Let’s talk trees today.

Not Christmas trees, mind you. But that’s a great topic, too.

Today, we’re looking at a real estate investment trust (“REIT”) sector I normally don’t write about – timber, or timberland.

By market capitalization, timberland REITs make up just 3% of the equity side of the REIT universe. And, frankly, they might make the news the least out of every other sector.

REIT-related stories these days usually center around data centers. With good reason, I might add, as I lay out in this brand-new presentation.

It’s understandable that timberland doesn’t capture the same interest from REIT investors. After all, like the trees in their portfolio, they just kind of sit there and grow slowly but surely.

Boring or not, though, as I point out in REITs for Dummies:

The lumber industry is intensely important to societal development. Yes, the need for actual building materials ebbs and flows. But the ability to build new houses is always a necessity; and single-family homes in the United States are mostly built from lumber products. We’re talking about 150 to 300 trees per house. Multifamily and commercial buildings are incorporating those materials more and more too.

This brings me to the reason why I haven’t written about timber REITs in quite a while. The housing market hasn’t been much of a market since the COVID-19 boom years.

The Rise and Fall of the Housing Market

Few people probably would have predicted that a global pandemic would be such a boon for U.S. housing prices. But that’s precisely what happened.

In response to the market crash and a locked-down global economy, the Federal Reserve cut its rate to essentially zero. It also restarted quantitative easing, flooding the markets with liquidity and forcing down longer-term rates. This, in turn, helped bring mortgages down to the lowest levels on record. For a brief moment in time, a 30-year fixed could be had for about 2.6%.

Another interesting phenomenon was the rise of remote work. Suddenly, many people were no longer tied to one geographic location. And so, they got up and moved. States like Texas, Florida, and the Carolinas saw a massive influx of new residents. And housing prices in those states took a turn higher as well.

In the fourth quarter of 2019, the average American home could be bought for about $327,000. By the end of 2022, that figure was nearly $443,000.

And as the housing market went, so went lumber. The combination of a roaring housing market and snarled supply chains – thus limiting supply – caused lumber to trade like an AI stock. In March 2020, lumber traded for about $272 per thousand board feet. By May 2021, it was nearly $1,500 – a 450% move in just over a year from wood, of all things.

And as lumber soared, so did the timber REITs. Many of the ones I track more than doubled during that time.

But that was a long time ago…

You remember what happened next. Rates rose. Mortgages rose. Lumber and timber REITs slid as the housing market cooled.

I last wrote about the housing market on July 31, dubbing it “a mess.”

At the time, we’d just learned “that the 2025 spring season – typically the busiest time to buy and sell a home – was the worst it [had] been in over a decade.” Moreover, there wasn’t:

… much hope for the summer months considering all the data we now have. This includes how sales of existing homes fell to a seasonally adjusted average annual rate of 3.93 million – a nine-month low.

The 30-year mortgage rate was “only” 6.475% at the time versus its 7.04% in January. But actual home prices were still rising, with the median existing house selling “for a record $435,300, according to the National Association of Realtors.”

As such:

Even if someone managed to have the $87,000 necessary for a 20% downpayment, Bankrate says they’d still be paying over $2,000 per month once property taxes and homeowner’s insurance are considered. And if they only have 10%, which is still $43,530… they’re paying $2,285 per month.

Fortunately, mortgage rates are now down to 6.08%, and home prices have decreased by 1.4% in the past three months. We also learned last week that there were more houses on the market last month versus November 2024 – with 13% more active listings and 1.7% more new listings.

As such, we could see home prices dip even further as those sellers face more competition.

Increased interest in homeownership should also mean homebuilders like D.R. Horton (DHI), Lennar (LEN), and PulteGroup (PHM) will start ramping up construction efforts.

And if that does happen, there’s one timber REIT I’ll be keeping an eye on.

Weyerhaeuser Is in the House

Weyerhaeuser (WY) is the largest private real estate owner of timberlands in North America. Its portfolio spans 10.4 million acres in the U.S. alone, with another 13 million acres licensed in Canada.

This timber giant is also one of the continent’s largest low-cost manufacturers of wood products. It boasts a diversified mix of 33 plants, including 21 distribution centers in the largest U.S. homebuilding markets.

But it’s not just in the tree business. It leases some of its land for solar and wind farms; generates carbon credits; participates in carbon recapture; and develops residential, commercial, and industrial sales in Florida, Louisiana, and the Carolinas.

