Yesterday, while writing about the very real profit potential in certain Sun Belt-specific regional banks, I brought up the blue-state exodus.

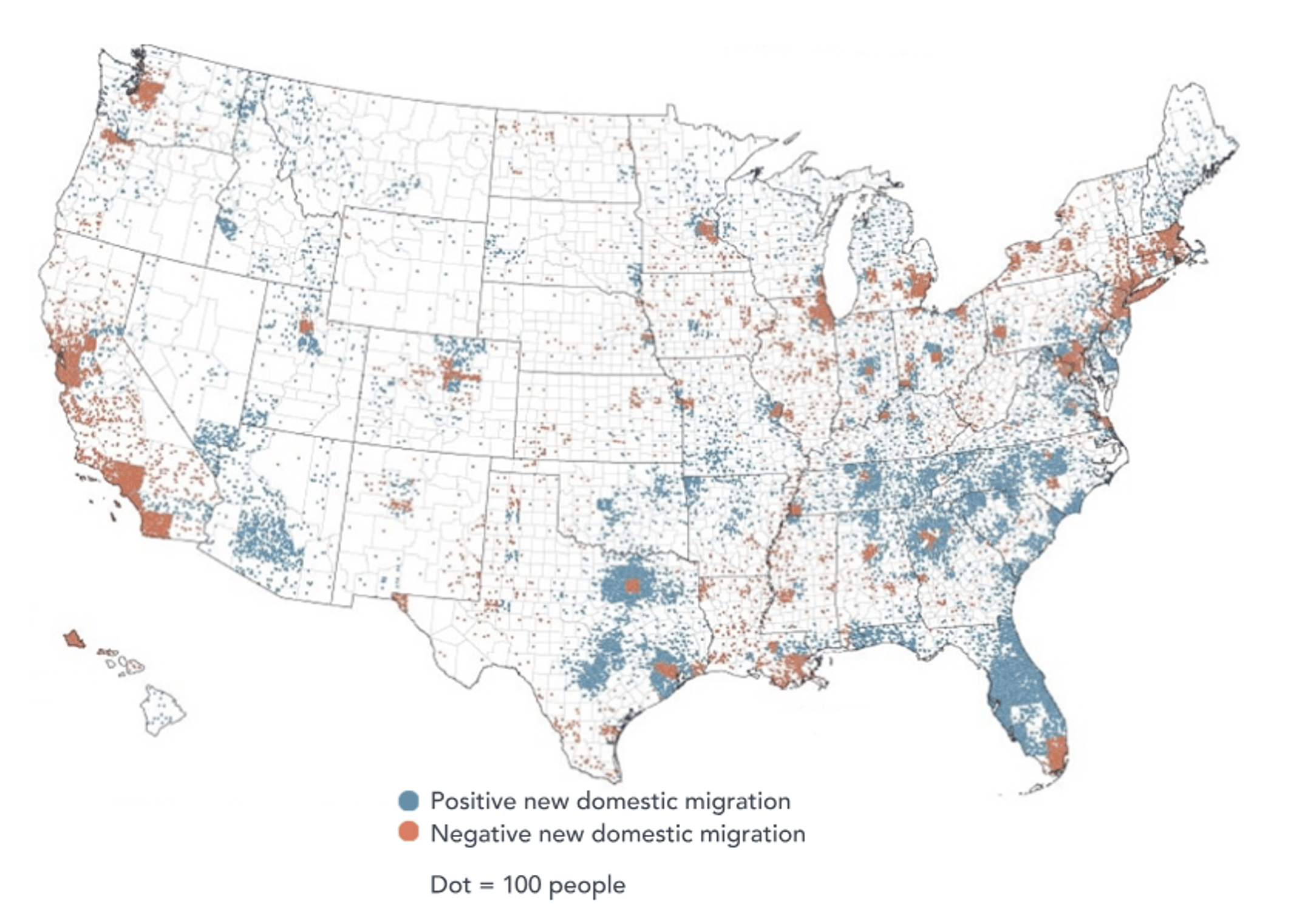

People are leaving Democrat-governed, heavily taxed, and over-regulated parts of the country for Republican-managed areas that are easier to thrive in. Sorry to get political, but those are the facts, as the map below backs up.

Source: ELS Investor Presentation

As I mentioned Monday, Massachusetts lost more than 180,000 residents between April 2020 and July 2025. And Meta CEO Mark Zuckerberg has joined the lengthening list of billionaires buying primary residences outside of California.

Plus, more than 60 companies have left or announced their intention to leave Delaware in the past two years.

