Do you believe in the American Dream?

If you’re like most Americans, the answer is… not anymore.

Here’s The Wall Street Journal (“WSJ“) earlier this month:

Nearly 70% of people said they believe the American dream – that if you work hard, you will get ahead – no longer holds true or never did, the highest level in nearly 15 years of surveys.

What’s interesting is that 15 years ago would have been 2010, the depths of the Great Recession. Americans are more pessimistic than they were during the worst recession in the 21st century?

It seems like the age-old American mantra of hard work, frugality, and saving for one’s future is losing its luster. And the new sense of pessimism is particularly acute with Generation Z.

A Harvard Kennedy School survey from a few months ago found that “more than 4 in 10 young Americans under 30 say they’re ‘barely getting by’ financially, while just 16% report doing well or very well.”

They’re also struggling to find jobs, as WSJ pointed out in a separate article:

What do you hire a 22-year-old college graduate for these days?

For a growing number of bosses, the answer is not much – AI can do the work instead.

At Chicago recruiting firm Hirewell, marketing agency clients have all but stopped requesting entry-level staff – young grads once in high demand but whose work is now a “home run” for AI, the firm’s chief growth officer said.

This seems to be spilling over into young people’s opinion of the American Dream. A Pew survey from May of last year found that 60% of Americans aged 18 to 29 believe the American Dream is not possible.

No matter how you slice it, the kids don’t appear to be alright.

And they’re turning to a surprising place to address their precarious financial situation.

The youngsters are focused on dividends!

Not YOLO, Just Yield

A recent Bloomberg article highlights the fact that a growing cohort of disillusioned Gen Z are flocking toward high-yielding investments as they attempt to exit the rat race… ASAP.

The idea of slaving away for decades, pinching pennies, and putting away savings to enjoy a few good years of retirement isn’t working for them.

As the article states, the traditional American financial timeline seems like a “rip-off” to the youngest generation of workers. And it has sparked the rise of financial influencers preaching the benefits of financial freedom and passive income.

From Bloomberg:

It’s a strange twist: Dividends – once the stodgiest corner of investing – have become the new hot thing with jaded Gen Zers hellbent on quitting and retiring early.

So far, so good.

And in some ways, I feel like the team here has been ahead of the curve.

Preaching about financial freedom? Planning for an early retirement? Extolling the benefits of dividends?! That sounds like Wide Moat Research!

Heck, Brad and I have a YouTube channel all about passive income. If any Gen Zs are reading this, subscribe here!

But wait, here’s where things get odd:

But the new playbook isn’t just about reliable payers like Coca-Cola Co. and Exxon Mobil Corp. Today’s dividend crowd is piling into [exchange-traded funds, or ETFs] offering eye-popping yields generated by complex derivatives.

The broad category of income-generating ETFs captured one in six dollars sent to equity ETFs as a whole in 2025, bringing the overall size of the sector to $750 billion. The most aggressive ones – dangling yields above 8% – have quadrupled in size in just three years to about $160 billion.

And that’s where I start getting worried…

Dividends Are Great… If They’re Reliable

Brad and I don’t just love dividends… we love safe, reliably growing dividends.

We’re not willing to sacrifice quality or earnings durability in the pursuit of unsustainably high yields. And that’s exactly what a lot of these Gen Z income investors are doing.

The issue with many of the highest-yielding ETFs is that they’re robbing Peter to pay Paul, so to speak, with their income-generating strategies.

Typically, these ETFs are focused on options strategies which sacrifice long-term upside in favor of present-day income.

