Bitcoin (BTC) has rallied by roughly 3,000% during the past month… in Iran.

For most of us, bitcoin has had a solid start to the year. Pull up most any chart for the crypto, and it will show an approximate 10% year-to-date return. That’s great, but it’s not 3,000%.

What gives?

The answer is that the 10% return is priced in dollars. But if you were buying/selling BTC with Iranian cash, it looks like Bitcoin has shot “to the moon,” as the crypto bulls like to say.

Of course, the truth is that bitcoin isn’t soaring in value. The Iranian rial (IRR) is falling. To be more precise… It’s collapsing.

The combination of domestic unrest, political instability, as well as new (and old) U.S. sanctions on the country has caused Iran’s currency to effectively crash.

The Iranian rial was never strong, but in recent days, it has lost half of its value against the U.S. dollar (USD). As I write this, it would require 1,092,500 IRR to exchange into just 1 USD.

Hyperinflation has taken off in the country. At the end of 2025, Iran’s official inflation rate was 42.5%. That rate is accelerating rapidly as the country’s economy collapses, making it so that much of the population can no longer afford basic staples like rice or bread.

The fact of the matter is, a handful of rials is now essentially worthless. The only Iranians who’ve done well for themselves – financially speaking – are those who had the foresight to dump cash and hold alternative assets, such as bitcoin or gold.

The window to do that is closed now. A single bitcoin now costs more than 106 billion IRR.

When currencies crash, economies crumble. Commerce stops. Who in their right mind would sell a product today when it’s likely to be worth 10% more (in constant currency, at least) the next day?

Bank runs occur. Lending stops. Debt is called. And chaos ensues.

Once the currency goes… everything else goes with it.

That’s the sad reality that Iranians are experiencing today.

And, at least according to some, that’s the path America is heading down as well.

Not Worth the Paper It’s Printed On

The collapse of Iran’s currency is not a new phenomenon. There have been similar crises in the past.

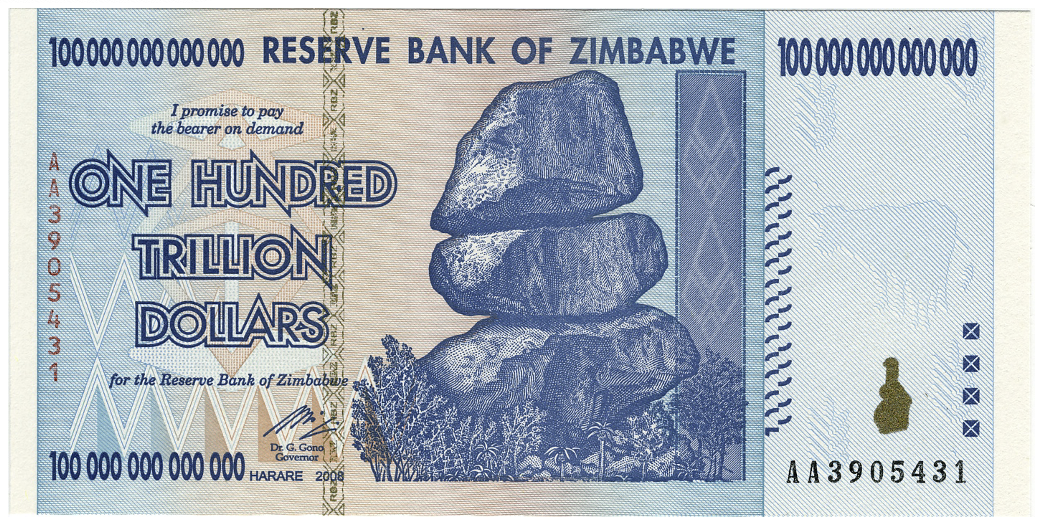

After the First World War, the currency issued by Germany’s Weimar Republic became so inflated that people filled wheelbarrels with the stuff to buy loaves of bread. Argentina has been dealing with hyperinflation – off and on – for decades. The country saw annual inflation of nearly 300% as recently as April 2024. And, of course, there was the infamous one-hundred-trillion-dollar note issued by Zimbabwe during the hyperinflation of 2009.

Source: Wikimedia Commons

Could the U.S. dollar be next?

You don’t have to look hard to find headlines about the supposed “death of the dollar.”

But, let me be clear: This is hyperbole… for now, at least.

