Americans have a lot of debt…

We learned just this past quarter that:

-

U.S. mortgage debt increased to $12.94 trillion.

-

Credit-card debt hit $1.21 trillion.

-

Car loans topped $1.66 trillion.

-

Student loan debt reached $1.64 trillion, with 10% of recipients being over 90 days delinquent.

According to the Federal Reserve Bank of New York, U.S. household debt grew by $185 billion last quarter to an eye-popping $18.38 trillion.

Then again, nominal debt levels are only one piece of the equation. The other piece, of course, is income used to service that debt.

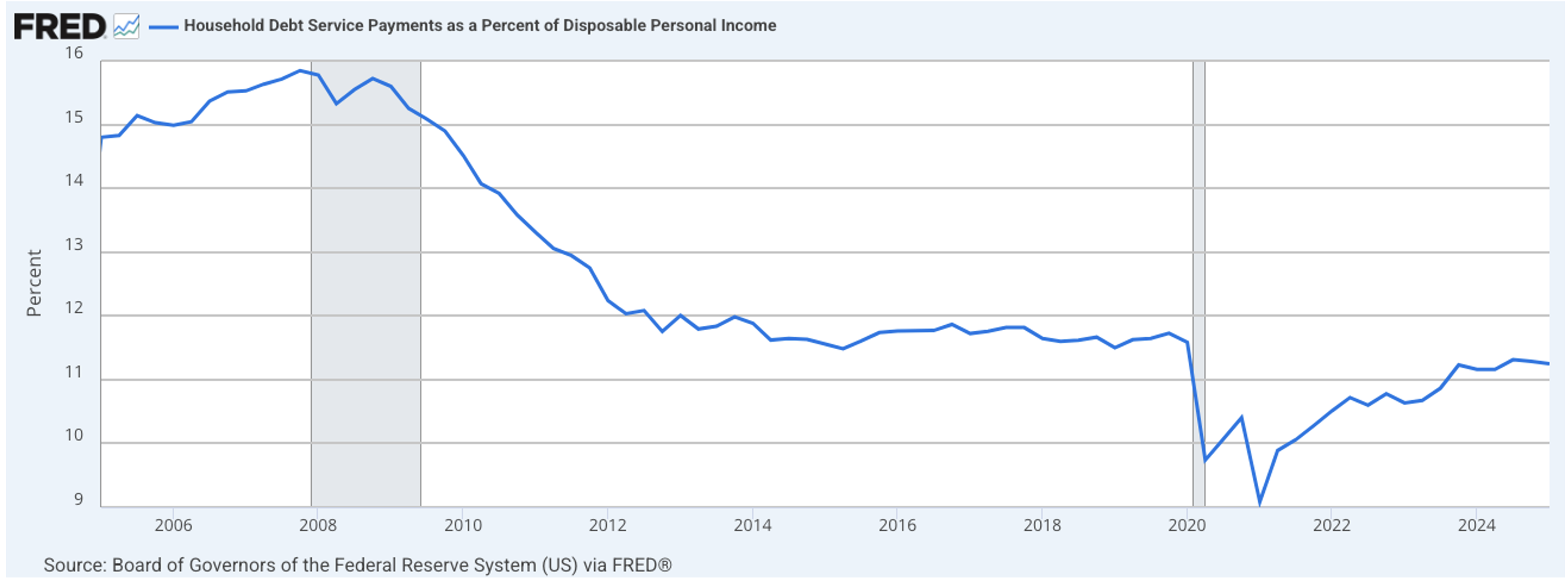

According to the Federal Reserve, household debt service payments as a percent of disposable personal income stand at around 11.2% today. That has risen from the COVID-19 era (you can thank stimulus checks and loan pauses/forgiveness programs for that low reading). But it’s still below pre-COVID levels. And it’s a far cry from the levels we saw in the run-up to the housing crisis. Back then, that metric reached nearly 16%, the highest level in 40 years.

Those really were strange times. Back before 2008, low-credit-score holders were known as subprime borrowers. The average credit score to qualify for such a loan was 580. But believe it or not, many mortgages required no income documentation. If you wanted a loan, you were going to get one, few questions asked.

