Editor’s Note: Today is President’s Day, a market holiday. In lieu of our typical Wide Moat Daily essay, we’re sharing a lightly edited excerpt from Stephen Hester’s latest edition of Intelligent Options Advisor. As Stephen puts it, private credit is in the news… for all the wrong reasons. But behind the sell-off is something much simpler – fear. Read on for the full analysis.

There’s a lot of talk about private credit right now… and it isn’t good.

“No income [is] being generated” – Megan Neenan, managing director at Fitch

“[Business development companies (“BDCs”)] are expected to mark down positions even in good assets” – Reuters

“We have no way of knowing how far the decline will go” – Howard Marks, CEO of Oaktree Capital Management

“Earnings are… going to be very hard to estimate” – Robert Dodd, analyst at Raymond James

And last but not least:

“Dividend massacre in this crisis is already breaking records, but it just started” – Wolf Street

These are all quotes about private credit. Most were directed at publicly traded BDCs since they are the part of the industry everyone sees. And these statements were made by widely followed analysts and investors.

No wonder private and public BDCs – and the asset managers in charge of them – have found their stock prices under pressure.

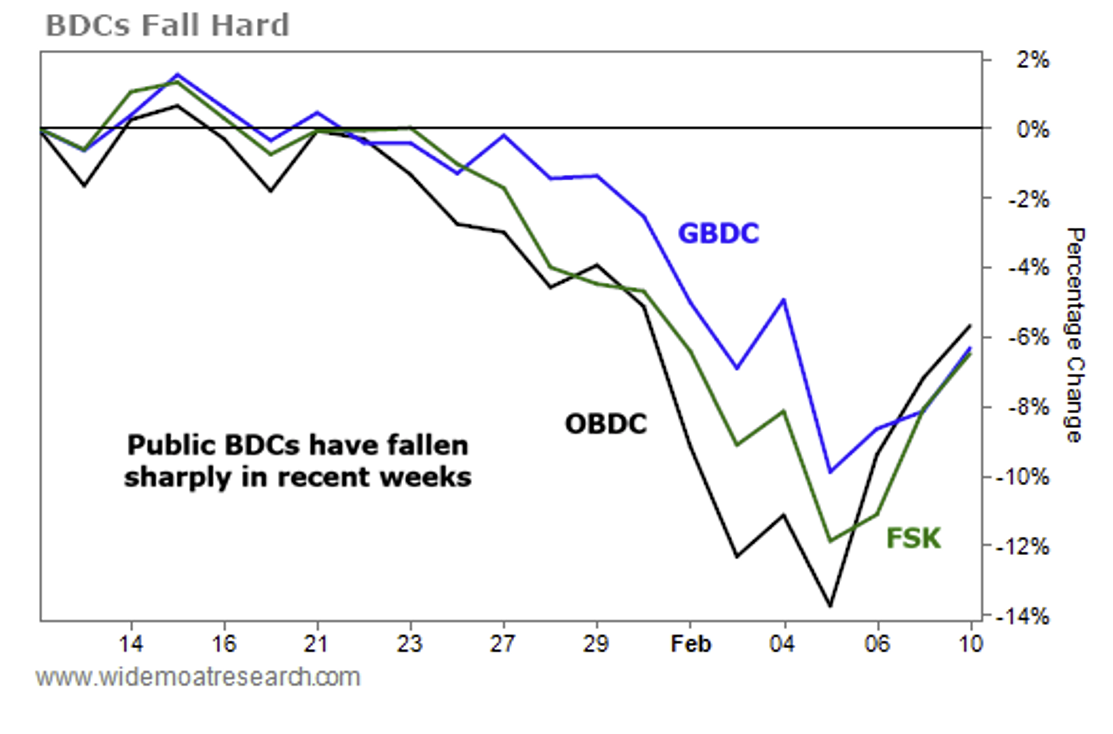

See for yourself:

What you’re looking at is FS KKR Capital (FSK), Blue Owl Capital (OBDC), and Golub Capital BDC (GBDC) – three of the largest, most liquid BDCs on the market. And they all have something else in common – they’ve fallen in recent weeks.

But there is something else you need to know: None of the quotes above are recent. They are from March and April 2020.

The recent jitters around private credit are nothing new. I’ve seen it off and on for years. The last “big one” was during the COVID era. But would you like to guess how these assets performed in months and years following that?

The VanEck BDC Income Fund (BIZD), the best proxy for publicly traded BDCs, gained 19.38% in April 2020 alone. It gained another 12.08% in May. A year later, it was up another 45%.

Today, investors are once again nervous about private credit and BDCs. Today, I’ll show you why that is, how it’s bringing even great firms lower, and what it could mean for investors brave enough to wade into that panic.