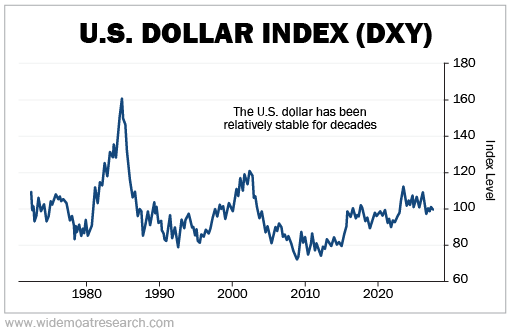

Yes, the U.S. Dollar Index (DXY) is down 9.6% over the past year. Put another way, the purchasing power of the USD has fallen by nearly 10% when compared with a weighted basket of six of the world’s other major currencies: the euro, the Japanese yen, the British pound, the Swedish krona, and the Swiss franc.

And, yes, it’s true that the dollar’s purchasing power has eroded over the years. I’m sure you remember a time when houses could be bought for around $100,000 and a vending machine soda was 50 cents.

But some perspective is in order.

First, the dollar – as measured by the DXY – has been remarkably stable over the decades.

There are outliers, of course. The dollar strengthened in the early 1980s as Federal Reserve Chair Paul Volcker hiked short-term rates to nearly 20% to “whip” inflation. And the dollar weakened through the 2000s as financial crises prompted emergency measures to force rates lower.

But, overall, this is not the type of chart that shows a currency on the brink of collapse.

As for inflation, it does bite. But the truth is that U.S. inflation is relatively tame. The most recent consumer price index (“CPI”) announcement from the U.S. Bureau of Labor Statistics came in at 2.7% year over year. That’s above the Federal Reserve’s 2% target, but well off of the 2022 highs, which were north of 9%. That may be uncomfortable, but it’s not hyperinflation.

But more to the point, the dollar is unlikely to collapse anytime soon for one simple reason – it’s the U.S. dollar!

It is the currency issued by the country with the world’s most advanced military, the largest economy, and the most liquid and trusted markets. And in the fact that most oil sales are conducted in U.S. dollars, and it creates almost permanent demand for U.S. greenbacks. The dollar is known as the global reserve currency for a reason. Because it is.

So, no, the dollar is far from dead. But maybe – just maybe – it could be dying… albeit very slowly.

On Debts and Deficits

Every year, the U.S. government collects revenue, mostly in the form of taxes. It then spends that money on a variety of programs – Social Security payments, Medicare, national defense, etc.

Despite the constant fighting in Washington, D.C., both sides of the aisle always seem to agree on one thing – spending more than they bring in. You know this as a deficit. And for fiscal year 2025, that deficit was some $1.77 trillion.

Now, in order to fill that hole, the U.S. Treasury issues debt. You know these as Treasury bills, notes, and bonds. The Treasury even issues new debt to help pay for interest on old debt. It’s a bit like paying off your credit card by taking out a mortgage.

The U.S. government has been doing this for years. And they get away with it because… well… it’s the U.S. government. As we already covered, the U.S. dollar is the world’s reserve currency. For that reason, the yield on the 10-year Treasury is typically the proxy for the “risk-free rate of return.”

But all things have a limit. And people are starting to wonder if even the mighty U.S. government is approaching one.

Did you know, for instance, that net interest on the national debt (all $38 trillion of it) was some $970 billion in fiscal year 2025? Did you further know that this was the first time that interest on the debt exceeded the spending on national defense?

If you didn’t, now you do.

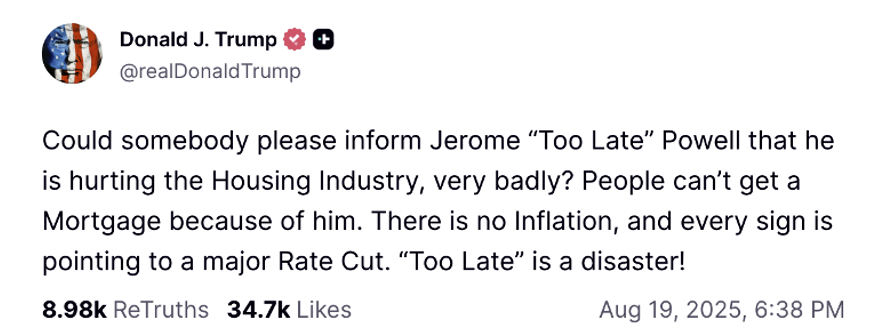

And now that you know, it answers another question – why President Trump has been hammering Jerome Powell.

Source: Truth Social

Trump hasn’t been shy about his desire for lower rates from the Fed. The hope is that, by lowering rates, the Fed will also help ease long-term rates lower. That, in turn, will reduce the government’s costs to borrow.

But things cranked up a notch when the Department of Justice opened a criminal investigation into Powell for, allegedly, lying to Congress. That’s a mess, to say the least. Even Trump’s Treasury Secretary, Scott Bessent, isn’t happy about it if recent reports are to be believed.