And in New York City, Mayor Zohran Mamdani announced the city’s first-ever pied-à-terre tax. This will impose annual fees on people who don’t live there full-time but still own local luxury properties worth at least $5 million.

That includes Ken Griffin, CEO of Citadel, one of the world’s largest hedge funds.

Mandani targeted him specifically, intentionally, and, apparently, proudly considering how he isn’t backing down from the attack. Not even after Citadel Chief Operating Officer Gerald Beeson responded with a public rebuttal that:

Over the past five years, our principals and team members (including non-residents) have paid nearly $2.3 billion… in city and state taxes, providing funds to support the city’s infrastructure, schools, parks, and first responders.

Then he mentioned Citadel’s planned 350 Park Avenue redevelopment project, which would involve more than $6 billion in spending – if the company moves forward with it.

It seems those plans are no longer set in stone, thanks to Mamdani.

Citadel might very well decide what so many other former blue-state operators have already recognized: That there are much greener pastures out there to invest in.

When a Billionaire Says Thank You

Ken Griffin himself is already in the very sunny state of Florida, having fled from Chicago, Illinois to Miami, Florida four years ago. He took both of his multibillion-dollar businesses with him, too: Citadel and Citadel Securities.

Here’s what he said about the move late last year:

Do you know how great it is to go to dinner, and people talk about their children, and they talk about their future, and they do so with excitement and enthusiasm? We lost that in Chicago in the last 10 years.

Dinner in Chicago would be about crime, about cronyism, about failed policies in the state. It is so refreshing to be in a city where people talk about tomorrow.

Even so, Citadel still planned on building a NYC headquarters through a joint venture that included local real estate investment trust (“REIT”) Vornado Realty Trust (VNO). The massive hedge fund was going to at least anchor the new and improved 350 Park Avenue office building – if not lease the majority of the 1.85 million square-foot development.

Now it might not invest in the project at all.

Do you know what project is a definite go, however? The $1 billion, 54-story, waterfront office tower Citadel is being developed in Miami. And its CEO is reportedly constructing an enormously expensive personal residence on 27 acres in Palm Beach.

Then there’s the private 30,000-square-foot marina Griffin purchased last year for superyachts… the $180 million office building he bought this year… and the $10 million “Ambition Accelerated” campaign he and real estate developer Stephen Ross began in February to tempt other businesses down to South Florida as well.

That’s the kind of “thank you” billionaires can give cities and states when they feel welcome.

Florida is flourishing as a result, opening up investment opportunities left and right… including in the realm of REITs.

Equity Lifestyle Is Living It Up

Equity LifeStyle Properties (ELS) is one of three manufactured housing REITs in the U.S., with 453 operating properties. It traces its roots back to the early 1990s and is widely viewed as the best-in-class operator in its peer group.

That might not sound like the most impressive title considering how it owns “trailer parks.” But bear with me as I reveal the Sun Belt-lit details…

Equity LifeStyle has grown over the decades through strategic acquisitions, premium community development, and a focus on high-quality, amenity-rich properties. These aren’t poor neighborhoods it’s in charge of; these spaces are actually very desirable places to live.

They’re also ideally situated in high-demand Sun Belt states, particularly Florida, where so many people go to retire. Many of its communities are reserved for seniors only, so that works out well for Equity.

Its sticky customer base is another selling point, with just 0.4% move-outs per year. And the fact that manufactured homes cost 50% less to build than traditional single-family residences – or that there’s still such a housing deficit – doesn’t hurt either.

Equity doesn’t take any of that for granted, though. It remains focused on disciplined capital allocation and operational excellence, consistently delivering steady net operating income (“NOI”) growth.

Take the first quarter of 2026, where the REIT delivered better-than-expected core funds from operations, up $0.01 from the consensus. Driven by lowered expenses and solid membership revenue, it led Equity to raise same-store NOI guidance by 10 basis points (“bps”) for the full year.

CEO Marguerite Nader pointed out on the first-quarter earnings call that “homeowners represent 97% of our [manufactured housing] portfolio” which “is a key driver of our predictable recurring cash flow.”

Equity also owns an RV portfolio. And as Nader explained there, “annual customers stay in park models, resort cottages, and RVs, with many families viewing [our] properties as an integral part of their traditions and family history.”

That makes for even more sticky revenue. So it should be no surprise that Equity’s balance sheet is strong.

The REIT’s debt to earnings before interest, taxes, depreciation, and amortization for real estate (EBITDAre) is 4.5 times. Its interest coverage is 5.6 times, and it has access to around $1.2 billion of capital between its line of credit and at-the-market (“ATM”) programs.