But first, we should get the lay of the land…

The Banking Crisis Never Went Away

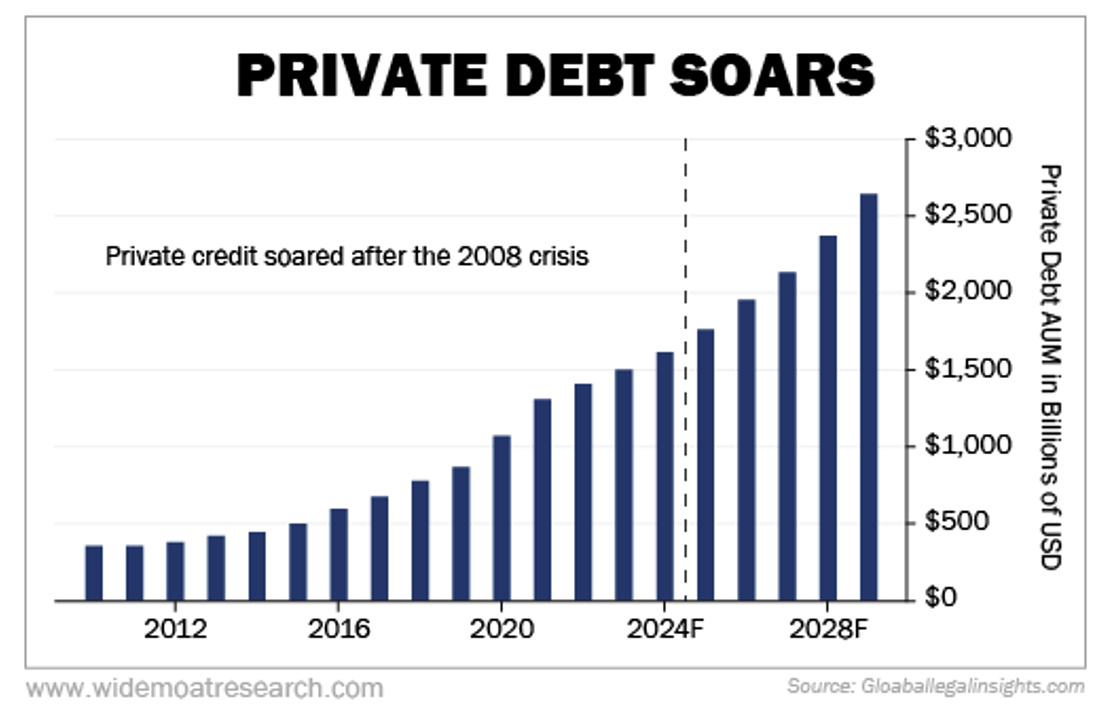

At a very high level, “private credit” is simply loans that are issued by investment firms rather than banks. So, instead of receiving financing from a JPMorgan, a company might turn to firms like Blackstone, Apollo, or Ares.

The origin of the modern private credit industry starts in the years following the 2008 financial crisis. legislation like the Dodd-Frank Wall Street Reform and Consumer Protection Act made small- and medium-sized business lending much more difficult for larger banks. So, they essentially stopped and focused almost exclusively on fee-rich deals involving other giant companies.

But that demand for credit from medium-sized businesses didn’t go away. Some of that demand was picked up by the regional banks which – for decades – had found a “sweet spot” lending to companies with 200-or-so employees.

Then, in 2023, the regional banks pulled back.

Starting in March that year, many regional banks either failed or nearly failed. You probably remember pictures of depositors lining up at Silicon Valley Bank locations to withdraw funds. The Federal Reserve and the Treasury stepped in to stabilize the system. JPMorgan Chase (JPM) did its part by acquiring First Republic in May of that year. And, for most people, the story was mostly over by late summer.

But the banking troubles never really went away…

By the third quarter of 2023, the Fed’s Senior Loan Officer Survey reported tightening standards and reduced lending in banks’ commercial and industrial (C&I) divisions. This problem really hasn’t gotten better.

As of November 2025, the Federal Deposit Insurance Corporation (“FDIC”) reported banks’ total unrealized losses on securities of $337.1 billion. A lot of people think the crisis ended with Silicon Valley Bank’s collapse. But many banks are still nervous to this day. Two more banks quietly failed last year.

Put simply: The big banks pulling back after 2008 set the stage for private credit to flourish. But regional banks pulling back was like adding rocket fuel to the machine.

This created a tsunami of opportunity for private credit. That’s why it has grown from an around $250 billion business in 2010 to close to $2 trillion today. And it’s expected to keep growing at a rapid pace.

But, more recently, investors have been jittery about this space. And it goes back to – of all things – new AI models released earlier this month

The “SaaS Apocalypse”

As I wrote recently:

The “reason” [for recent volatility in the stock market] was the introduction of a new artificial-intelligence (“AI”) model from Anthropic. The model goes beyond simple “chatbot” features. It proved itself capable of automating tasks typically done with enterprise software.

Put another way, investors are starting to ask the right questions.

The question isn’t whether AI will change the world. That part is largely settled for most of us. AI is already reshaping software development, logistics, drug discovery, customer service, and a lot more.

Instead, the market started asking the more dangerous question: Who is actually making money from this… And who could potentially be put out of business?

In short, investors are worried that the growth story for many Software as a Service (“SaaS”) companies is over. These companies aren’t going bankrupt overnight, but they could be under pressure if new AI tools disrupt their business models.

