This was the podcast The Wall Street Journal (“WSJ“) published this week:

WSJ isn’t alone.

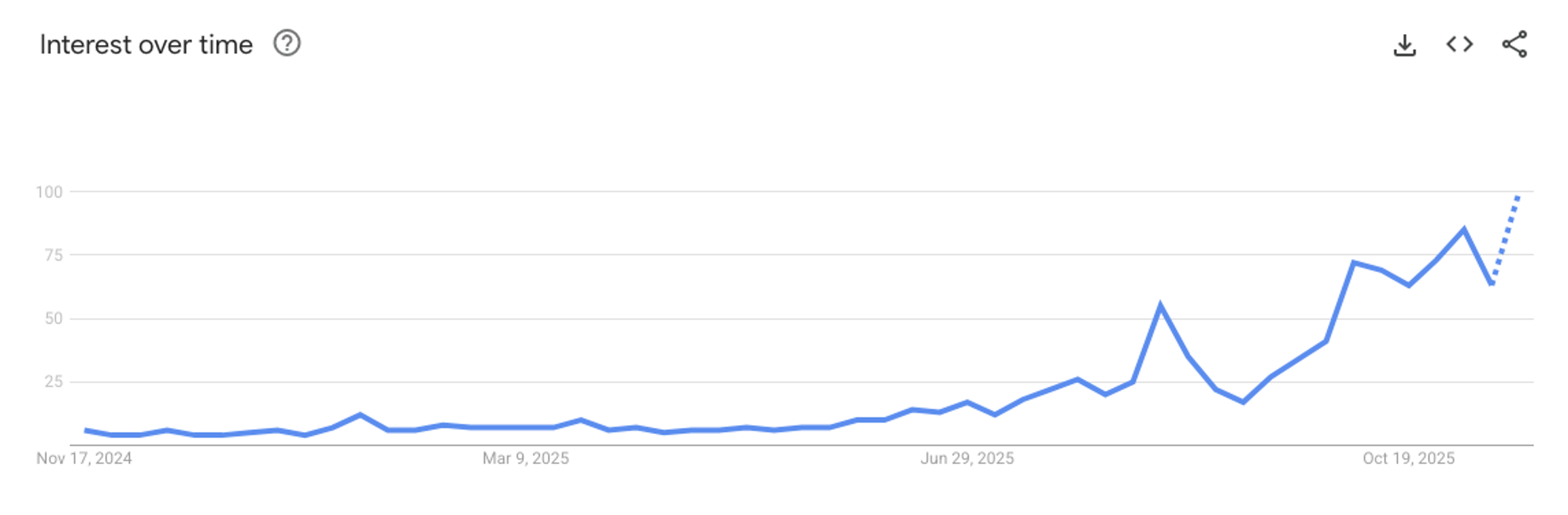

Here’s a Google Trends chart – which tracks the popularity of a search term – for “AI Bubble.”

There’s a lot of bubble talk…

And yet, for all the consternation, would you like to guess how far the S&P 500 is off from its highs? It’s about 5% as I write.

Yes, really.

I covered this a few weeks ago. Bubbles do not form when everybody is worried about a bubble. As I put it at the time:

You think people were sounding the alarm during the dot-com bubble? I mean, some people were. But most of the market was busy explaining why webpage views were more important than earnings and why it made sense for an unprofitable pet-food delivery company to spend $2.2 million on a single Super Bowl ad.

Now, that’s a bubble.

That doesn’t mean there aren’t things to worry about.

Because there are.

What the Market Worries About

OpenAI is reportedly making $13 billion in annual revenue. That’s a big number. But it’s not as big as the $1.4 trillion in spending commitments from the company.

Sam Altman – CEO of OpenAI – was strangely defensive earlier this month when it was pointed out how much bigger that spending number was:

First of all, we’re doing well more revenue than that. Second of all, Brad, if you want to sell your shares, I’ll find you a buyer[.]

I mean, that’s a fair question, right? “How the hell are you going to pay for this?” usually is.

So, yes, you could worry about that.

