It’s easy to make life more complicated than it needs to be…

For instance, Valentine’s Day is approaching. Roses, some quality time, and/or washing the dishes might be all your loved one wants. In which case, that $400 pair of earrings you’ve been eyeing is a waste of your time, money, and affection.

(Then again, you know your loved one better than I do. So, act accordingly.)

As a general rule, keeping it simple wins out. That’s as true for investments as it is for life.

I’ve been a Wall Street writer for a long time now. I’ve seen fads, trends, and flashy companies with complicated business models come and go. Some of them make it and deliver wonderful returns to investors.

But, more often than not, it’s the simple, deceptively boring, quiet compounders that create real wealth over the long run.

Remember, when in doubt, KISS (keep it simple, stupid).

One of the Best KISS Compounders

One of the best KISS compounders on the planet is Hershey (HSY). Hershey does not have a complicated business. It makes sweet and salty snacks. Then, it sells those snacks for more than the cost to make them.

That’s it.

The company’s products include Reese’s, Kit Kat, Twizzlers, and Kisses. The company also has several salty snack brands like Dot’s Pretzels, Pirate’s Booty, and Skinny Pop Popcorn. These snacks are hard to resist, even during inflationary times.

During downturns, people may forgo major purchases but still buy candy. If anything, it seems like an understandable consolation when saying no to larger luxuries.

As such, Hershey has historically performed well in recessions. That’s one reason it has achieved Dividend King status with 50-plus consecutive years of dividend increases.

Hershey really does have the textbook “keep it simple” business model, complete with fast inventory turnover, low obsolescence, and, most importantly, reliable free cash flow year after year.

And its margins are among the best in the packaged foods sector, driven by its:

-

Massive scale advantage, with around 45% share of the U.S. chocolate market

-

Efficient manufacturing through large plants that never stop running

-

Tight stock keeping unit (“SKU”) control, which avoids complexity

Although Hershey is considered a consumer staple, it still grows earnings in the mid-single digits. By reinvesting in the brands it understands, this chocolate king generates highly predictable, repeatable high returns on invested capital (“ROIC”).

Consider how Hershey tends to grow its revenue 5% per year with strong margins. If it then buys back 1% to 2% of those shares annually while raising its dividend 6% to 10%, earnings per share (“EPS”) might grow 7% to 9% per year.

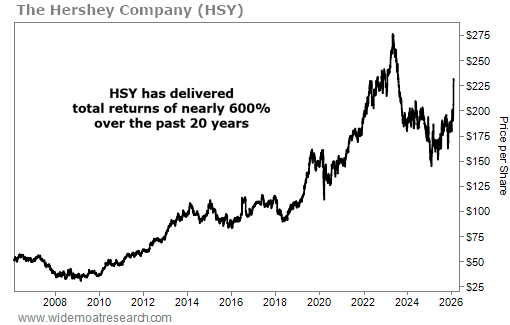

It’s reliability like that which has helped HSY deliver close to 600% total returns over the past 20 years.

That’s what I call “boring magic,” and it’s why we recommended the company to readers of The Wide Moat Letter in January 2025. It’s recording a 41% return for us, more than twice what the S&P 500 put up over that period.