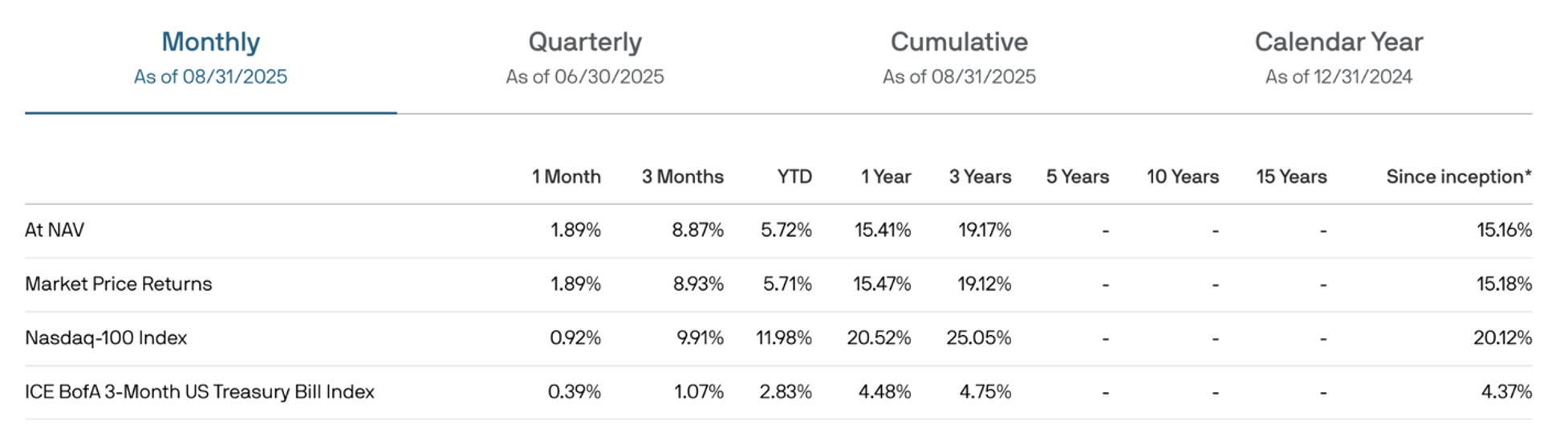

One of the most popular funds in this income-oriented area of the market is the JPMorgan Nasdaq Equity Premium Income Fund (JEPQ).

What this fund does is hold high-growth stocks (often the popular technology stocks of the day) and sell options against them to generate large premiums. These premiums are then returned to shareholders in the form of a dividend.

This strategy has worked well for investors since JEPQ’s inception. As you can see below, the fund has generated returns north of 15% since it was created in 2022. That’s great.

But if an investor had bought the Nasdaq 100 Index instead of this income-oriented vehicle, they would be much richer. The Nasdaq 100 produced total returns north of 20% during this same period.

(Note: Below, “NAV” stands for “net asset value.”)

If you’re at or near retirement, these types of funds might make sense. But, for the vast majority of investors, it’s not a good idea to focus primarily on short-term income while the underlying NAV of your holdings erodes away.

Also, many of these popular income-oriented ETFs have not been at battle during a recession.

None of these Gen Z investors have managed money throughout a prolonged bear market. Sure, we had a blip of a recession in 2020, but the market experienced a rapid V-shaped recovery.

That’s not normal.

Since World War II, the average U.S. recession has lasted nearly a year… and stock market recoveries have taken much longer.

A lengthy bear market could bring about lower asset values and options premiums for these high-yielding ETFs, resulting in a negative double-whammy for these funds, hurting their net asset values and income levels.

In a situation like that, I have a lot of concern for the financial well-being of investors (of any age) placing all of their eggs in these potentially risky baskets.

When something seems too good to be true, it probably is.

A Message to Gen Z: Do This Instead

If there are any Gen Zs reading this, I want you to know that I get it.

Most of you were children in the aftermath of the Great Recession. COVID-19 and the lockdowns came around right as you were graduating high school and entering college. Then came inflation, putting houses out of reach for many of you. And now, you’re not only competing with each other for jobs, you also have to contend with a world of AI.

I could understand the pessimism. And I could understand why you’d want to pull the proverbial rip cord as soon as possible. But not like this.

Instead of chasing double-digit yields with these options-oriented income funds, you’re better off buying and holding very high-quality dividend growers.

Remember, growing fundamentals (sales, earnings, cash flows) are what makes dividend growth sustainable over the long term. What’s more, not only do growing fundamentals support rising dividends, but also rising share prices.

If you like ETFs, there are also options for that.

The Schwab U.S. Dividend Equity Fund (SCHD) doesn’t use risky options strategies and has produced double-digit annualized total returns (12.60%) since its inception in 2011.

The top holdings are companies like AbbVie (ABBV), Chevron (CVX), Home Depot (HD), Verizon Communications (VZ), and Coca-Cola (KO). These are stocks that have not only provided consistent share price appreciation throughout a wide variety of broad market conditions, but also reliable dividend growth.

SCHD’s three-year dividend growth rate (“DGR”) is 9.01%, its five-year DGR is 12.99%, and its 10-year DGR is 11.10%.

Sure, the fund’s 3.8% yield might not be as attractive… right now. But the buy, hold, and reinvest strategy will be much more sustainable over the long term.

I get it. I truly do. We all want to retire ASAP.

But patience is key. Investing and retirement planning isn’t a sprint. It’s a marathon. And anyone who attempts to take a shortcut usually ends up doing a lot of damage to their future prospects.

Remember, if it seems too good to be true, it probably is.

Regards,

Nick Ward

Analyst, Wide Moat Research

|