I’m not usually the type of guy to say, “I told you so.”

But…

I told you so.

Two weeks ago, I covered the latest meme stock rally in these pages. The target for the “apes” this time was Beyond Meat (BYND).

At the time, the stock was up more than 1,000% in the span of a few trading days. Shares went from penny-stock status to around $7 per share. All this despite the fact that the company has never, ever turned a profit.

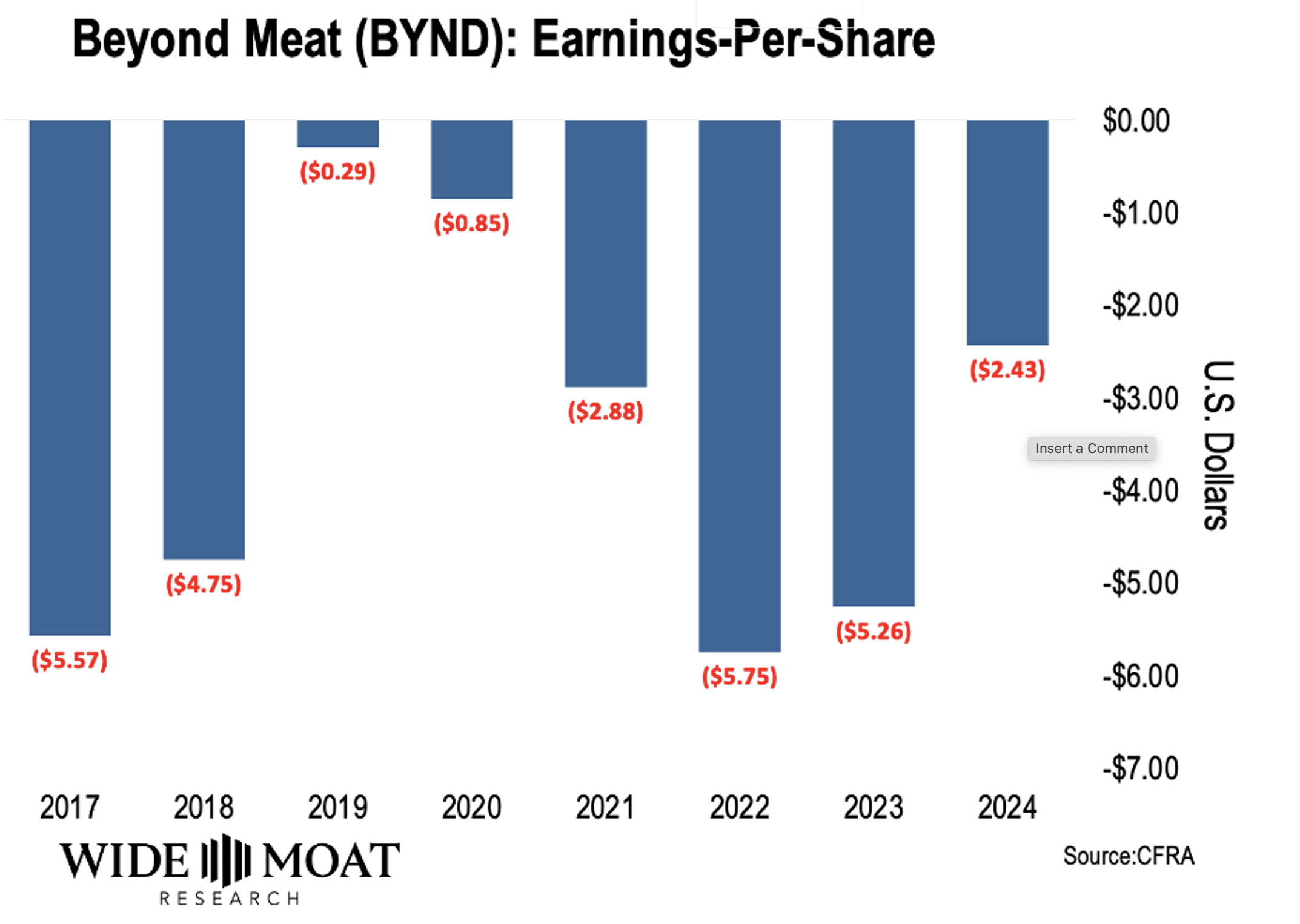

Here’s the chart I shared from the issue:

My advice was pretty straightforward:

I’m sure it goes without saying… but don’t buy this stock. You might as well light a bundle of cash on fire. It’s the same thing.

In the short term, the market is a voting machine. But in the long term, it’s a weighing machine. And what it weighs are profits.

And here’s the bad news: Beyond Meat has no profits!

The meme mania is an interesting phenomenon, but it’s not worthy of your investment.