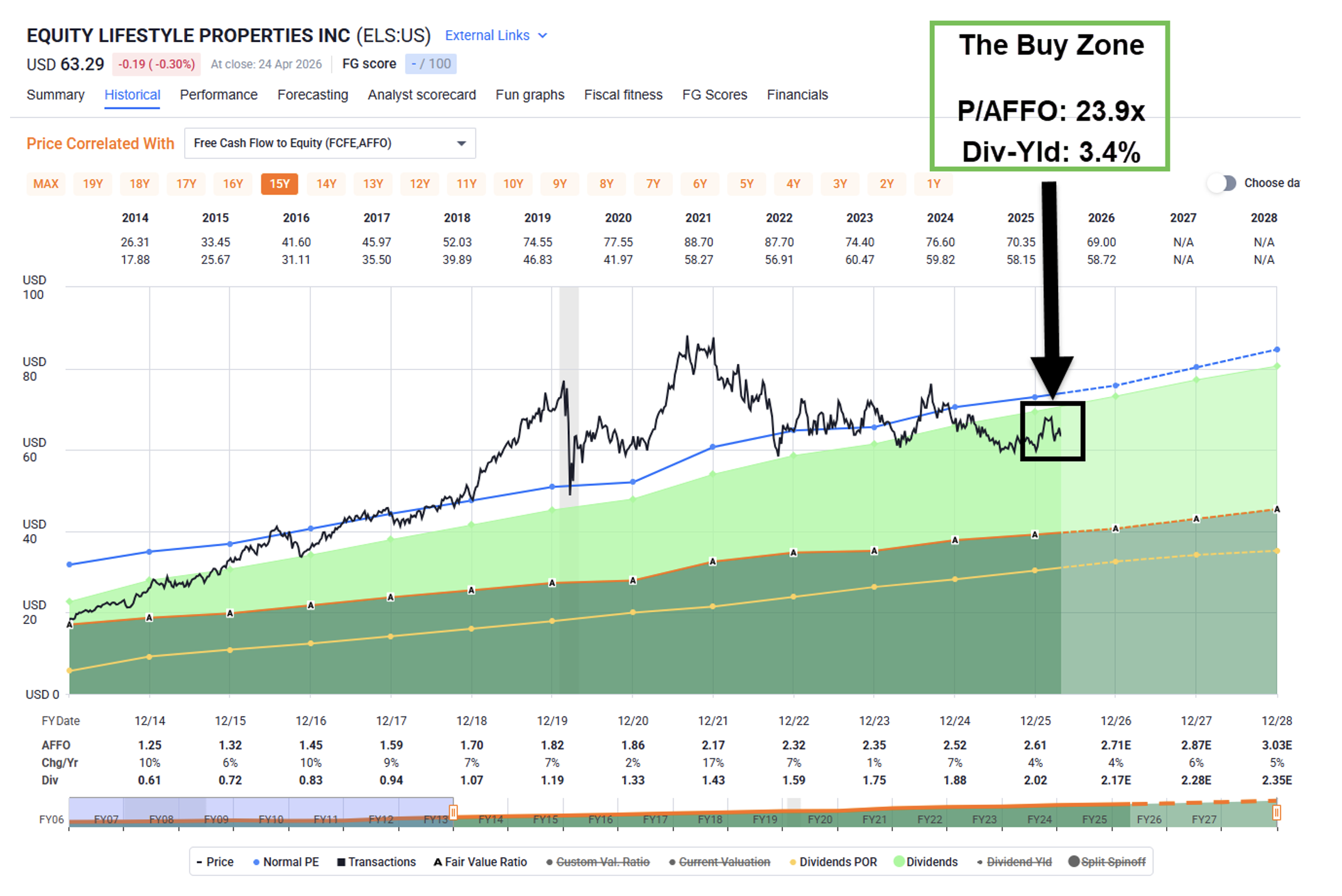

Yet somehow, shares are now trading in our buy zone, with a price to adjusted funds from operations (“AFFO”) multiple of 23.9 times instead of their normal 28 times. The dividend yield is 3.4%, and analysts expect around 5% growth in 2026, 2027, and 2028 as well.

All put together, ELS could realistically generate returns of around 20% annually.

Source: FAST Graphs

Regards,

Brad Thomas

Editor, Wide Moat Daily

P.S. Be sure to tune into The Wide Moat Show on Thursday, where I have nine other wide-moat stocks to talk about in addition to ELS.

|