The new Gulf War just entered a dangerous new phase: direct strikes on major energy infrastructure.

Over the past 48 hours, Iran targeted key facilities in Qatar, Saudi Arabia, and the United Arab Emirates. Israel also bombed one of Iran’s natural gas fields. We’ve moved from a traditional military conflict to a “no limits” strategy with energy infrastructure in the crosshairs.

In this edition of the Wide Moat Daily, we’ll break down exactly what’s been damaged, the impact on supply, and who feels the pain (spoiler: the U.S. fares better than you might think).

Winners and Losers in Natural Gas

Qatar’s Ras Laffan liquified natural gas (“LNG”) complex was targeted by Iranian missiles. Two full liquefaction trains (numbers four and six) are offline – that’s 12.8 million tonnes per year gone, or 17% of Qatar’s total LNG exports. Up to 25% of the nation’s output could be at risk if more trains are affected.

Let’s put that into context.

Qatar normally supplies roughly 20% of the world’s LNG. A double-digit percentage hit to its export capacity is going to leave a mark on the global economy. QatarEnergy estimated it’ll take three to five years for a full recovery. The amount of money at stake means repairs could be fast-tracked, but output will be down for a long time.

Qatar is an obvious loser, but who else?

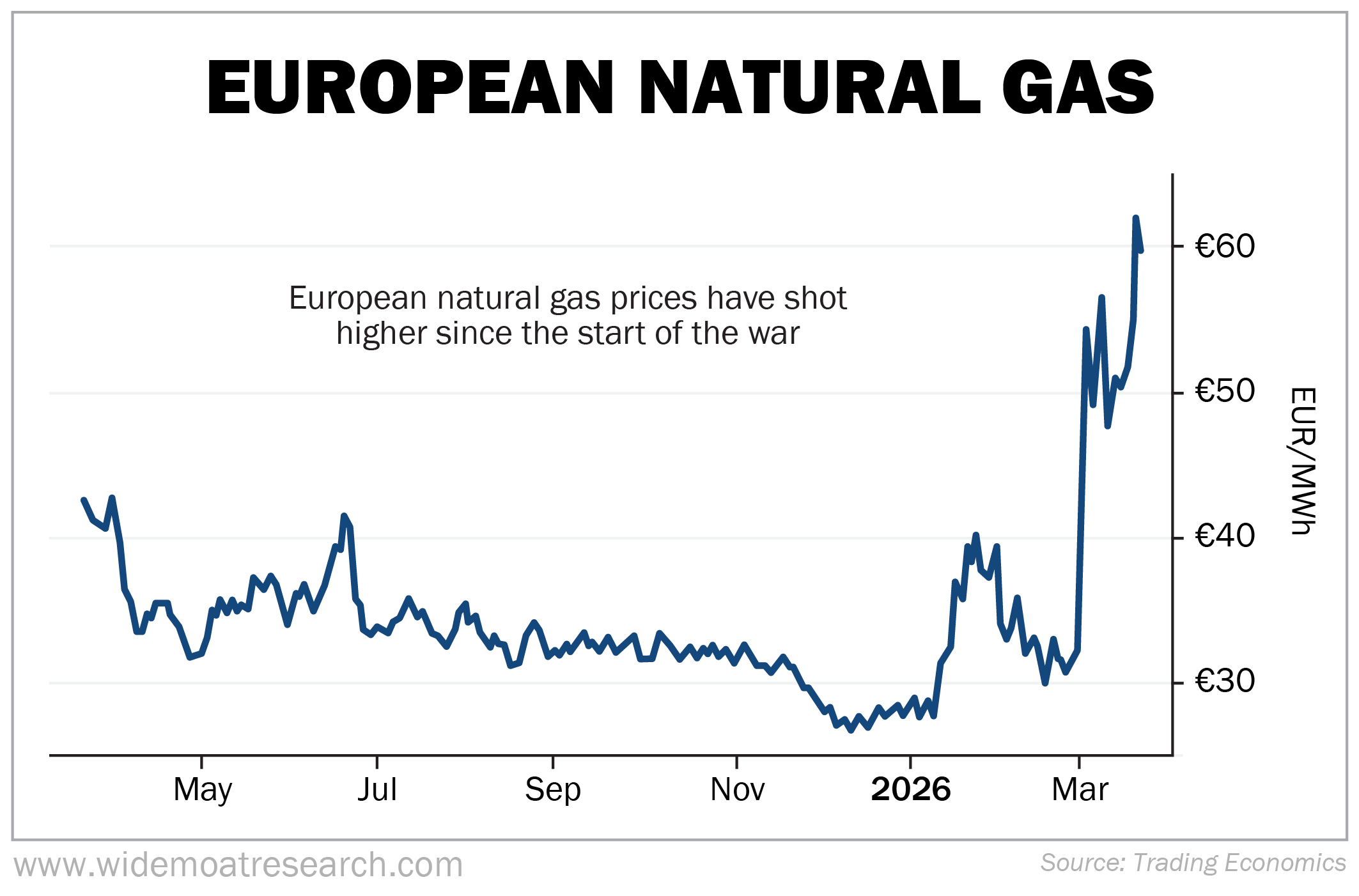

Europe and Asia are the big buyers, and it won’t be easy or cheap to replace Qatar’s LNG supplies. The timing for the Europeans could not be worse. In December, the European Union (“EU”) announced its plans to completely cut off Russian gas imports by November 2027. The EU assumed it would find plenty of supply from producers like Qatar. Now, that’s uncertain.