Today, income verification is a must for even non-prime mortgages – a category between prime and subprime, with an average credit score of 660. And consumers in this category do have reputable resources to turn to today.

This includes the two companies I’m covering today.

OneMain Financial

OneMain Financial (OMF) is an omnichannel consumer finance lender that serves over 19 million non-prime customers. Its nationwide network consists of about 1,300 branches and six central operations centers across 47 states.

That means it’s the seventh-largest network of finance companies in the U.S., including traditional banks.

OneMain’s core lending platform services more than 3.5 million customers, up 11% from a year ago. They’re able to choose from a diverse product suite of unsecured and secured loans. Credit cards, too, all offered under the name Brightway, with more than 920,000 customers so far.

The company also deals in auto financing, with over $2.6 billion in receivables and 132,000 loans. This combination of local relationships with central servicing, underwriting, and similar services allows OneMain to maintain close contact with customers while also supporting their digital preferences.

Its customers’ credit scores average around 641 for unsecured loans and 622 for auto loans. And its interest rates range from 28% for the former category and 22% for the latter.

Delinquency rates are down by 29 basis points (bps) year over year, and the 30-day delinquency rate was 5.07%. Consumer loan charge-offs also fell 64 bps to 7.2% in the latest quarter.

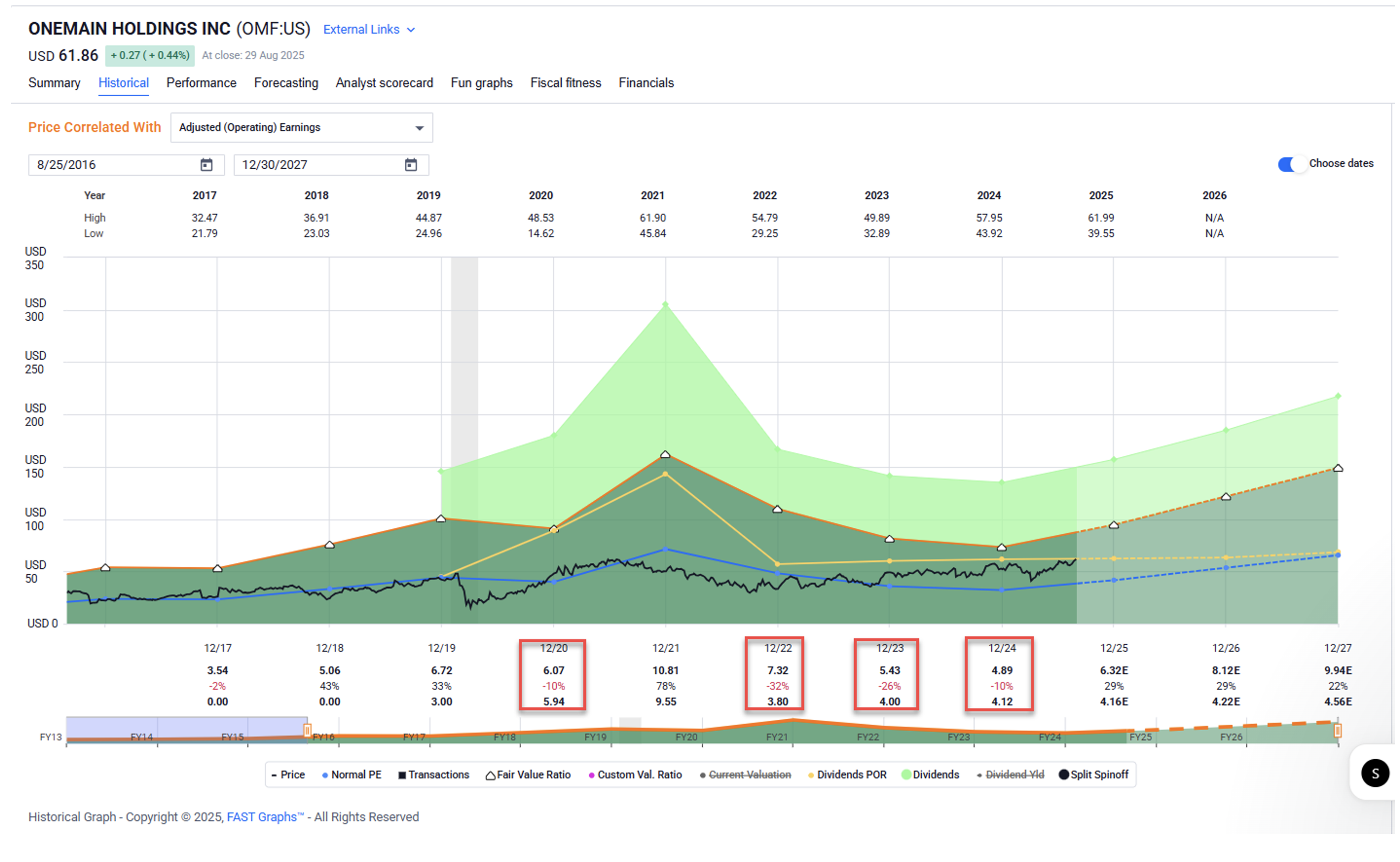

As shown in the FAST Graphs below, OneMain’s earnings history has been rather lumpy in recent years. In fact, it experienced negative earnings per share in 2020 and 2022 through 2024.

However, analysts are bullish on its growth going forward, expecting a 29% increase in both 2025 and 2026.

Source: FAST Graphs

Shares are trading at $61.86 with a price-to-earnings (P/E) ratio of 10.6 times, in line with their normal value. And its dividend yield is a healthy 6.7%.

As a value investor, I would wait on a pullback, possibly establishing a position closer to $50. But it’s still definitely a stock to watch in my book.

FirstCash Holdings

You might not think of a pawnbroker as “reputable,” but that’s exactly the case with FirstCash Holdings (FCFS).