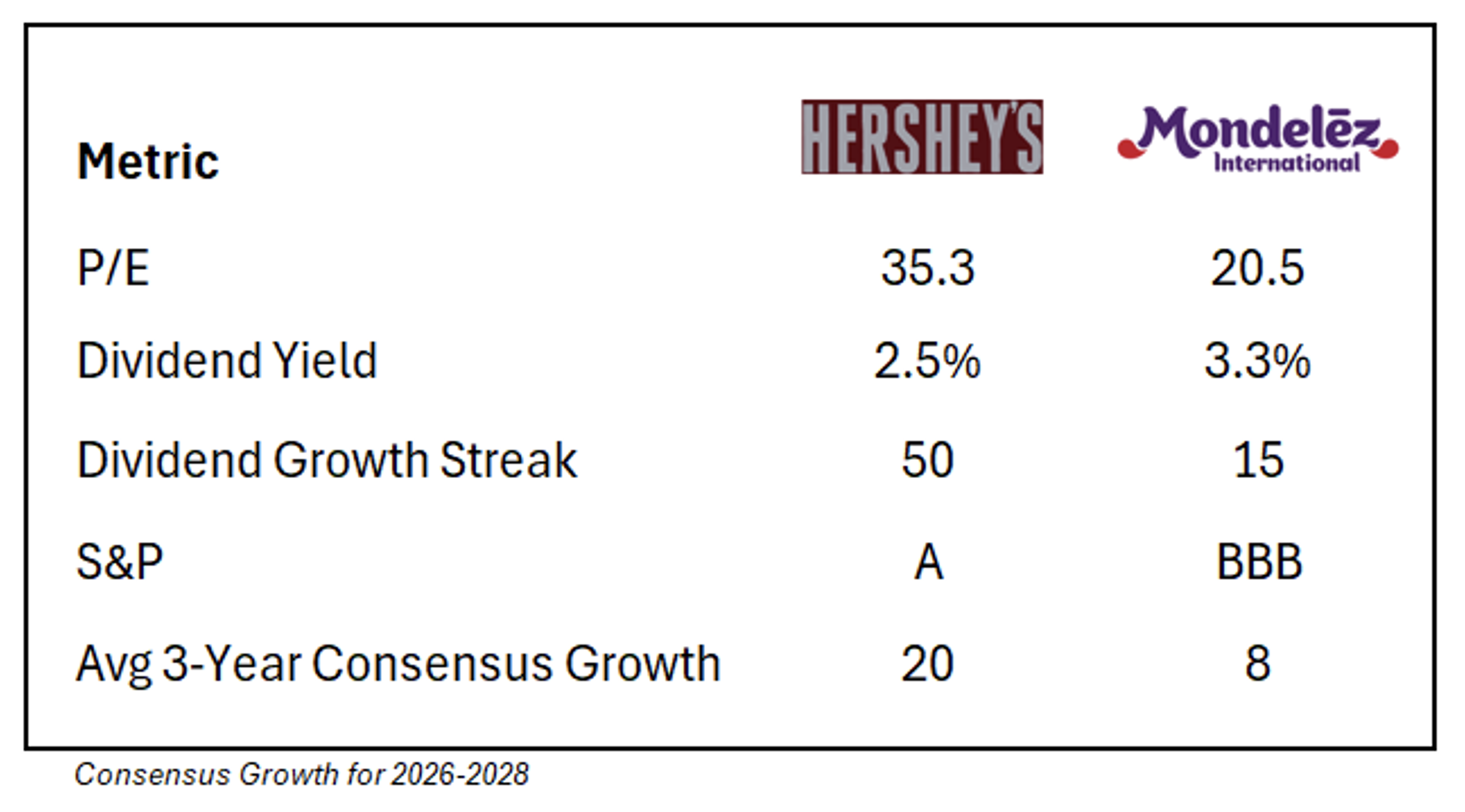

As impressive as Hershey is, though, I would wait on a pullback before buying. It was a bargain when we recommended it last year. But, as shown below, shares are now yielding 2.5% and trading at a premium of 35.5 price to earnings (P/E) ratio.

Source: FAST Graphs

Keeping it simple also means waiting for the price to be right. That’s the situation I see with Hershey today.

Another Sweet Tooth Stock

Mondelez International (MDLZ), meanwhile, is known for its global snack brand portfolio. Oreo, Cadbury, Milka, Toblerone, Ritz, Trident, and Halls: These treats boast massive shelf presence with decades of consumer habit behind them.

Mondelez’s moat is strongest in biscuits and cookies, where it’s basically king. Oreo alone is a monster with huge production volumes, global recognition, and endless variations.

This company has a global scale advantage throughout the U.S., Europe, emerging markets, Latin America, and Asia. But it is exposed to competitive private-label cookies that do manage to hold their own.

Essentially, Hershey’s moat is tighter, with the U.S. chocolate aisle dominated by its products.

Still, Mondelez’s dividend growth has been solid, averaging about 10% over recent years. The company pays regular quarterly dividends and has increased them for 14 consecutive years.

Shares are now trading at 20.5 times – just below their normal multiple of 21.3 times, with a dividend yield of 3.3%. As seen below, Mondelez is a reasonable buy today with a modest margin of safety.

Source: FAST Graphs

Both Mondelez and Hershey are very clear what they’re about and how they handle their business. It’s easy to understand their appeal – and how they keep their customers coming back for more.

That’s what makes them such KISS-able considerations this February. Just remember to wait until the price is right.

Source: Wide Moat Research

Regards,

Brad Thomas

Editor, Wide Moat Daily

P.S. Make sure to tune into The Wide Moat Show this week, where Nick and I will be featuring more keep-it-simple stocks. You don’t want to miss this Valentine’s Day edition. Who knows… it might pay for next year’s presents and then some.

|