Time flies…

I recently found myself reminiscing about 15 years ago… back when real estate investment trusts (“REITs”) changed the entire course of my life.

At the time, I was employed by a Texas-based real estate developer as a senior strategist focused on bringing in new clients. I was happy for that job.

It was after a bad partnership that devastated my own commercial real estate (“CRE”) company. Then, when I finally got it back up and running, the 2008 financial crisis happened, destroying everything I’d worked so hard to rebuild.

With a wife and five children to provide for, I desperately needed this new job, humbling though it might have been to go from self-employed to employee.

A few months in, I asked my boss if I could write a few articles on a new financial publication platform called Seeking Alpha. It was focused on do-it-yourself investing, a crowd I figured I could do well with.

He gave me the green light, and so I went for it, primarily focusing on REITs since that was a space I knew well, having even done work for some of them before. That knowledge seemed to resonate with Seeking Alpha readers, including some of my employer’s higher-ups, who told me directly.

As it turned out, however, it rubbed others in my company the wrong way.

While on a business trip to the West Coast, I got an e-mail from the general counsel telling me I had to stop. Floored, I responded by saying that I would remove the company’s name from my bio.

For that, they fired me. No further discussion or explanation given.

Driving to the airport and then flying home, I had plenty of time to think about the weight of it all. The uncertainties could have been overwhelming. But something inside me just knew I could make something out of educating investors about REITs.

That something turned out to be right.

Within a few years, I had over 50,000 followers, which grew to 100,000 and then over 125,000. In fact, I was the most-followed writer on Seeking Alpha for years.

I also began publishing newsletters under the iREIT® and Forbes Real Estate brands. I became a regular guest lecturer at significant universities such as Penn State and Cornell. And I went on to publish four real estate-oriented books, the last (so far) being REITs for Dummies.

And then, of course, there was the founding of Wide Moat Research… and all of the subscribers we count today.

Providing research on REITs changed my life. So, today, let’s get back to basics. Where do REITs stand? How have they been performing? And what should we expect going forward?