With more than 3,300 retail locations, it’s the largest pawn store operator in both the U.S. and Mexico. Basically, the company has been able to scale its business over three decades by rolling up smaller rivals.

FirstCash is also the largest pawnbroker in the U.K. after last month. It just finalized its acquisition of H&T Group there with its 286 locations… setting the stage for further European growth.

As FCFS management pointed out, this latest move is “meaningfully accretive to earnings” as well.

In the current environment of high interest rates, banks have pulled back on riskier customers. So FirstCash is well-positioned to serve consumers with lower credit scores.

CEO Rick Wessel pointed out in a recent Barron’s interview how:

There is no doubt that we are seeing new customers, given our unique value proposition of offering smaller-dollar loans in quick, hassle-free transactions that take 15 minutes or less. All loans are non-recourse and don’t involve credit checks or credit reporting.

FirstCash’s business model is one of the oldest forms of banking. The customer can either repay the loan with high interest to reclaim the item or forfeit it, allowing FirstCash to resell it for a handsome profit.

In the second quarter of 2025, its same-store pawn loan balances increased by 13% year over year in the U.S. and Latin America. That strong demand helped boost its revenue to $831 million.

Plus, adjusted earnings per share increased by 31% to $1.79 per share. And the company raised its dividend by 11%, to $0.42 per share.

As shown in the FAST Graphs below, FirstCash has demonstrated steady capital markets discipline over various market cycles. The COVID-19 pandemic era was no exception, allowing FCFS to maintain its dividend.

Since 2016, the company has boosted its dividend by an annual average of 12%.

Source: FAST Graphs

Shares are now trading at $147.27 with a P/E multiple of 19.3 times compared with their normal 19.6 times. Its dividend yield is 1.1%, and analysts expect it to grow 22% next year and 27% in 2027.

Our year-end 2026 price target is $184, which would translate into a 20% annualized total return forecast.

Regards,

Brad Thomas

Editor, Wide Moat Daily

P.S. On my YouTube channel this week, I will be discussing a “real time” millionaire next door that I met when I was a real estate developer. You don’t want to miss this episode… or the ones I’m developing right now.

Make sure to officially subscribe to get weekly notifications.

|