We haven’t even talked about the interference in private industry – caps on credit-card rates, banning corporate landlords, and trying to stop dividends for defense contractors. And we haven’t considered the geopolitical tensions around events like Venezuela and Greenland.

And before you say I’m heaping blame on Trump exclusively, I do have a bone to pick with the Biden admin as well.

The decision to seize Russia’s dollar-denominated assets as punishment for the invasion of Ukraine was a Rubicon of sorts. I’m certainly not here to defend Russia. On the contrary, I think they’re clearly in the wrong. But whatever you think of that conflict, just consider what message that action sent. It showed foreign governments that their dollar assets may not, in fact, be their assets. What country would put up with that risk? Perhaps it’s why central bank gold purchases have been soaring ever since.

Why does any of this matter?

It matters because, at the end of the day, all the Treasury rates are the perceived risk of lending to the U.S. government. For decades, that didn’t seem like much of a risk. But what happens if the bond market ever looks at all this debt, all this uncertainty, all this risk, and says… “no more”?

On that day, bonds crash. Rates will soar. Everybody will learn the hard way what “austerity” really means. As that happens, the value of the dollar will be called into question. I don’t know what that will look like specifically, but it will be ugly.

To be clear, I hope that never happens. Maybe this is the “Art of the Deal.”

Maybe the Trump administration has a grand plan that will result in strong employment, low inflation, lower interest rates, a booming stock market, and peace on Earth.

We can hope!

But hope is not a strategy. The chances of a full-blown debt and currency crisis in the near future may be slim… but they’re not zero.

Large, existential events like that don’t happen often. But they do happen.

So, what is an investor to do about all that?

The Silent Default (and Why You’ll Want to Own ‘Stuff’)

The most pressing concern for the United States’ long-term financial health is the debt. At nearly $40 trillion, growing your way out is going to be difficult. Not impossible, but difficult.

I’ve heard persuasive arguments that the only way to get out of the massive hole is for the U.S. to inflate its way out. My colleague Stephen Hester refers to this as a “silent default.” In other words, a good chunk of the debt could be paid down in nominal terms, but the paper will have been so devalued as to basically mean the same thing as an actual default.

This is the thinking behind the “debasement trade” and a big reason why precious metals have been on such a tear the past 12 months. In the past, I’ve also referred to this as the “anything but the dollar” trade.

But for our purposes, here’s another way to frame: The next several years will be the “Era of Stuff.”

What does that mean?

It means we may very well be entering a zeitgeist where paper assets (currency, government debt, etc.) loses its luster and real assets are the key to maintaining your purchasing power.

During the hyperinflation of the 1920s, astute Germans in Weimar began buying pianos. It’s not the worst idea. Pianos are beautiful items that held their value as the paper currency rapidly lost its value.

The United States is not Weimar Germany. And you have better options than pianos.

If the trends I’ve described above remain in place, you’re going to want to own scarce, valuable stuff like real estate, precious metals, and, yes, maybe even a little bitcoin.

You’re going to want to own stuff that’s compounding at a global scale. That means having exposure to stocks that represent real businesses with real pricing power and real, durable cash flows.

Energy commodities probably aren’t a bad bet, either. That means keeping an eye on oil companies with scale and wide moats. It means knowing about the many midstream firms that move these commodities from point A to point B and possess real-world infrastructure that is both vital and irreplaceable.

Heck, it could even be farmland.

Arable, water-rich land, will forever be sought after by humans. In December, the billionaire owner of the Los Angeles Rams, Stan Kroenke, made the largest land purchase in the U.S. in more than a decade, buying nearly 1 million acres of cattle/horse ranchland in New Mexico. He’s now the largest private landowner in the U.S., joining famous names like Ted Turner, Jeff Bezos, and Bill Gates, who are all ranked in the top 50 on the largest U.S. landowner list.

Obviously, you and I can’t go buy million-acre ranches with our pocket change, but you get the idea here. Billionaires are protecting the value of their savings by investing in vast swaths of land, and we can follow suit, albeit at a smaller scale.

I should be clear, we’re not in a total “cash is trash” environment yet. But if the dollar devaluation trend that we’ve seen play out over the past year or so accelerates, you’re going to want to rethink your holdings. That means potentially rebalancing toward assets and stocks that can provide sound returns and peace of mind for decades.

I don’t like writing essays like this.

Normally, I’m on my soapbox, and the message is usually the same: It’s not different this time. Ignore the fear. Buy the dip.

But given everything we’ve seen, I think I might be stepping down.

I hope I’m wrong. I truly do.

All the same, I’ll be tracking all of the relevant data points closely moving forward and assisting Brad with providing recommendations to Wide Moat Letter subscribers that should not only protect them but help them thrive.

Regards,

Nick Ward

Analyst, Wide Moat Research

|