REITs Through the (Recent) Years

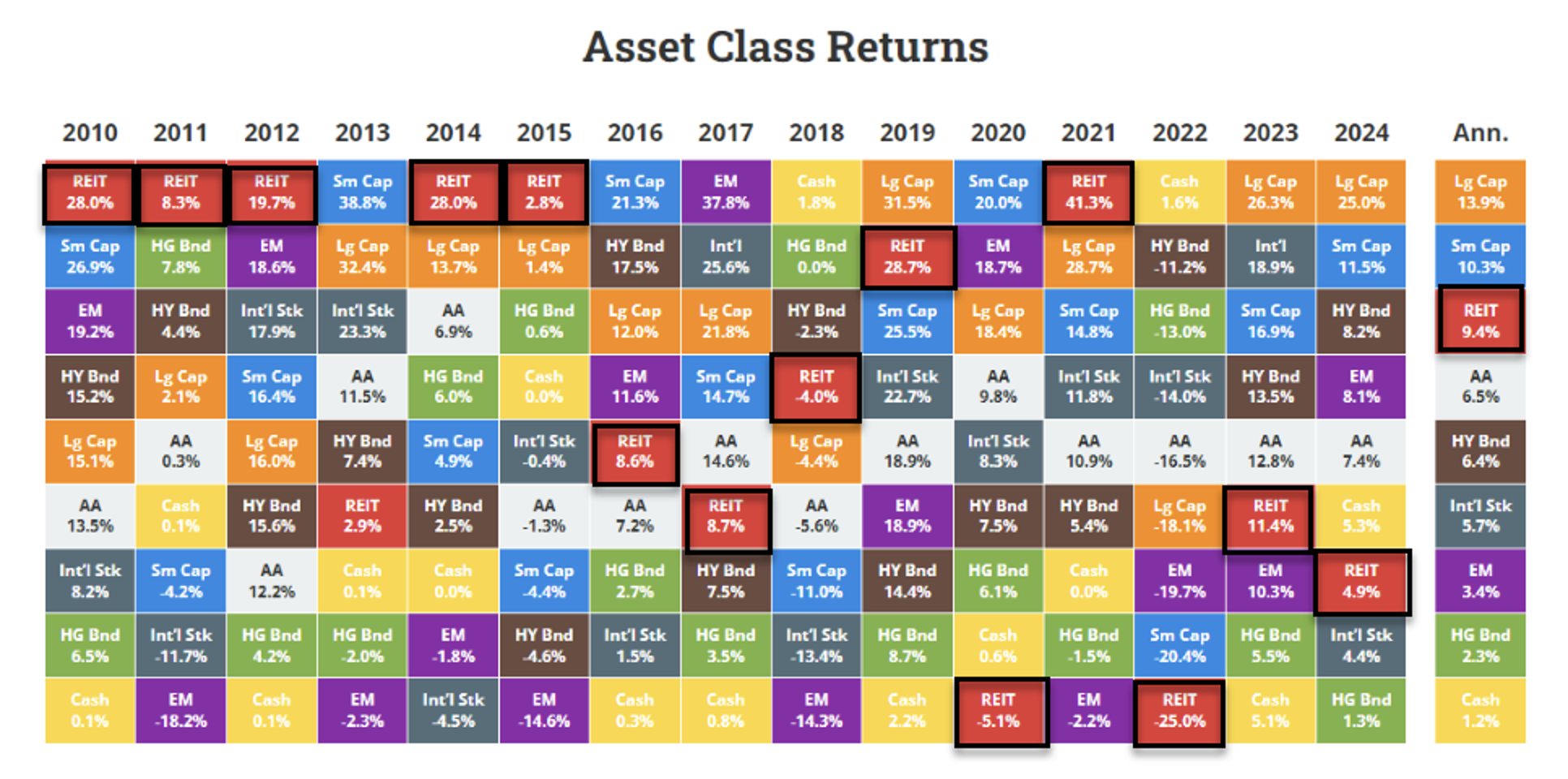

Over the past 15 years, REITs as a category have performed fairly well, especially coming out of the Great Recession, which leveled so many other real estate ventures, my own included.

REITs were the top-performing asset class in 2010, 2011, 2012, 2014, 2015, and 2021 alike.

In other years, as we’ve seen more recently, REITs suffered a clear fall from Wall Street’s favor – something that needs to be explained.

After the crash in 2008, the Federal Reserve immediately slashed interest rates in order to encourage economic activity. By December, the effective Federal Funds Rate had fallen to the lowest positive range of 0.00% to 0.25%.

This was the start of a prolonged period of ultra-low interest rates. And since REITs tend to thrive when interest rates are down, investors piled into them.

When the Federal Reserve began to raise interest rates in December 2015, it increased the cost of capital, thereby reducing REITs’ perceived attractiveness. Please note how I said “perceived.” Because, contrary to popular opinion, these CRE businesses can still grow quite nicely in less opportune environments, raising their dividends while maintaining well-balanced books.

People will think what they want to think, though. So when the Fed raised interest rates even more in 2017, REIT shares underperformed yet again.

2020, of course, was a different story. The pandemic and ensuing lockdowns shuttered CRE properties everywhere. So, I understand why investors fled from real estate, and why it became the year’s worst-performing sector of that year.

REITs rocketed right back the next year, bringing in the stock market’s best gains. Though that share-value victory was short-lived, as the Fed hiked interest rates a total of 11 times starting in 2022.

As I explained in a recent article:

… it was 2021 when financing rates fell and the generous yields from real estate investments looked very attractive compared with the near-zero returns from Treasurys. But what should also stand out is the drawdown in 2022 that saw those macro tailwinds turn into headwinds. Real estate has limped along ever since.

I’ve advocated holding REITs regardless due to their history of paying out safe dividends with higher-than-average yields. However, I think their shares are about to take off, too.

In short, I see the turning point up ahead. It’s so close that it’s practically here.

The Economic Cycle Is Turning in REITs’ Favor

I’ve witnessed over three decades of economic cycles now – and I’ve never seen a time when REIT valuations were so attractive. They’re boasting strong fundamentals, favorable supply trends, and capital markets that are wide open…

Yet their share prices are undervalued to the point of being ridiculous.