This fear has bled over into the firms that lend to these companies. After all, enterprise software is typically 15% to 25% of every diversified private-credit portfolio. That’s the thinking, anyway.

But, so far at least, I’ve seen precisely zero stories about private software companies losing business to AI startups and becoming financially stressed. They may be out there, but I can’t find any examples.

Instead, I see something much simpler – momentum selling. It’s fear, in other words.

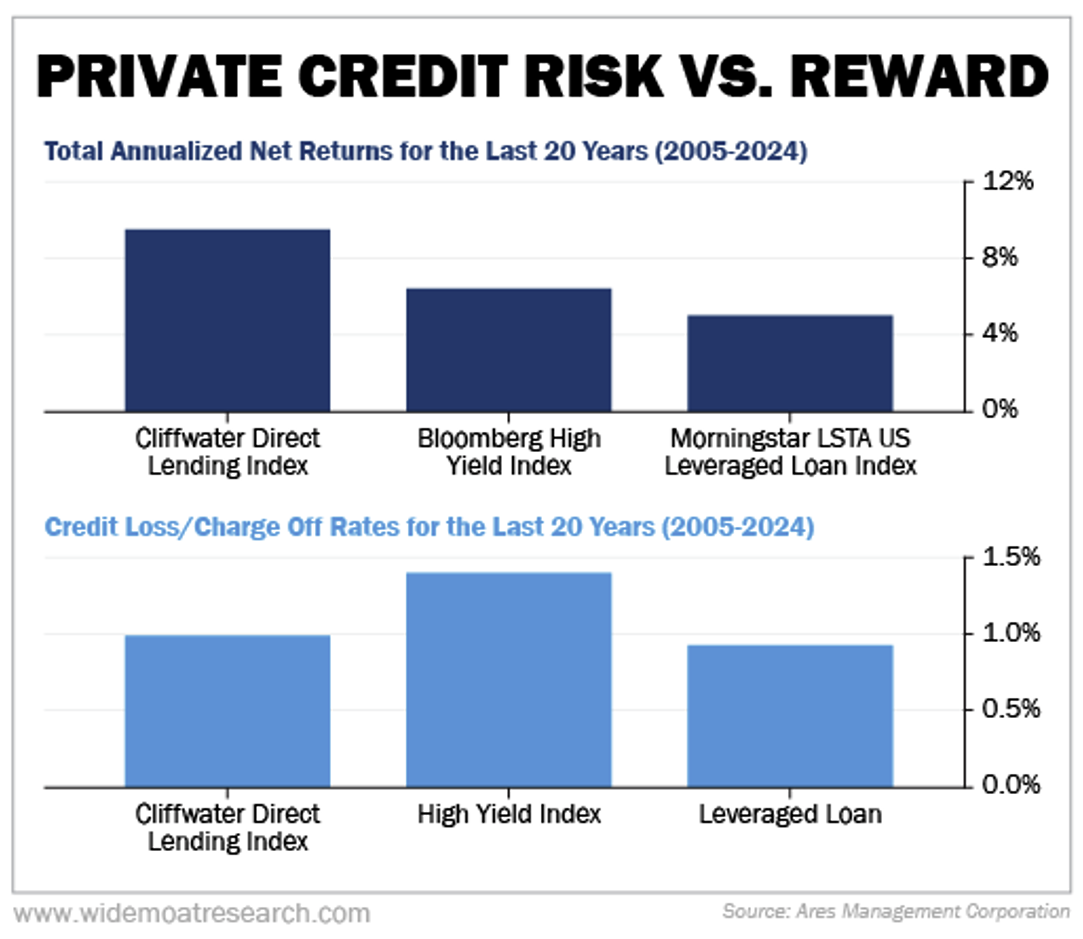

And the benefits to private credit investors remains appealing. Have a look at the next chart.

On the left, we see the Cliffwater Direct Lending Index. This is the bread and butter of private credit. It generated total annualized net returns (after all fees) of 9.54% for the past 20 years. Essentially all of that is in the form of income. We can compare this with the Bloomberg High Yield Index, which delivered 6.45% using the same metric and timeframe. There’s also the Morningstar LSTA US Leveraged Loan Index at 5.03%.

Given the much higher annualized return, you’d expect that the loan losses associated with the Cliffwater Index would be much higher than the Bloomberg High Yield Index and the Morningstar LSTA US Leveraged Loan Index.

But have a look at the chart on the bottom.

We can see that Cliffwater delivered 48% better returns over the 20-year period with 29% lower loan losses. Leveraged loans had slightly lower loan losses at 0.93% annually versus Cliffwater’s 1.01%, but it also generated only about half the income.

The market is fearful about private credit right now – no doubt.

But fear never cares about fundamentals. Fear sells first and asks questions later. Fear never thinks about which companies have actual exposure to new risks.

That’s what happened in 2020 when everyone got it exactly wrong.

I suspect this latest panic will be remembered the same way.

Regards,

Stephen Hester

Chief Analyst, Wide Moat Research

|