In terms of business “moats” – assets or angles that keep it safe from market competition – Weyerhaeuser has unmatched competitive advantages in regard to:

-

Scale, with 2.5 million acres of land on the West Coast, 6.7 million in the South, and 1.2 million in the North

-

Capital allocation, where it returns 75% to 80% of adjusted funds available for distribution to shareholders

-

Proprietary AI and machine-learning tools that give it stronger business development capabilities

-

Best-in-class operations and performance

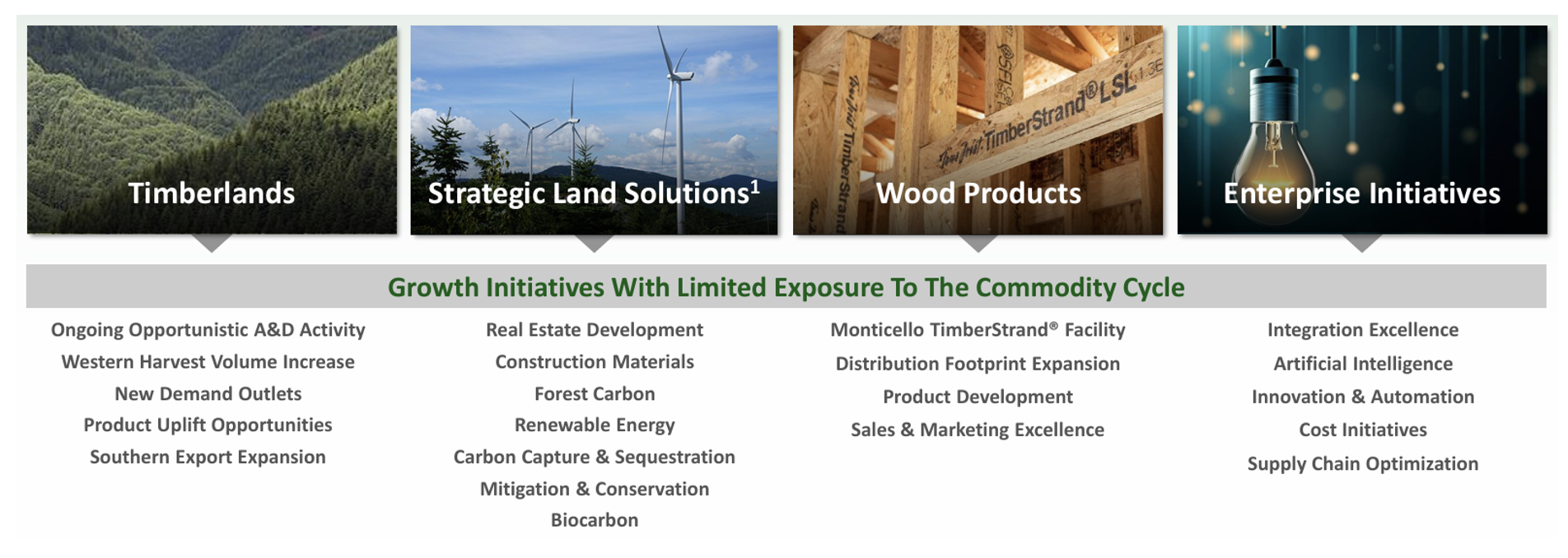

At a recent Investor Day conference, Weyerhaeuser laid out its roadmap to generate multiyear growth. This involves improving cash flow per share, reducing volatility…

And delivering an incremental $1.5 billion of adjusted earnings before interest, taxes, depreciation, and amortization (“EBITDA”) by 2030 through its timberlands, strategic land solutions, wood products, and enterprise initiatives.

Source: WY Investor Presentation

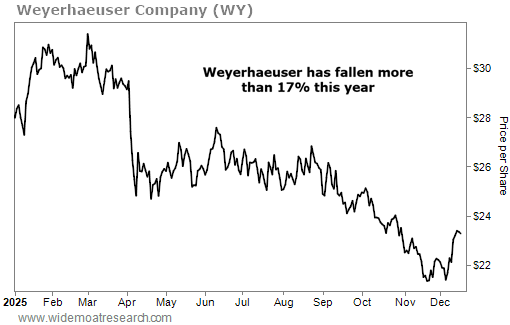

It’s clear that this company has value – not that you would know from looking at its share price, which has dropped more than 17% year to date. Weak home sales and tariff uncertainties have weighed on the stock.

But this puts it in a very buyable range with a seemingly sustainable 3.6% dividend yield.

Source: Yahoo Finance

The divergence between Weyerhaeuser’s price and net asset value (“NAV”) has become remarkably attractive. Consensus NAV is around $36, about 30% above where it’s currently trading.

Now, a primary catalyst for that growth, other than management’s 2030 EBITDA target of $1.5 billion, is rate cuts. And the Fed did just indicate it isn’t likely to drop interest rates at its next meeting.

Then again, it said that last time, too… only to cut for a third time in a row. But even if it breaks that streak next month, the Fed still expects to reduce rates further at some point in 2026. That will help Weyerhaeuser reduce interest on its debt and generate more free cash flow to pay out dividends and buy back shares.

Mr. Market may not be able to see the forest for the trees quite yet. But I can see this timber giant’s potential to harvest annualized returns of around 30% by the end of next year.

It’s just one more example of how boring can be beautiful when you buy in at the right price.

Regards,

Brad Thomas

Editor, Wide Moat Daily

|