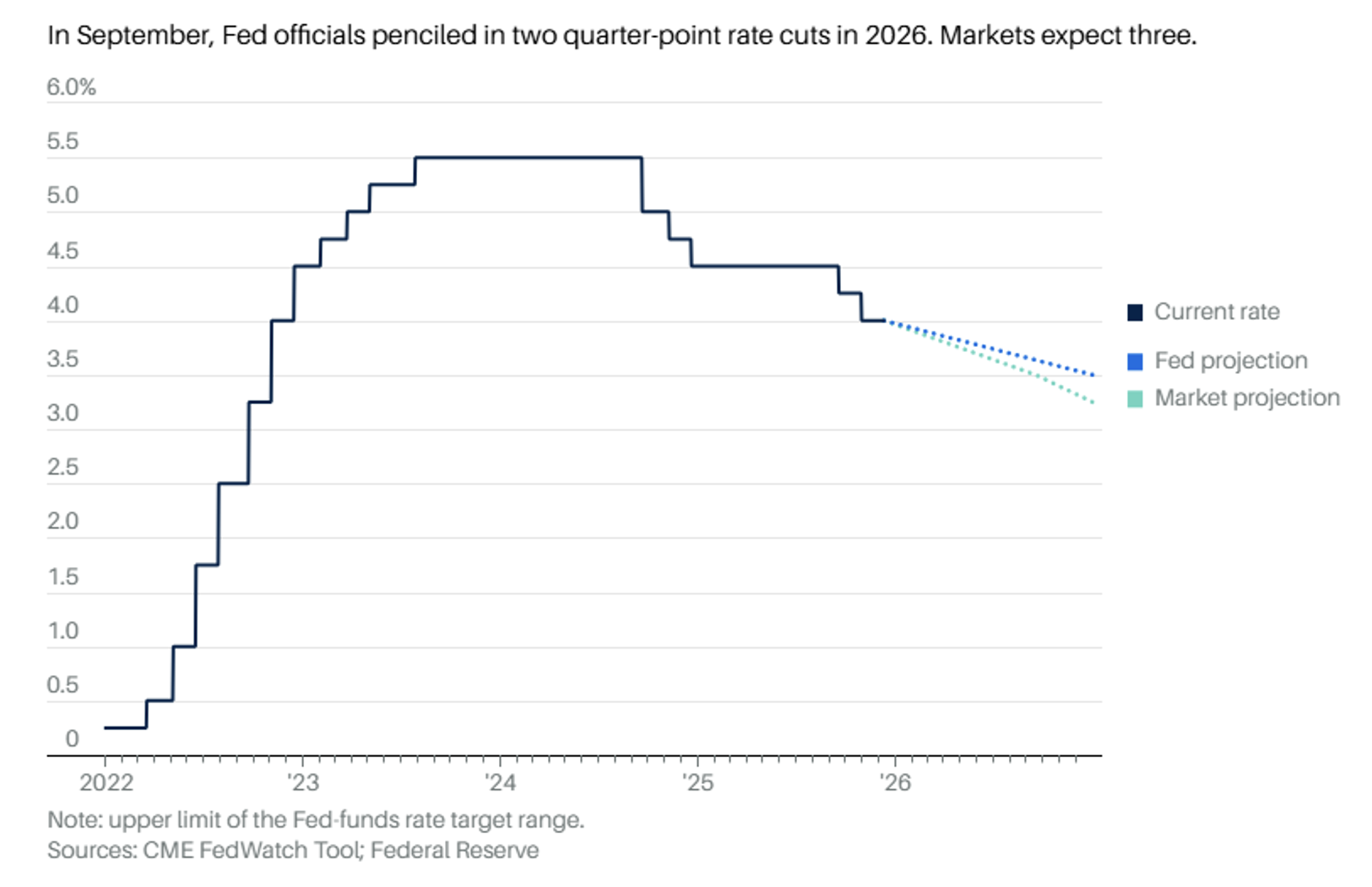

The Fed will have already made its decision on whether to cut or not cut by the time you read this. And the economic consensus is that we’re in for a final 0.25% reduction this year. In which case, it would only reinforce income and capital inflows into the REIT sector.

But even if there is a surprise and rates stay the same for the time being, I’m still exceptionally optimistic.

For one thing, the Fed is still expecting to cut rates further next year. It’s saying two times; the market is projecting three.

Source: Barron’s

And in the meantime, institutional investors – market players with the most money to throw around – are beginning to see what I see. Nareit reported earlier this week that:

Leading institutional investors, including pensions and sovereign wealth funds, are expanding their use of REITs, drawn to their higher total returns, strong operations, scale, access to emerging sectors, and efficient global exposure.

That engagement should go far in bumping up these CRE plays’ very undervalued stocks.

While I don’t have insider access to their books and boardrooms concerning which REITs they’re eyeing and buying up… I do have some suggestions. I recently put together a special report that highlights certain mission-critical REIT categories that should benefit, especially next year.

Readers of The Wide Moat Letter can access it right here. And if you’re not a member, you can learn more by going right here.

I also encourage you to tune in to tomorrow’s Wide Moat Show, where I’ll be discussing another three companies with my fellow host and Wide Moat Research analyst Nick Ward.

The possibilities aren’t quite endless when it comes to REITs right now. There are definite companies I wouldn’t touch with a 10-foot pole.

But I’m confident the larger sector is full of profitable opportunities we haven’t seen for quite some time. And I, for one, want to make the most of them.

Regards,

Brad Thomas

Editor, Wide Moat Daily

|