, and amortization ("EBITDA") was approximately 6.3 times.

Lineage, for its part, ended the quarter with net debt of $7.4 billion and total liquidity of $1.5 billion. Its leverage ratio was 5.7 times.

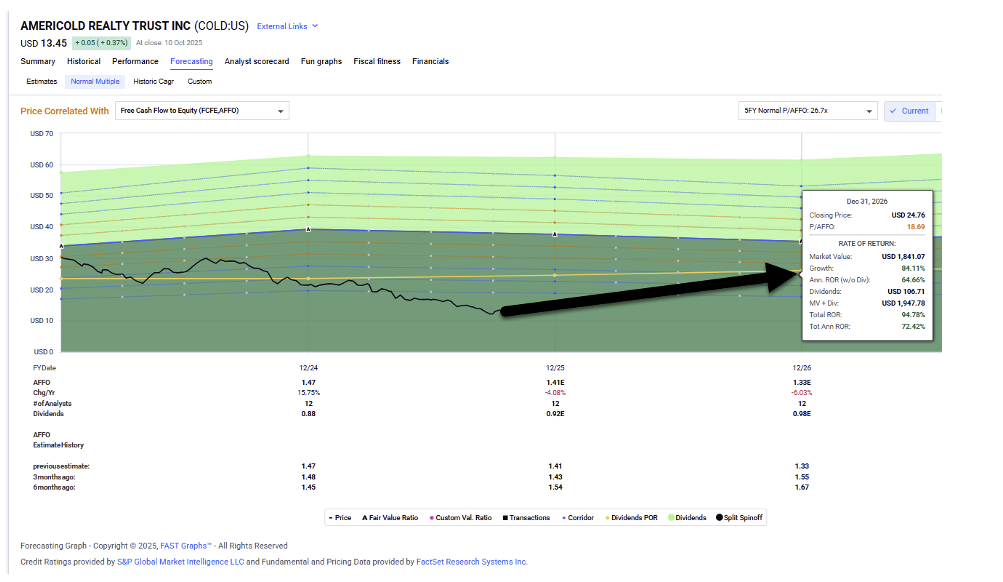

Moreover, shares of Americold are now trading at 9.5 times adjusted funds from operations (“AFFO”) compared with the normal (historical) valuation of 25.7 times. And that deserves consideration even though growth expectations are negative for the year… and negative for 2026 as well. Analysts don’t get more bullish until 2027, where consensus growth goes back to a safer 7%.

Source: Fast Graphs

But Americold’s payout ratio is 65% – lower than it was in 2021, where growth was down 11% and the REIT traded at around 24 times.

Look, I’m not expecting Americold to return to normal valuation levels any time soon. However, even a reset back to 19 times would generate annual returns of 70% or more… all while you get paid a juicy 6.8% dividend yield.

Source: FAST Graphs

Lineage is cheap as well, though it’s trading a bit higher than Americold at 12.1 times. Its dividend yield is 5.7% with a payout ratio of 65%, and analysts expect negative 1% growth this year and flat growth in 2026.

Source: Fast Graphs

So it’s a similar story here and could provide very nice returns going forward.

Then again, the deep-value play in the cold-storage sector is without a doubt Americold. I like it the best, given its higher yield and potential for superior total returns.

Regards,

Brad Thomas

Editor, Wide Moat Daily

|