Stay disciplined. Stay rational. Stay the course.

When I started looking into BYND on October 22, shares hit a recent high of $7.69. When we published that article on October 24, shares opened at $3.31 and closed at $2.19.

But then, the thinkable happened…

As I write, BYND shares are trading for just $1.27… down by nearly 50%. Traders who bought at the $7.69 highs are down by 83%.

And, no, they’re not “investors.” I said “traders” for a reason. Even that might be a bit generous. Perhaps “gamblers” might be more appropriate.

There was no fundamental justification for buying into that BYND rally. All of that pain could have been easily avoided.

Am I a soothsayer?

Of course not.

But when it comes to meme stocks, it doesn’t take a magician to spot a trainwreck.

Today, let’s go back to that advice from two weeks ago: Stay disciplined. Stay rational. Stay the course.

What is “the course” exactly?

This Is the Course

Investing isn’t always easy. But it can be pretty simple.

And the simplest, easiest, and most effective path to success is this:

-

Find the highest-quality companies.

-

Buy them when they’re trading for a fair price.

-

Hold them forever.

That’s it. It’s not always easy, but it is that simple.

Your biggest enemy will always be yourself. Following this strategy requires discipline and patience, something human nature isn’t always great at.

Two weeks ago, I shared a word of caution. Today, I’ll share a few opportunities that should be on your radar. If you can be patient and disciplined, I think you’ll want to be aware of them.

A Few High-Quality Stocks Trading at a Fair Price

Waste Management (NYSE: WM) is the U.S. leader in non-hazardous waste (think: trash pickup and landfill operation). It’s trading near 52-week lows. WM shares are down by 8% during the past month, resulting in significant underperformance on a year-to-date basis. Thus far during 2025, Waste Management is down by 0.6%. The S&P 500 is up by 15.7%.

I’m sure momentum traders hate a stock like this. I love it.

WM is a steady compounder. It has posted positive annual earnings-per-share (“EPS”) growth during nine out of the last 10 years. Waste Management has increased its annual dividend for 22 consecutive years. The company’s most recent dividend increase was 10%. The company’s five-year dividend growth rate is north of 8%. And after the stock’s recent sell-off, WM’s dividend yield is 1.64%.

A 1.6% yield growing at an 8% to 10% rate might not be exciting. But when a company can consistently produce results like that for decades on end, the compounding process results in a ton of wealth.

WM shares are up by 284% during the past decade… beating the S&P 500’s 234% 10-year gains by a wide margin.

Another blue-chip compounder trading near 52-week lows is Automatic Data Processing (Nasdaq: ADP), the world’s largest payment processor.

ADP’s fundamental growth record is even more impressive than Waste Management’s. ADP has posted positive annual EPS growth during each of the past 10 years and during 19 out of the last 20 (with the only miss being a negative 1% result in 2010).

Automatic Data Processing has raised its annual dividend for 49 consecutive years. ADP shares are down by 11.3% on the year, pushing its dividend yield up to 2.38%.

ADP’s most recent dividend increase was also 10%. This company’s five-year dividend growth rate is approximately 12%. And during the past decade, its shares have posted gains of 205%.

During the past 10 years, with dividends reinvested, the S&P 500 has produced a total return compound annual growth rate (“CAGR”) of 14.05%. Over the same period of time, ADP’s total return CAGR is 14.42%.

That’s the power of a reliably compounding dividend (especially when the yield is roughly 1% greater than the S&P 500’s).

Waste Management currently trades for 26.7 times forward earnings. Automatic Data Processing trades for about 23.7 times forward earnings.

Neither of these stocks is a screaming bargain right now. Both of their multiples are in line with their long-term averages, pointing toward fair valuation (from a historical perspective, anyway). But the good news is… that’s good enough.

You don’t need to find huge discounts to do well with blue chips. You just need to find a fair price and start accumulating shares.

Neither company is exciting. But people need their trash picked up. They need to get paid for work. That won’t change for the foreseeable future (or, perhaps ever).

Both are highly profitable, relatively boring companies that have generated life-changing wealth for investors over the long haul.

When thinking about investments, capital preservation is always top of mind. That’s why we don’t speculate at Wide Moat Research. And we certainly don’t gamble with our recommendations.

Some risks are worth taking. Others take you.

Just as anyone who bought BYND a couple of weeks ago.

Remember, follow the profits. They’ll eventually lead to sustainable, reliably increasing dividends. Compounding passive income is what will release you from your financial burdens and provide peace of mind.

Waste Management and Automatic Data Processing are great candidates to help you do that.

Who knows?

Maybe in a few years, I’ll get to say “I told you so” again.

And you’ll be happy to hear it.

Regards,

Nick Ward

Analyst, Wide Moat Research

|