The result is that European natural gas prices jumped from roughly 30 euros per megawatt hour (EUR/MWh) to over 60 EUR/MWh in recent days.

Source: Trading Economics, March 20, 2026

With Europe famously reliant on imports from Russia and the Middle East for energy, it’s a clear loser.

But what about the U.S.?

America is a large exporter of LNG thanks to a recent infrastructure investment boom starting in 2016. Cheniere Energy (LNG) built Sabine Pass in Louisiana and invested over $50 billion. Sempra (SRE) Infrastructure/Energy, Venture Global (VG), and Dominion Energy (D) all invested tens of billions. One of the largest projects in the startup phase is Golden Pass LNG – a partnership between Exxon Mobil (XOM) and none other than QatarEnergy.

These LNG exports are suddenly in much greater demand. U.S. LNG cargoes are already seeing premium pricing. The U.S. exported a record 111 million tons of LNG in 2025 and sits at 95% to 98% utilization. That means supply can’t move more than another 4 million to 6 million tons annually without more projects like Golden Pass LNG coming online. Let’s run through a quick calculation to determine if U.S. LNG is really setting up for windfall profits.

We’ll assume the U.S. fills 40% of Qatar’s gap via higher facility utilization and faster ramp-ups on new projects. That results in a conservative estimate of another 5 million tons per year. With scarcity premiums driving up prices by at least $3 per million British thermal units (“MMBtu”), and 1 tonne of LNG being 52 MMBtu, that works out to $780 million per year or $3.9 billion.

While a lot of money, that’s not where the real money comes from. Adding the premium pricing to the existing 111 million tonnes the U.S. already exports is another $8.7 billion in profits.

Keep in mind that this is not revenue – the full cost to extract, process, and ship the LNG is already accounted for. Over a five-year period, that’s just under $50 billion in additional profits for the industry. That’s roughly the market capitalization of Cheniere Energy or Dominion Energy. If you were wondering why Cheniere’s stock price has gone from under $200 late last year to over $285 today, now you know.

Other Middle East Assets Attacked

Iran struck Saudi Arabia’s Saudi Aramco Mobil Refinery Company (“SAMREF”) facility along the Red Sea coast. Saudi Arabia forced precautionary shutdowns that took 550,000 barrels per day off the global market. This wasn’t due to extensive damage like Qatar’s and should be back to normal in three months or less.

The U.S. won’t feel much pain since we are not big buyers of their refined products. But it does push global crude prices higher, helping U.S. producers but hurting consumers. The main losers here are those buying specialty refined products like jet fuel. Prices rose 11.2% in the past week and are up about 100% year over year in most markets.

Critically, the crack spread (the difference in the price of crude and a refined product, in this case jet, fuel) increased by 269.5% year over year. Jet fuel premiums are now at their largest since post-Katrina 2005. Usually, it’s a $10 to $30 per barrel (“bbl”) premium to buy jet fuel over traditional crude. Today, it’s $85 to $95 per bbl. To put it another way, the premium to buy jet fuel now exceeds the cost of crude oil in many markets.

Valero Energy (VLO), Marathon Petroleum (MPC), and Phillips 66 (PSX) are among the biggest winners, plus the super-majors like Exxon and Chevron that both drill for and refine oil and natural gas.

The biggest loser is airlines. They pay the inflated price of jet fuel and hedges (locking in prices into the future) aren’t used by all airlines, and when they are, it’s partial protection.

The UAE’s Habshan Gas Facilities and Fujairah Oil Terminal were shut down due to debris from intercepted Iranian missiles. These support a big percentage of Abu Dhabi’s crude and natural gas exports. Repairs could bring them back online in the next few weeks, notwithstanding more attacks. This is another sharp stick into the side of Asian and European markets.

Iran has also been on the receiving end of energy infrastructure attacks. On March 18, 2026, Israel hit facilities linked to the South Pars gas field. Interestingly, this is shared with Qatar, geologically. Iran’s half of the field is the nation’s biggest gas asset and supplies 70% to 75% of its total natural gas production. The latest data shows that roughly 12% of its total gas production was affected, with 20% possible.

But here’s where the attacks on Iran’s energy assets differ. Nearly 100% of Iran’s gas is used domestically for electricity. There is essentially no impact to global markets. Instead, this directly punishes Iran’s domestic economy.

Conclusion

The strikes on critical global energy infrastructure are real and painful. A large chunk of global LNG, for example, will be offline for years. Elevated natural gas prices in Europe and Asia will slow growth until things normalize. Each facility that goes offline creates a complex web of outcomes.

But here’s the practical angle for most people reading this: the U.S. is one of the few potential net winners from this.

At the very least, there are large segments of the American energy industry receiving huge gains at little to no cost. This also cements America’s role as a reliable LNG exporter for European and Asian buyers that may be more cautious about long-term contracts with Middle East partners for the foreseeable future.

Regards,

Stephen Hester

Chief analyst, Wide Moat Research

|