Then there’s this…

Aswath Damodaran, professor of finance and corporate valuation at the New York University Stern School of Business, otherwise known as “the Dean of Valuation,”- recently joined Scott Galloway on a podcast. He highlighted his belief that without AI capex in recent years, we’d be in a recession.

That could be worrying. But, in another way, maybe we should all be thankful for the AI hype. It’s the rising tide that has stabilized the market in an otherwise poor economic environment.

There’s more…

Alphabet’s (GOOGL) CEO, Sundar Pichai, recently sat down for a special interview with BBC where he said, “We can look back at the Internet right now. There was clearly a lot of excess investment, but none of us would question whether the Internet was profound.”

Pichai continued, “I expect AI to be the same. So, I think it’s both rational and there are elements of irrationality through a moment like this.”

Markets tend to worry when you compare the trade everybody is following with the Internet buildout… no matter the caveats.

But that hasn’t stopped Alphabet from raising its 2025 capital expenditure (capex) guidance twice during the year. Currently, the company expects to spend more than $90 billion in 2025, largely on its AI-infrastructure (data centers) buildout.

And it doesn’t help that people like billionaire venture capitalist, Peter Thiel, recently liquidated his Nvidia stake and sold much of the Tesla holdings from his hedge fund.

Or that Softbank sold $5.3 billion worth of Nvidia shares recently to fund other AI investments.

Or that famed investor, Jeffrey Gundlach, CEO of DoubleLine Capital, is recommending a flight to safety. He’s urging investors to keep roughly 20% of their portfolios in cash because of “garbage lending” in the private credit space and overvaluation.

So, yes, you could worry about all those things.

But here’s what else you should do.

Do Nothing

The best reaction to bubble-talk is to simply do nothing. It’s hard to ignore headlines, but you probably should.

Remember this: For a bubble to pop, there has to be a catalyst.

In this context, that catalyst would probably be the end of hyperscaler capex. If/when that spending stops, the AI growth story will quickly deflate.

I’m sure that will happen one day, but probably not tomorrow…

Looking at Nvidia’s recent results and current capex guidance across the mega-cap tech space, it doesn’t appear as though any cracks are forming in the narrative.

Nvidia just posted earnings, beating Wall Street’s already lofty expectations by wide margins. The company’s third-quarter revenues were nearly $2 billion more than analysts expected. And the company’s fourth-quarter guidance came in at $65 billion (well above the $61.66 billion expectation).

Coming into the quarter, NVDA’s management touched upon a half-a-trillion-dollar backlog. During the third-quarter conference call, Colette Kress, the company’s CFO, said, “The number will grow.”

Nvidia just posted a gross margin of 73.6% on $57 billion in sales (up 62.5% on a year-over-year basis). The company is guiding toward a fourth-quarter gross margin in the 75% area (on $65 billion in sales).

All of these numbers point toward one thing: insatiable demand for AI-related compute hardware. The company said that its cloud computing graphics processing units are sold out with no end in sight because demand is accelerating.

Nvidia’s CEO, Jensen Huang, also said this on the call:

There’s been a lot of talk about an AI bubble. From our vantage point, we see something very different.

Simply put, demand still outpaces supply by a wide margin when it comes to data-center chips, and that story could last for years and years to come.

Maybe there is an AI bubble. But stock market bubbles have always been and will always be simply a part of long-term economic cycles.

They’ll form. They’ll pop. Some people will benefit. Others will lose. Ideally, everyone will learn a thing or two… and then the process will start again.

Thankfully, throughout all of these cycles, the stock market has continued to churn higher.

Here’s a chart from Guggenheim showing why…

Source: Guggenheim Investments

This chart shows that the value of the S&P 500 (SPY) rose from 44.06 in 1957 to 5881.63 by the end of 2024. The SPY is up another 13%-plus thus far in 2025, pushing its new price higher, to 6727 as I write this.

And chances are that number will continue to climb before we enter the next bear market. Markets climb wall after wall of worry. The world keeps spinning. Investors who stay the course do quite well.

That’s what I’d advise readers do. Stay disciplined. Stay the course.

And try not to worry…

Regards,

Nick Ward

Analyst, Wide Moat Research

|