In 1944, the Servicemen’s Readjustment Act was signed into law. You – and millions of Americans at the time – probably know it simply as the “GI Bill.”

The bill provided a series of benefits to returning veterans. They included reduced or free tuition costs, vocational training, and guaranteed low-interest, zero-down-payment home loans.

The program didn’t come cheap. By the time it was wrapped up in 1956, approximately $14.5 billion had been spent. That would be in the ballpark of $260 billion when adjusting for inflation, an enormous sum.

But it paid dividends…

College enrollment doubled by 1947. Access to affordable mortgages led to an explosion of residential development and the creation of the modern suburbs. The U.S. economy – instead of collapsing after the war, as some predicted – had itself a boom.

In some real sense, this one piece of legislation created the modern middle class. Over the years, it more than paid for itself as this new middle class provided higher and higher tax revenue to the federal government.

It’s considered by many to be the most successful domestic government program in history.

Why do I bring this up?

I bring it up because there’s a realistic chance that every American child born this year will be a millionaire.

Not now, of course. But eventually.

And it’s not because of a dollar collapse or hyperinflation. It will be because of the simple power of compounding over long periods of time and a new government initiative meant to support American families and keep the American dream alive.

There’s a new policy out of the Trump administration that isn’t being talked about enough. But the long-term benefits for America’s children are enormous.

I know, it’s tough to look at the news these days. There’s violence, disorder, protests, and divisive politics.

But if there’s one thing everybody can agree on, I think it’s this: Giving $1,000 to newborn babies is a good thing.

Seed Money

Trump Accounts are going live on July 5, 2026. These are essentially IRA accounts for children. The money in them grows tax deferred until they’re 59.5. But it can be accessed without the typical negative 10% early withdrawal penalty for things like education expenses for first home purchases.

The government is going to provide $1,000 of seed capital to start accounts for children born between January 1, 2026, and December 31, 2028.

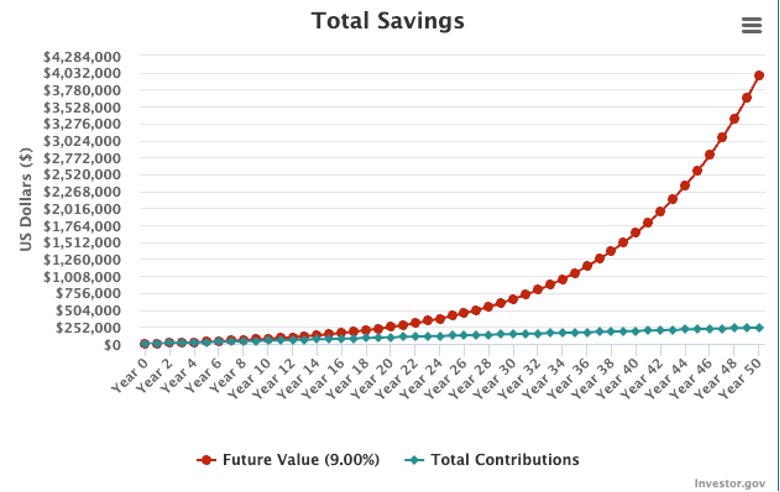

And while $1,000 might not seem like much, that money can grow. See for yourself below.

What you’re looking at is the compounded returns for a hypothetical investor using the following assumptions.

-

An initial investment of $1,000 (“seed money” from the government)

-

A contribution of $400 per month (roughly $100 per week)

-

An average annual return of 9% (the approximate long-term average for the S&P 500)

Do this for 50 years… and the portfolio is just shy of $4 million. That’s the sort of thing that can happen with patience and process. And it’s the sort of thing I hope we see more of with these government accounts.

One complaint that I’ve seen about this policy is that it’s more government spending when the deficit and national debt is already out of control. But, as it turns out, Trump Accounts may not end up being a burden for the government at all.

There are roughly 10,000 babies born a day in the U.S., meaning that these $1,000 seed deposits are going to add up to roughly $3.6 billion per year.

First, that’s a drop in the bucket of the federal government’s budget. For context, defense spending in fiscal year 2025 was $916.6 billion.

Second, the government might not end up footing all of the bill for this seed capital when it’s all said and done.

Since Trump Accounts were announced, several prominent philanthropists have said that they would be willing to provide the seed capital for the original $1,000 investment because of how strongly they believe in financial literacy and the importance of investing in the U.S. stock market.

For instance, this week, Brad Gerstner, the CEO of Altimeter Capital, said that he would contribute money to kids in his home state of Indiana.

“We have philanthropists that are going to claim every state,” Gerstner told CNBC.

Furthermore, parents/loved ones can also add money to these accounts each year with annual contribution caps, like how ROTH IRAs are currently run.

But even if the government does end up footing the bill, it could prove to be one of the best investments this country has made in decades… just like the GI Bill.

How It Works

According to Fidelity, there are rules as to what can be owned in the Trump Accounts. It appears that investors here will be limited to low-cost index funds or mutual funds that track the S&P 500 (max expenses ratios are 0.10%). Also, no leverage is allowed within the accounts.

Frankly, that sounds fine to me.

Providing children with exposure to the S&P 500 means that they will benefit from the growth of the American economy – and its strongest individual companies – throughout their lives.

Ideally, giving children the ability to track the value of their Trump Accounts throughout their young lives will birth a generation of young people who no longer fear the stock market, but instead, understand the power of compounding.

Removing leverage means that they will see that you don’t have to take shortcuts to get rich with U.S. stocks. Instead, all you have to do is buy and hold blue-chip U.S. companies and reinvest the dividends over the long term.

Maybe this money would be used to buy a house at 30 (bolstering the housing market) or maybe it will be left in the accounts until they’re ready to retire. Either way, the lessons learned by being forced to watch money in the markets over a long period of time will be invaluable.

I’m certainly not a fan of every decision that this administration has made. And I’d be lying if I said I felt comforted by what I’m seeing on the news these days.

But this is a good thing. Full stop.

I continue to believe in the strength of the U.S. free-market economy. And as someone who thinks that long-term investments in the U.S. stock market are the simplest and easiest way for people to climb the social ladder, I think the Trump administration has hit a home run with these Trump Accounts.

If you have (or plan on having) a child, you can learn more about this initiative at Trumpaccounts.gov. And if these early investments spark an interest in the stock market in your young one, be sure to sign them up for Wide Moat Daily where they can expand their financial literacy even further.

Regards,

Nick Ward

Analyst, Wide Moat Research

|